|

Finance and Management

Reference:

Safarli, A.H., Mamedov, M.A., Bolonin, A.I. (2022). The current state and prospects for further development of the global cryptocurrency market. Finance and Management, 3, 48–60. https://doi.org/10.25136/2409-7802.2022.3.38305

The current state and prospects for further development of the global cryptocurrency market

Safarli Aziz Hafis Ogly

ORCID: 0000-0002-5349-015X

Postgraduate Student, Department of International Finance, Moscow State Institute of International Relations (University)

119454, Russia, Moskva oblast', g. Moscow, ul. Prospekt Vernadskogo, 76

|

aziz.safarli@mail.ru

|

|

|

Other publications by this author

|

|

Mamedov Murad Azer Ogly

ORCID: 0000-0003-2751-8283

Postgraduate Student, Department of International Finance, Moscow State Institute of International Relations (University)

119454, g. Moscow, ul. Prospekt Vernadskogo, 76

|

|

murad.mammad15@gmail.com

|

|

|

|

Bolonin Aleksei Ivanovich

ORCID: 0000-0003-0351-8529

Doctor of Economics

Professor, Department of International Finance, Moscow State Institute of International Relations (University)

115494, Russia, g. Mosvka, ul. Prospekt Vernadskogo, 76

|

|

danrotten@yandex.ru

|

|

|

|

DOI: 10.25136/2409-7802.2022.3.38305

EDN: KBYGJS

Received:

22-06-2022

Published:

08-10-2022

Abstract:

The article examines the genesis and technologies of the cryptocurrencies, presents data from leading cryptocurrencies platforms for the purpose of in-depth analysis of the current market situation. In recent years, there has been a significant growth of the cryptocurrency market, the development of new technologies and products on the market, as well as an increase in its influence on more traditional financial markets. In this regard, the issue of regulating cryptocurrencies at the national and supranational levels is becoming increasingly relevant. The subjects of the research are the international cryptocurrency market, the technology of the distribution register, the experience of various countries in regulating the issuance and circulation of cryptocurrencies. Based on the results of the study, the authors identified current trends in the global cryptocurrency market. According to the authors, it is practically impossible to completely ban the issue and turnover of cryptocurrencies by the state due to their decentralized nature. Regulation of the cryptocurrency market is a new source of funds for the tax budget, and will also contribute to the further development of the field of digital technologies. In the article, the authors investigated the approaches a number of countries in the direction of regulation and legalization of the cryptocurrency market, which can be used as an example in the process of creating a regulatory framework for the Russian cryptocurrency market.

Keywords:

cryptocurrency, blockchain, digital currency, bitcoin, stablecoin, token, altcoin, smart contract, mining, digital financial asset

This article is automatically translated.

