|

Taxes and Taxation

Reference:

Garibov A.G.

Development of tax incentives for non-profit organizations

// Taxes and Taxation.

2023. ą 5.

P. 54-70.

DOI: 10.7256/2454-065X.2023.5.43992 EDN: FTWPIW URL: https://en.nbpublish.com/library_read_article.php?id=43992

Development of tax incentives for non-profit organizations

Garibov Aleksandr Georgievich

Student, Faculty of taxes, audit and business analysis, Financial University under the Government of Russian Federation

127083, Russia, Moscow, Moscow, Verkhnyaya Maslovka str., 15

|

garibov1507@yandex.ru

|

|

|

|

DOI: 10.7256/2454-065X.2023.5.43992

EDN: FTWPIW

Received:

08-09-2023

Published:

06-11-2023

Abstract:

The subject of the study is to identify possible ways to develop tax incentives for non-profit organizations in Russia. The author focuses on the important role of non-profit organizations in the economic development of the country and the provision of social services to society, improving the quality of life of various segments of the population. This paper examines the theoretical aspects of the functioning of NPOs and their taxation system, analyzes the dynamics of existing and newly created NPOs and the factors influencing it; identifies the main problems in the application of the norms of the Tax Code of the Russian Federation that complicate the activities of non-profit organizations, as well as existing gaps in legislation that cause contradictions in tax practice. A special place in the scientific research is occupied by the development of possible options for reforming existing regulatory legal acts in the field of taxation to stimulate the development of the domestic non-profit sector. Based on the results of the work, a conclusion is made about the inconsistency of tax legislation and the presence of administrative barriers that hinder the development of the non-profit sector in Russia. According to the author, the proposals formulated in this scientific article on changing legislation can be applied in practice and are designed to improve the existing conditions for the functioning of non-profit organizations in Russia, to create additional tax incentives for the development of the non-profit sector in our country.

Keywords:

Non-profit organizations, VAT, income tax, simplified taxation system, tax incentives, targeted receipts, targeted financing, separate accounting, charitable activities, sponsorship

This article is automatically translated.