introduction Interest in cryptocurrencies among both large investors and ordinary citizens is increasing every day, despite the inconsistency and increased risk of this type of asset. The relevance of the topic of the article is justified by the fact that today there is a rapid growth of the cryptocurrency market, new products appear on the market, created on the basis of increasingly advanced technologies and mechanisms. To date, there are no centralized international bodies and rules for regulating the cryptocurrency market in the global economy, countries independently investigate the issue of cryptocurrency turnover at the state level. According to a number of statistics, the Russian cryptocurrency market is one of the fastest growing and promising in the world. To date, the issue of further development of this market and its regulation at the macro level is relevant. The purpose of this study is to determine the current trends in the global cryptocurrency market and the prospects for its further development. In the course of the research, the scientific works of both domestic (Gulyaev R. A. [3], Sinelnikov-Muryleva E.V. [4]) and foreign authors (Ciaian P. [16], Gee W. [19], Giudici G. [20]) were studied. Analytical data of specialized news agencies and mass media were also used. As the methodological basis of the work, general scientific methods and research techniques are used: analysis, synthesis, analogy, methods of historical and logical cognition, comparative and systematic approaches. The methodological basis of the article is based on the principles of scientific objectivity. According to the results of the study, the current trends of the international cryptocurrency market will be revealed and the author's position on the further development of this market will be described. Despite the fact that the phenomenon of cryptocurrencies is one of the key objects of research in the field of digital economy, there is currently no single definition for this asset. In its materials, the World Bank interprets cryptocurrencies as "the most developed product of the technology of distribution registers, which is able to create money without the participation of central banks and carry out monetary transactions without the participation of financial organizations" [27, p. 21]. In the statistical sources of the International Monetary Fund, cryptocurrencies are called "digital assets developed as means of exchange" [24, p. 5]. ECONOMIC INTERPRETATION OF CRYPTOCURRENCIESFor the first time in Russian legislation, cryptocurrency was described as a "digital financial asset created and accounted for in a distributed register of digital transactions by the participants of this register in accordance with the rules for maintaining a register of digital transactions" [2] according to Article No. 2 of the draft Federal Law dated 25.01.2018 "On Digital Financial Assets" of the Ministry of Finance of the Russian Federation. However, in the first legislative document approved and published to regulate the cryptocurrency market in the Russian Federation, namely in the Federal Law "On Digital Financial Assets, Digital Currency and on Amendments to Certain Legislative Acts of the Russian Federation" dated 31.07.2020 N 259-FZ, where cryptocurrency was defined as a digital currency, which means a set of electronic data (digital code or designation) contained in the information system, offered and (or) accepted as a means of payment that is not a monetary unit of the Russian Federation, a monetary unit of a foreign state and (or) an international monetary or settlement unit [1]. Thus, having studied the definitions of cryptocurrencies proposed by international organizations, state legislatures and experts in this area, it can be summarized that a cryptocurrency is a digital representation of value that does not have the status of a legal tender and operates on the basis of distributed registry technology. A distributed registry is a decentralized data system based on the calculations of network nodes. Nodes are called electronic devices that have access to the Internet and an IP address and keep records of updating the distributed registry [4, p. 38]. For their work, the nodes receive a reward in the form of a commission or a new cryptocurrency based on the results of the update. Blockchain is one of the varieties of the distribution registry. The specificity of the blockchain is that the information in this system is distributed in blocks. Each new block contains data on operations performed during a specific period of time. For the first time, the blockchain system was used in practice as part of the release of the bitcoin cryptocurrency (Bitcoin – BTC). We will analyze the implementation of the transaction in the blockchain system using the example of the purchase of a service with cryptocurrency. To purchase the service, the sender of the payment provides data to the recipient's wallet address, the transfer amount, as well as other information, if necessary. The transaction is checked and connected with other transactions that are performed within the same time [20, p. 21]. Next, the nodes encrypt the collected data based on cryptographic calculations, after which the data collection enters a new block. All nodes update their versions of the blockchain and confirm that the block is generated correctly. If a block is not generated in accordance with the rules as a result of unauthorized interference or due to incorrect data receipt, the network participants will not include it in the block chain and the transaction will not be considered completed. After that, the specified amount is transferred to the seller's wallet, and the operation is considered implemented [3, p. 331].