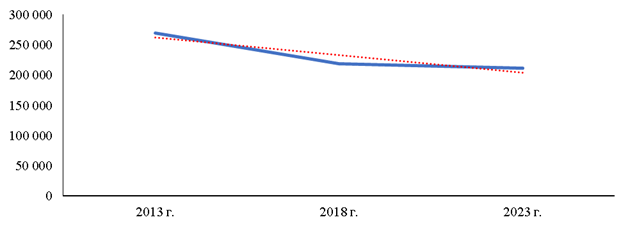

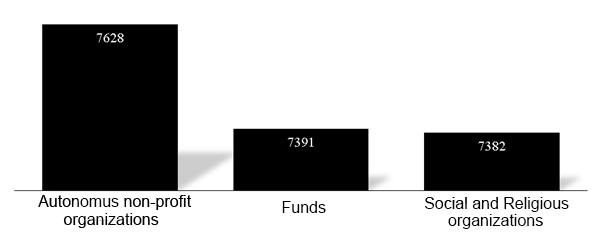

Introduction. In the process of sustainable and integrated development of the country, the formation and effective functioning of the social sphere, non-profit organizations (hereinafter referred to as NGOs) play an important role, this is evidenced not only by domestic, but also by advanced foreign experience. It is NGOs, being the most important institution of civil society, that direct their efforts to solving various social problems, as well as meeting the non-material needs of the population. In accordance with Federal Law No. 7-FZ of 12.01.1996 "On Non-Profit Organizations", a non-profit organization is recognized as "an organization that does not have profit extraction as the main purpose of its activities and does not distribute the profits received among the participants" (Federal Law No. 7-FZ of 12.01.1996 "On Non-profit organizations"). In Russia, there are a significant number of organizational and legal forms in which NGOs can be created, as well as the goals for which they are created. Non-profit organizations can carry out entrepreneurial activities, but only on the condition that the income from such activities is directed exclusively for the purpose of creating this NGO, and the very opportunity to conduct entrepreneurial activities is prescribed in the constituent documents. Such a provision, in fact, forms the basis for the construction of most regulatory legal acts regulating the activities of NGOs, including in the field of tax legislation. In general, non-profit organizations are payers of the same taxes as other organizational and legal forms of enterprises, however, when they conduct business, there is a separation: the main activity of such organizations, that is, the statutory, is not taxed; and commercial activity is taxed by the legislation in the general manner, as for commercial organizations. NPOs applying the general taxation system pay corporate income tax and VAT for the most part from transactions related to commercial activities. Also, if there is an object of taxation, even when conducting exclusively statutory activities, NGOs also pay property taxes. NGOs can also apply a simplified taxation system. Then organizations pay a single tax on the USN (also from commercial transactions), which replaces the corporate income tax, VAT and corporate property tax. The number of non-profit organizations in Russia shows a slight decrease. To date, the number of entries in the register of the Ministry of Justice is 212887 (Information portal of the Ministry of Justice of the Russian Federation (accessed: 05/11/2023)). In 2018, there were about 219 thousand such organizations, and 10 years ago in 2013 – about 270 thousand. Source: compiled by the author according to Rosstat. Figure 1. The number of registered NGOs in Russia. The territorial placement of NGOs in Russia is uneven. The largest number of NGOs is registered in Moscow – as of January 1, 2023, their number is 42720 (the number of non–profit organizations registered in the territorial section of the Rosstat State Register), among which autonomous non-profit organizations occupy the first place - 7628, then foundations - 7391, in third place - public and religious organizations - 7382 (risu noc 2). And the stochnik:compiled by the author according to Rosstat. Figure 2. The number of NGOs in Moscow by form of ownership as of 01.01.23 The number of newly created and the effectiveness of existing NPOs is influenced by many factors, and the most important of them is the taxation of such organizations. The reasons for the lack of growth and even a certain decrease in the number of NPOs, in our opinion, are due to various factors, but the key ones are the lack of proper state support measures against the background of low profitability of such organizations, especially indirect ones, including in the form of tax incentives, as well as a huge number of administrative barriers (complexity and redundancy of reporting, excessive state regulation, constant tightening of legislation, especially regarding foreign agents, lack of proper accessible infrastructure, high level of bureaucratization and corruption, and much more). Highlighting the specifics of the taxation of NPOs is necessary both to avoid risks and fully comply with current legislation, and to understand ways to improve in order to stimulate the development of the non-profit sector in Russia. The relevance of this topic is due to the need to understand the current tax mechanism for stimulating the activities of non-profit organizations for possible further improvement in order to increase the level of development of the social sphere and intangible services provided in Russia. Literature review. With the development of the non-profit sector in Russia, the issue of taxation of NGOs is reflected in a large number of studies by domestic scientists. However, it is worth noting that to date, the non-profit sector has not yet received such coverage in scientific works as other spheres and industries in terms of taxation and its features (for example, in the field of mining, trade, industry, etc.). In their work "Problems of taxation of non-profit organizations in Russia", S. Sinelnikov-Murylev and I. Trunin considered theoretical aspects of the activities of non-profit organizations, the tax regime for NGOs in Russia, as well as possible options for its reform [1]. Despite the fact that this scientific work was published more than 15 years ago, many of the identified problems have not been solved, and therefore have not lost their relevance. The authors highlighted, in particular, such problems as the ability not to tax income from donations only if the donations are charitable; restrictions on the financing of NGOs by foreign persons; lack of proper regulation in the issue of passive investments carried out by NGOs, and the taxation of income received by various means management tools on the profit of organizations. The team of authors formulated various proposals to improve the taxation system of non-profit organizations in Russia, for example, the exclusion of income from passive investments from the corporate income tax base for a certain range of NGOs; the development of clear criteria, conditions and amendments to the Tax Code of the Russian Federation for the possible exemption of NGOs from the calculation and payment of income tax.