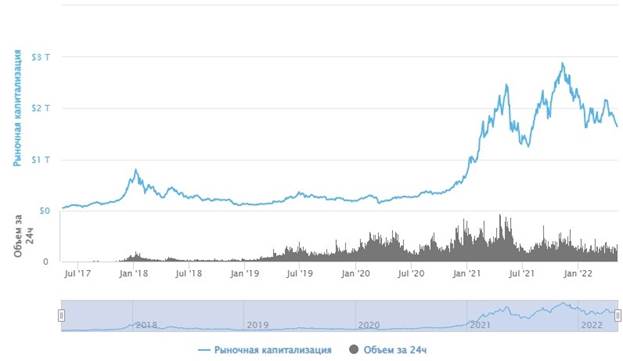

Updating the distributed registry (in the case of blockchain, adding a new block) occurs by voting of all nodes, this process is called consensus. There are two main types of consensus: Proof of work (Proof-of-Work — PoW) and proof of ownership (Proof-of-Stake — PoS). With the PoW consensus type, nodes compete for the creation of each new block, working on solving a cryptographic problem. This process is called mining [14, p.37]. There is more chance to generate a new block for the node (miner) whose computing power is greater, respectively. Each new subsequent block is extracted by calculating more complex cryptographic tasks, and thus becomes more energy-consuming and expensive. As a result of generating a new block, new coins of this cryptocurrency are issued, which is a reward for nodes. The supply of cryptocurrencies that are issued under the "proof of work" consensus mechanism is limited, but the achievement of the maximum amount is delayed in time [17, p. 35]. With the type of PoS consensus, the chance of creating a new block is greater for the system participant who owns a large amount of cryptocurrency. During the generation of a new block with this type of consensus, there is no mining of a new cryptocurrency. The role of remuneration is the commission from the operations that the block contains [16, p. 890]. The issue of cryptocurrencies with the "proof of ownership" consensus mechanism is fully carried out at the time of the creation of this cryptocurrency. In 2008, a White Paper text file was published by a person or group of people under the pseudonym Satoshi Nakamoto, which described the operation of the blockchain and bitcoin system. In 2009, the first 50 bitcoins were issued and the first transaction was carried out, Satoshi successfully transferred 10 bitcoins to another participant of the network [12]. In the same year, the first purchase of bitcoin for a fiat currency was made. 5050 bitcoins were purchased for 5.02 USD. In 2010, a serious global error was detected in the system. It was due to the fact that operations before being added to the blockchain did not pass through verification. The scammers, using this gap, generated 184 billion coins and sent them to two addresses. However, the developers managed to solve this problem and cancel the fraud operation. As the cryptocurrency market developed, its attractiveness increased not only from investors and traders, but also from many IT specialists. Unlike investors, they are more interested in further research and development of blockchain technology, improvement of current and development of new products for the market. In 2011, British programmer Amir Taaki developed proposals to improve bitcoin (Bitcoin Improvement Proposal – BIP) [28]. It was expected that the implementation of these proposals would eliminate errors that existed in the system. But the most important value that Taaki's proposals brought to the industry was the opportunity to create new cryptocurrencies. In the market, cryptocurrencies other than bitcoin are called altcoins. One of the first altcoins released is Litecoin (Litecoin – LTC). It is considered an offshoot of bitcoin and has many similarities with the first cryptocurrency. Litecoin is easier to mine, has a higher speed of organizing operations and is much cheaper than bitcoin. One of the main pushes for the development of the cryptocurrency market is the launch of the Ethereum project by programmer Vitalik Buterin in 2015. Ethereum is a smart contract platform for the development of decentralized services based on its own blockchain system, where the platform's cryptocurrency, ether (Ether - ETH), which is the second in capitalization after bitcoin, is also in circulation. A smart contract is an agreement with automated execution [15, p. 9]. This process is implemented by running code that has been converted from a legal text into an executable program. In the Ethereum blockchain, a smart contract is an autonomous computer program implemented automatically if the necessary conditions are met. CURRENT TRENDS IN THE CRYPTOCURRENCY MARKET AND PROSPECTS FOR ITS DEVELOPMENTAccording to the information platform ”CoinMarketCap", the capitalization of the cryptocurrency market for May 2022 is 1.2 trillion US dollars [11]. In addition, the cryptocurrency market also includes stablecoins and tokens. Figure 1. Total market capitalization of cryptocurrenciesSource: Information platform about the global crypto asset market CoinMarketMap.

[electronic resource]. URL: https://coinmarketcap.com / (accessed: 05/28/2022) Stab coins are digital coins whose value is tied to a specific physical asset. The role of such assets can be fiat currencies, securities, natural resources, precious metals, real estate, etc. Due to this binding, the cost of stablecoins is significantly less volatile than that of standard cryptocurrencies [19, p. 5]. Thus, stablecoins provide stability for investors and traders during the period of volatility in the cryptocurrency market. Stablecoins are considered a "bridge" between the world of cryptocurrencies and the fiat world, they increase the level of liquidity and volume in the cryptocurrency market. A token (tokenized asset) is a digital certificate that assigns certain rights to its owner, is considered an analogue of securities or a confirmation of the right to receive specific goods and services in the digital sphere. Tokens are registered using blockchain technology, this process is called tokenization. The value of the token is tied to the value of the underlying asset (for example: a security, a precious metal) [18]. They can be traded using cryptocurrency and receive a similar profit if the investor traded the underlying asset in the traditional market. With the help of blockchain technology, it is possible to carry out operations on tokens in an operational and secure manner.