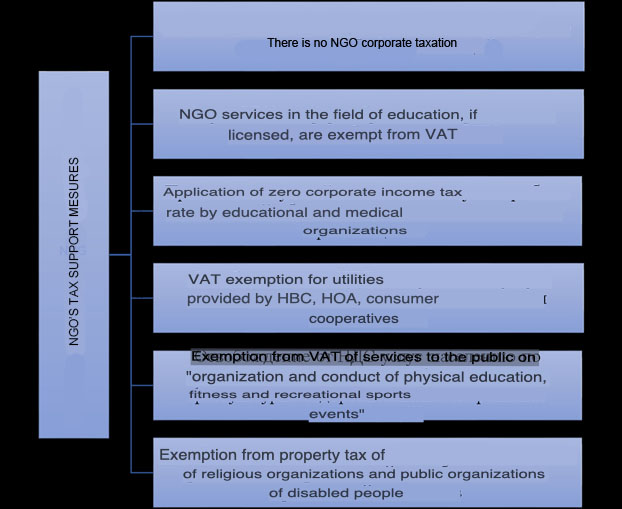

In the work "Debatable issues of tax regulation of the activities of non-profit organizations", the authors Grishchenko A.V., Grishchenko Yu.I. and Chigrakova N.M. identified three stages of the formation of the tax system in the non-profit sector [2]. The first stage from 1980 to 1993, according to the authors, is characterized by a kind of revival of the non-profit sector and the introduction in the early 1990s of the first corporate income tax benefits, which extended to a portion of profits directed to social purposes, such as, for example, charity, the maintenance of children's institutions, environmental events, etc. The second stage (1994 – 1999) was, in fact, the formation of the non-profit sector. It was during this period that the main legislative framework for the functioning of non-profit organizations in Russia was formed. In particular, on November 30, 1994, a new section "non-profit organizations" was introduced into Part one of the Civil Code of the Russian Federation, which, among other things, established the forms of non-profit organizations and their characteristics. The authors also talk about the establishment of some tax preferences related to NGOs in the field of culture and art. The third stage of the modern development of the non-profit sector began with the introduction of the Tax Code of the Russian Federation and continues to this day. According to the authors of the work, Chapter 25 of the Tax Code of the Russian Federation, which came into force, annulled "almost all the existing corporate income tax benefits relating to both non-profit organizations and their donors" [2]. At the same time, it should be noted that with the evolution of tax legislation in modern Russia, there were more and more various benefits for NGOs, which, unlike the previous stages of development mentioned earlier, already had a clearer legislative design and structure. A number of studies also emphasize that the current system of tax incentives for NPOs is focused mainly on payers of the general taxation regime, while most NPOs use the STS [3]. In particular, the specifics of the use of special tax regimes by NPOs and, in particular, the specifics of determining the income threshold for the use of the USN were considered in his work by Grishchenko Yu.I. [4]. When analyzing the specifics of calculating taxes by non-profit organizations, some scientific papers emphasize the absence in the tax legislation of a mechanism for distributing VAT amounts for general economic expenses of NGOs [5]. In addition, scientific research pays attention to the accounting and reporting of NGOs, highlights the lack of information content and completeness of disclosure of information in the Report on the targeted Use of Funds [6]. Some authors consider various, including tax, methods of supporting NGOs in the context of the COVID-19 pandemic. Attention is paid to the foreign experience of supporting non-profit organizations during the pandemic period, comparing these measures in different countries, and the Russian experience on this issue is also given [7]. Measures to stimulate NGOs in the regional context are of interest. So, Chikina A.S. and Officers P.L. in their work consider the main measures of support for non-profit organizations in the Ulyanovsk region. The authors, citing the normative legal acts of the subject regulating the non-profit sphere, analyze the indicators of various forms of support for NGOs, noting the need for further development of state incentives for this sector [8]. The authors of scientific publications also emphasize the importance of the non-profit sector for economic development and improving the quality of life of the population and the need to create a unified state policy for the formation and effective functioning of the "third sector" in Russia [9]. Articles by foreign authors concerning taxation and tax incentives for the non-profit sector are of great interest. Thus, one of the works examines tax benefits for NGOs in the United States, including the historical aspect of these benefits, and also assesses the elasticity of the tax on the income of charitable organizations [10]. Based on the analysis of tax returns of NGOs and various calculations, the author proposes a new approach to assessing the importance of tax benefits related to charitable donations. In another foreign work, the rationality of the exemption of non-profit organizations from the "federal corporate tax" (analogous to corporate income tax) in the United States is disputed [11]. According to the authors of this article, the benefits of such a benefit do not always outweigh the costs. And the various effects achieved by competition between non-profit organizations in the same market even collapse due to income tax benefits. The system of tax incentives for NGOs. The taxation of NPOs in many countries of the world contains a significant incentive component (Figure 3).