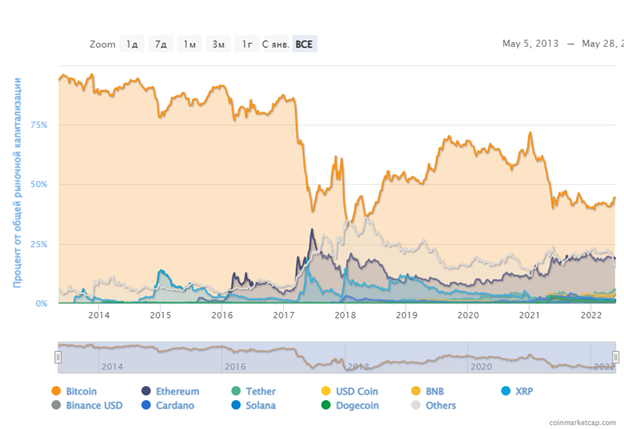

The dominant products on the crypto asset market are cryptocurrencies Bitcoin (44.8%) and Ethereum (19.2%). A total of 19,626 assets are transacted on the market [11]. Figure 2. Shares of cryptocurrencies from the total market capitalizationSource: Information platform about the global crypto asset market CoinMarketMap.

[electronic resource]. URL: https://coinmarketcap.com / (accessed: 05/28/2022) According to a study by the world's leading blockchain ecosystem Binance “2021 Global Crypto User Index”, 15% of cryptocurrency owners consider them the main source of their income. 65% of cryptocurrency owners have bitcoin in their portfolio [21]. Basically, the owners of cryptocurrencies see the prospect of obtaining high returns in the long term. Distrust of the current financial system also increases interest in this market. Cryptocurrencies are also attractive to many investors due to the fact that there is an idea that they are more resistant to inflation compared to fiat currencies. The basis of this statement is a limited number of cryptocurrencies in circulation. However, despite this advantage of cryptocurrencies over fiat currencies, they cannot be called a confident tool to protect savings from inflation due to their high volatility and lack of regulation of their turnover. Binance in its study divides all owners of cryptocurrencies into two groups: crypto experts (crypto natives) and ordinary owners of cryptocurrencies (general crypto users). Crypto experts own 13% of all cryptocurrencies on the market [21]. Binance counts those among the crypto experts: · who has cryptocurrencies as the main source of profit; · who makes payments in cryptocurrency in everyday life; · who is highly informed about blockchain technology and the cryptocurrency market; · who expects higher profits in the longer term. The attitude towards the cryptocurrency market on the part of the state authorities is ambiguous. In 2021, El Salvador adopted bitcoin as a national means of payment. Previously, this state did not have its own national currency, US dollars were actively used in circulation. This step on the part of the authorities was taken in order to attract the attention of investors in cryptocurrencies, as well as to increase the volume of non-cash payments in the national economy. At the same time, a ban on any activity related to cryptocurrencies came into force in China during the same period of time. At the end of 2020, this country accounted for half of the global bitcoin mining volume [29]. The US and the EU have taken the first steps in regulating the market of stab coins, which are linked to fiat assets and show a lower level of volatility than traditional cryptocurrencies. However, issuers of stab coins need to have sufficient reserves to maintain the issued currency. At the end of 2021, the US authorities published a plan to regulate the stab coin market. According to this plan, insured depository institutions that are subject to banking regulation with the necessary capital and liquidity sufficiency can issue stab coins [25]. In parallel, almost at the same time, the European Council presented a strategy for regulating the crypto assets market (Regulation on Markets in Crypto-Assets - MiCA), according to which companies providing services related to cryptocurrencies will be subject to licensing and capital requirements [26]. The Bank of England also takes a tough stance on the regulation of the stablecoin market. According to the British regulator, issuers of such altcoins should have reserves in fiat money in an amount that should fully cover the cost of the issue [31]. Japan, in 2017, was the first in the world to introduce measures to regulate the cryptocurrency market. In relation to crypto exchanges, capital requirements are set, they need to identify participants and track their operations. The Financial Services Agency of Japan plans to leave the possibility of issuing stablecoins only with banks [30]. The analytical company Chainalysis has been publishing an annual rating of states on the Global Crypto Adoption Index (Global Crypto Adoption Index) since 2020 [22]. The Global acceptance Index is a geometric mean of the following indicators: · the value of the cryptocurrency received by the country within the framework of blockchain operations; · the cost of cryptocurrency transferred from the country within the framework of blockchain operations; · the volume of direct transactions with cryptocurrencies in peer-to-peer format on the Paxful and LocalBitcoins platforms.