Source: compiled by the author himself. Figure 3. Instruments of tax incentives for NGOs For a clearer understanding of the mechanism of taxation of non-profit organizations and further analysis of some problems in this area, we will consider in more detail the corporate income tax and VAT. The income received by an NGO to achieve its statutory goals is not subject to taxation. Such incomes are called targeted. In order for funds to be recognized as targeted and not included in the tax base for corporate income tax , the following requirements are imposed on them: - gratuitous receipt; - intended use; - separate accounting. The target sources of income of NGOs are divided into two categories: funds of targeted financing and targeted receipts. All types of targeted financing are listed in Clause 14, clause 1, Article 251 of the Tax Code of the Russian Federation. Grants are an example of targeted financing. Clause 2 of Article 251 of the Tax Code of the Russian Federation reveals the content of the second category of targeted sources of income – targeted receipts. The main type of such receipts are funds from various levels of the budget. The difference between these types of targeted sources is that targeted funding is allocated to non-profit activities in general, and targeted revenues are allocated to specific programs or expenditure items.

Income from the sale, that is, business activities, as well as non-operating income are taxed on the profit of non-profit organizations according to the general rules. However, in some situations, special features are highlighted in practice, for example, if an organization sells a fixed asset purchased at the expense of earmarked funds before the end of its useful life, then the entire cost of the fixed asset will be taxed, since it was not used for its intended purpose (Letter of the Ministry of Finance of the Russian Federation dated 26.06.2020 No. 03-03-06/1/55183 ). In terms of expenses, it is also important to keep separate records, that is: expenses incurred at the expense of earmarked funds are not taken into account in taxation; only those expenses that are made at the expense of entrepreneurial activity can be taken into account. This rule applies to all types of expenses. For example, depreciation is charged only on fixed assets acquired at the expense of income from commercial activities. Of course, fixed assets are often used by non-profit organizations simultaneously for statutory and business purposes. But it is impossible to take into account even a part of depreciation, since the officially fixed procedure for dividing depreciation deductions is not fixed. In the value added tax within the framework of taxation of non-profit organizations, a similar feature can be traced: the VAT tax base is formed only by transactions from entrepreneurial activity; target receipts are not subject to taxation and, accordingly, do not participate in the formation of the VAT tax base. Article 149 of the Tax Code of the Russian Federation lists transactions that are not subject to VAT. Some of these benefits apply only to non-profit organizations. For example, services in the field of education. In accordance with Clause 14, clause 2, Article 149 of the Tax Code of the Russian Federation, they must be specified in the license issued by the relevant NGO. At the same time, income from the sale of other services or goods will be subject to VAT, regardless of their further orientation. Another example of benefits only for non-profit organizations is the exemption from VAT of utilities that are provided by various management organizations in the housing and communal services sector: HBC, HOA, consumer cooperatives, etc. At the same time, such NGOs should provide utilities themselves, and not act as an intermediary, purchasing them from other organizations. Also, the right of exemption from VAT applies to NGOs in the case when the revenue for the three previous periods did not exceed 2 million rubles. It is important to note that targeted receipts are not included in the limit, since they are not revenue for the organization. A large number of NGOs work in the field of physical culture and sports, and the state has also introduced certain benefits. Thus, one of the measures of tax incentives is the exemption from VAT of services to the population for "the organization and conduct of physical culture, physical culture and recreational sports events." Also, in accordance with paragraph 13, paragraph 3 of Article 149, the sale of entrance tickets to sports and entertainment