These indicators are weighted by purchasing power parity per capita in each country under study. The list of countries with the highest cryptocurrency adoption index is dominated by emerging economies. Vietnam tops this list, India and Pakistan took the second and third places, respectively, Russia takes the 18th place in the list. According to the analysis of Chainalysis, the growth in the turnover of cryptocurrencies in developing countries is mainly due to the desire of citizens to earn on the crypto asset market and protect their income from the depreciation of the national currency. In countries with developed economies, the main locomotives of the crypto market development are institutional investors. They invest in cryptocurrencies to hedge assets against inflation, as well as to diversify investment portfolios. As cryptocurrencies become more and more popular not only among private and institutional investors, but also among non-financial organizations, the correlation between traditional financial assets and crypto assets is increasing. According to IMF experts, this will lead to the fact that cryptocurrencies will lose their relevance as a tool for diversification [23]. Many experts draw an analogy between the current course of development of the crypto asset market with the growing popularity of other financial bubbles, which eventually led to economic crises. Most owners of cryptocurrencies have a low level of income, acquire them in the hope of earning easy money and are far from fully informed about the risks they carry. International organizations are mainly in favor of regulating the turnover of cryptocurrencies. In addition to the fact that cryptocurrencies can be used as tools for fraud and money laundering, the expansion of their turnover also reduces the effectiveness of monetary policy within the country. According to the chief economist of the IMF, Gita Gopinath, states should adhere to the policy of regulating cryptocurrencies, since if they are banned, the authorities will completely lose control over the market. It is impossible to completely ban cryptocurrencies, since their users can use decentralized tools that do not obey any legislative norms and rules [8]. The Bank of Russia at the beginning of 2022 estimated the volume of transactions of Russians with cryptocurrencies in the amount of 5 billion US dollars [5]. As of May 2022, Russia is the main source of traffic to the Binance platform (7.31%) [7]. According to a survey by the Bank of Russia from September 2021, 18% of novice investors in the country choose cryptocurrencies as their first investment assets [7]. By the end of 2021, Russia became the fifth country in the world in terms of bitcoin mining. It accounts for 4.66% of the computing power used to mine the first cryptocurrency [29]. According to the Cambridge Center for Alternative Finance online service, which demonstrates current electricity consumption in connection with bitcoin transactions, as of January 2022, the largest amounts of computing power used for bitcoin mining are in the United States (37.84%). Despite the fact that bitcoin mining is banned in China, the country ranks second in its production (21.11%). The third and fourth places are occupied by Kazakhstan (13.22%) and Canada (6.48%). Such a high rate of cryptocurrency mining in Russia is mainly due to the presence in the country of many sources of cheap electricity in various forms. There are large hydroelectric power plants on the territory of the Russian Federation that can provide miners with not only cheap, but also environmentally friendly electricity. Oil companies that provide electricity on associated gas have also begun to actively cooperate with miners. In 2020, at the initiative of Gazprom Neft, a project was launched for the useful use of associated gas at the Alexander Zhagrin field in the KhMAO. The company connected a mobile mining farm to the associated gas power plant, providing miners with the opportunity to use the generated electricity to mine cryptocurrencies. As a result, during a month of test mining, the participants of the Gazprom Neft project disposed of 49,500 m3 of associated gas, used 170 million kWh and extracted 1.8 BTC [10]. Since the beginning of 2021, Federal Law No. 259 "On Digital Financial Assets and Digital Currency" has entered into force in Russia. This law prohibits cryptocurrencies from paying for goods and services and recognizes them as property. The tax base is the difference between the purchase price and the sale price of a cryptocurrency [1]. According to many experts, this law does not reflect the answers to all the questions that concern citizens, and the issue of regulating the Russian cryptocurrency market is still open. In fact, at the moment the Russian cryptocurrency market is not regulated, the only restriction on the market is the prohibition of using cryptocurrencies as means of payment. At the beginning of 2022, the Bank of Russia prepared a draft banning the issuance and circulation of cryptocurrencies. Also, according to this draft, banks and other financial organizations are prohibited from holding private digital currencies in assets. For violations, the regulator proposes to introduce administrative fines. According to the Central Bank, interest in cryptocurrencies is growing rapidly among citizens, and they are increasingly inclined to invest their savings in them. The decentralization of the issue of these assets, the volatility of their value and the lack of their provision make transactions with cryptocurrencies risky both for the welfare of the population and for the stability of the national economy. The regulator also adds that the status of the ruble, which is not a reserve currency, does not allow for a soft approach in Russia and ignoring the increase in risk [5]. In parallel, the Ministry of Finance has submitted to the government its own version of the bill on the regulation of cryptocurrencies, on the basis of which the Ministry of Finance proposes to organize a regulated legal market for digital currencies with established rules for their turnover and participants. This project, unlike the one proposed by the Bank of Russia, does not imply a ban on the issuance and circulation of cryptocurrencies. According to the draft, it is necessary to transfer the organization of all transactions with private digital currencies to banks and identify holders of crypto wallets, as well as allow only qualified investors to carry out transactions. The government approved the draft of the Ministry of Finance and approved a roadmap suggesting a regulatory and restrictive regime for the cryptocurrency market, Vladimir Putin, for his part, also asked the Ministry of Finance and the Central Bank to come to a common opinion on the regulation of cryptocurrencies.

Against the background of active work and discussions between the Bank of Russia and the Ministry of Finance about the future of the Russian cryptocurrency market, other government agencies also share their positions on this issue. According to the statements of the Ministry of Economic Development, the mining of cryptocurrencies should be recognized as a commercial activity and taxed upon the conversion of cryptocurrencies into rubles [9]. The agency recommends allowing mining in regions with a stable surplus of electricity generation and offering acceptable prices for business for its consumption, explaining that this will remove the risks of insufficient electricity supply to housing, social facilities and industry in other territories. The Minister of Industry and Trade of the Russian Federation Denis Manturov also expressed his optimistic position on the regulation of the cryptocurrency market. According to Manturov, the turnover of cryptocurrencies in Russia should be correct and legal [13]. Regulatory rules will be formulated for the market, on the development of which the Central Bank and the Ministry of Finance are actively working together. The geopolitical situation may become an incentive for the development of the Russian cryptocurrency market. Against the background of the ban on the work of global payment systems with Russian banks, settlements in cryptocurrency may become one of the alternative payment options. The government of the country is considering the possibility of using digital currencies in foreign trade activities. The Bank of Russia and the Ministry of Finance, whose positions differed on the further development of the Russian cryptocurrency market, are currently jointly trying to assess the existing risks and create the necessary support for foreign trade relations. conclusionThe cryptocurrency market is developing rapidly, new, more advanced technologies and products are emerging that can also find their application in other areas of life, in addition to finance. A more transparent and independent structure of operations, a lower propensity of cryptocurrencies to inflationary phenomena attract both private and institutional investors to invest their funds in the instruments of the cryptocurrency market. However, the high volatility of cryptocurrencies puts the profitability of such investments at risk. And many private investors who do not have sufficient information about the specifics of the market put their investments at high risk, which can lead to negative consequences for the national economy at the macro level. The practice of banning the issuance and circulation of cryptocurrencies by the Chinese authorities shows that it is difficult to completely prohibit the implementation of these processes due to their decentralized nature. Despite the ban, China ranks second in bitcoin mining in the world. The number of countries that decide to regulate the turnover of cryptocurrencies in the national economy is gradually increasing. Regulation of the cryptocurrency market will not hinder the further development of technologies, providing the federal budget with a new source of financing, and market participants with legal protection. In the process of legalizing the Russian cryptocurrency market, it is possible to resort to the experience of advanced states in this direction, taking into account the specifics of the national economy.

References

1. Federal Law of July 31, 2020 No. 259 “On Digital Financial Assets, Digital Currency and on Amendments to Certain Legislative Acts of the Russian Federation”. // Consultant Plus. [Electronic resource]. URL: http://www.consultant.ru/document/cons_doc_LAW_358753/ (date of access: 05/12/2022).

2. Draft Federal Law of March 20, 2018 No. 419059-7 “On Digital Financial Assets”. Consultant Plus. [Electronic resource]. URL: http://www.consultant.ru/cons/cgi/online.cgi?req=doc&base=PRJ&n=170084#XiXtk8T63lgfhpZp/ (date of access: 05/12/2022).

3. Gulyaev R. A. Cryptocurrencies: essence, evolution and formation as a means of payment / R. A. Gulyaev // Public administration. Electronic Bulletin.-2018.-No. 70. C-329.

4. Sinelnikova-Muryleva E.V., Shilov K.D., Zubarev A.V. The essence of cryptocurrencies: descriptive and comparative analysis. / E. V. Sinelnikova-Muryleva, K. D. Shilov, A. V. Zubarev // Finance: theory and practice.-2019.-No. 23 (6). S.-36.

5. Report for public consultations of the Bank of Russia. Cryptocurrencies: trends, risks and measures. Moscow. 2022.

6. Investment behavior and investment expectations of Russian novice investors in large cities. Marcs. Moscow. 2021.

7. Analysis of traffic to the official website of the Binance crypto exchange. Information platform SimilarWeb. [Electronic resource]. URL: https://www.similarweb.com/en/website/binance.com/#overview/ (accessed 05/11/2022).

8. The IMF urged to regulate cryptocurrencies and abandon their ban. Official site of the daily business newspaper RBC. [Electronic resource]. URL: https://www.rbc.ru/crypto/news/61bc5efd9a79477181548bfb/ (date of access: 05/07/2022).

9. In Russia, they may introduce a tax upon the conversion of cryptocurrencies into rubles. Official site of the socio-political and business daily newspaper "Izvestiya" [Electronic resource]. URL: https://iz.ru/export/google/amp/1291482 (date of access: 05/15/2022).

10. Drivers and problems of cryptocurrency market development. Official site of the public and business magazine "Energy Policy". [Electronic resource]. URL: https://energypolicy.ru/drajvery-i-problemy-razvitiya-rynka-kriptovalyut/energetika/2022/12/27/ (date of access: 05.05.2022).

11. Information platform about the world market of cryptoassets CoinMarketMap. [Electronic resource]. URL: https://coinmarketcap.com/ (date of access: 05/28/2022).

12. The history of the creation of cryptocurrency: the world's first crypt and Satoshi Nakamoto. The official website of the world's leading blockchain ecosystem Binance. [Electronic resource]. URL: https://www.binance.com/en/blog/markets/ (accessed 05/17/2022).

13. Manturov allowed the legalization of cryptocurrencies in Russia. Official site of the daily business newspaper "RBC" [Electronic resource]. URL: https://amp.rbc.ru/rbcnews/finances/18/05/2022/62851ec09a794788ce6e9ecd (date of access: 05/24/2022).

14. Akyildirim, Erdinc & Corbet, Shaen & Katsiampa, Paraskevi & Kellard, Neil & Sensoy, Ahmet, 2020. "The development of Bitcoin futures: Exploring the interactions between cryptocurrency derivatives," Finance Research Letters, Elsevier, vol. 34(C). doi: 10.1016/j.frl.2019.07.007.

15. Carpenter A. Portfolio diversification with Bitcoin. Journal of Undergraduate Research in Finance. 2016;6(1):1–27.

16. Ciaian P., Rajcaniova M., Kancs A. The digital agenda of virtual currencies. Can BitCoin become a global currency? Information Systems e-Business Management. 2016;14(4):883–919.

17. Cheah E.-T., Fry J. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Economics Letters. 2015;130:32–36.

18. Cukierman, A. (2019) Welfare and political economy aspects of a central bank digital currency. Centre for Economic Policy Research, discussion paper DP13728, May 2019.

19. Gee W., Arslanian H., Wang D., Zhou J. at al. Emergence of stable value coins and a trust framework for Fiat-backed versions. Hong Kong: PwC; 2019.

20. Giancarlo Giudici, Alistair Milne, Dmitri Vinogradov. Cryptocurrencies: market analysis and perspectives. Journal of Industrial and Business Economics. 7 September 2019.

21. Binance Research. 2021 Global Crypto User Index. Crypto user profiles, attitudes and motivations.

22. Chainanalysis. The 2021 Geography of Cryptocurrency Report. Analysis of Geographic Trends in Cryptocurrency Adoption and Usage. October 2021.

23. IMF Monetary and Capital Markets. Cryptic Connections: Spillovers between Crypto and Equity Markets. No. 2022/01. Prepared by Tara Iyer. January 2022.

24. IMF Statistics Department. Treatment of Crypto Assets in Macroeconomic Statistics.

25. Presindent’s Working Group on Financial Markets, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency. Report on Stablecoins. November 2021.

26. Proposal for regulation of the European Parliament and of the Council on Markets in Crypto-assets, and amending Directive (EU) 2019/1937. Brussels, 19 November 2021.

27. Word bank group. Cryptocurrencies and Blockchain. Europe and Central Asia Economic Update. May 2018. P. 21.

28. Bitcoin Improvement Proposals (BIPs) And The BIP Process. Официальный сайт американской биржи Nasdaq. [Электронный ресурс]. URL: https://www.nasdaq.com/articles/bitcoin-improvement-proposals-bips-and-the-bip-process-2021-06-11/ (дата обращения: 27.05.2022).

29. Cambridge center for alternative finance. Cambridge bitcoin electricity consumption index. [Электронный ресурс]. URL: https://ccaf.io/cbeci/mining_map/ (дата обращения: 19.05.2022).

30. Japan Declares Bitcoin as Legal Tender. Информационная платформа TotalBitcoin. [Электронный ресурс]. URL: https://totalbitcoin.org/bitcoin-legal-tender-japan/ (дата обращения: 28.05.2022).

31. Stablecoins must face ‘difficult questions’, warns Bank of England. Официальный сайт международной деловой газеты Financial Times. [Электронный ресурс]. URL: https://www.ft.com/content/5bbf8546-29e4-4f7c-a30e-f15a5e261819/ (дата обращения: 28.05.2022).

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The reviewed article is devoted to the study of the current state and prospects for the development of the global cryptocurrency market. The research methodology is based on the study of literary sources on the topic of the work, analytical data from specialized information agencies and mass media, the use of general scientific research methods and techniques. The authors rightly attribute the relevance of the study to the rapid growth of the cryptocurrency market, the emergence of new products on the market created on the basis of increasingly advanced technologies and mechanisms. The scientific novelty of the presented research, according to the reviewer, is to identify current trends in the global cryptocurrency market and substantiate the prospects for its further development. In the article, the authors have identified the following structural sections: introduction, economic interpretation of cryptocurrencies, current trends in the cryptocurrency market and prospects for its development, Conclusion, Bibliography. The authors conduct a historical review of Russian regulatory documents describing digital financial assets, as well as consider definitions of cryptocurrencies proposed by international organizations and state legislative bodies. The article notes that as the cryptocurrency market developed, its attractiveness increased not only from investors and traders, but also from many IT specialists. The article is illustrated with two figures: "The total market capitalization of cryptocurrencies" and "The share of cryptocurrencies from the total market capitalization", the content of which highlights the current state of the global digital financial assets market. The authors believe that against the background of the ban on the operation of global payment systems with Russian banks, settlements in cryptocurrency can become one of the alternative payment options, and the Bank of Russia and the Ministry of Finance of the Russian Federation are jointly trying to assess existing risks and create the necessary support for foreign trade relations. The bibliographic list includes 31 sources – scientific articles by domestic and foreign authors in periodicals, as well as Internet resources and legal acts, to which the text contains address links indicating the presence of an appeal to opponents in the publication. The reviewed article is not without flaws. Firstly, the section "Materials and methods", generally accepted in modern scientific publications, is not highlighted in the text, although these elements of the research apparatus are reflected in the introduction. Secondly, for some reason, the names of the drawings are reflected before them, and not after, as is customary in accordance with the rules of design, and the illustrations themselves do not reflect the results of author's research and calculations, but only reproduce information posted on the Internet, which is why the quality of their image leaves much to be desired - it seems that in this case, you could simply limit yourself to a link to the appropriate resource, the description of which can be given in the bibliography. The topic of the article is relevant, the material corresponds to the topic of the journal "Finance and Management", may arouse interest among potential readers and is recommended for publication after revision.

|