events and the rental of sports facilities for such events are not subject to VAT. Therefore, in the case of an NGO, if, for example, its statutory activity is the popularization and development of physical culture and sports and at the same time it sells training passes at its institution, then such implementation will not be subject to VAT, despite the fact that it will be an entrepreneurial activity. One of the main areas of NGO activity is charity. The legislation exempts the transfer of goods (performance of works, provision of services) free of charge within the framework of charitable activities. Public organizations of disabled persons that meet the requirements of clause 2, clause 3, Article 149 are also exempt from VAT. The issue of VAT deduction for general economic transactions, that is, transactions related to both commercial and non-commercial activities is very complicated. For example, E.S. Mityukova believes that the distribution of VAT in this case may lead to proceedings in court [12]. The main justification for this position is that when an organization carries out its statutory activities, the concept of shipped goods, works and services does not arise. In addition, all income from core activities, that is, targeted financing, is gratuitous and at the same time can be directed both to specific programs and to support the activities of NGOs as a whole. Therefore, it is quite problematic to calculate the proportion of revenue, as stipulated in paragraph 4 of Article 170, and therefore, the distribution of VAT on general economic transactions by type of activity and subsequent deduction is a tax risk. Another benefit related to wages, but, nevertheless, related to non-profit organizations, is associated with exemption from payroll taxes. According to paragraph 1 of Article 217 of the Tax Code of the Russian Federation and paragraph 2 of paragraph 1 of Article 422 of the Tax Code, athletes' meals and sports referees, sports equipment and uniforms during the training process and participation in competitions are exempt from personal income tax and insurance premiums. Such a benefit, especially with a large number of athletes or the organization of large competitions, allows NGOs to save on labor costs. Non-profit organizations are payers of corporate property tax. At the same time, only real estate is recognized as an object of taxation, since movable property has been exempt from taxation since 2019. The procedure for determining the tax base and calculating the tax on property used for entrepreneurial activity is similar to the mechanism of commercial organizations. The tax base according to Article 375 is determined by one of two options: 1) the average annual value of the property; 2) the cadastral value of the property listed in Article 378.2 of the Tax Code of the Russian Federation. For property used for non-commercial, statutory purposes, there are features and benefits in the imposition of this tax. At the same time, as such, there is no division for property taxation for commercial and non-profit organizations, certain exemptions have been introduced by law in a general manner. The list of organizations exempt from taxation is named in Article 381 of the Tax Code of the Russian Federation. Thus, according to paragraph 2 of Article 381, religious organizations are exempt from property tax, which they use in religious activities. Paragraph 3 of the above-mentioned article, in respect of property used in statutory activities, exempted from payment all-Russian public organizations of disabled people, in which at least 80% of employees are disabled and their representatives. The property of bar associations, law offices and legal consultations has also been released under clause 14 of Article 381.

Continuing the topic of property taxes, consider the transport tax. Article 358 of the Tax Code of the Russian Federation establishes vehicles that are not subject to taxation. This benefit applies to all organizations, as well as to individuals. The Tax Code does not provide for separate benefits for NGOs on transport tax. However, the transport tax is a regional tax, therefore the subjects of the Russian Federation can establish benefits on their territory. Thus, Article 7 of the Law of the Moscow Region "On Preferential Taxation in the Moscow Region" (Law of the Moscow Region dated 24.11.2003 No. 151/2004-OZ "On Preferential taxation in the Moscow Region") exempts public organizations of disabled persons from paying transport tax. In addition, according to Article 26.7 of the above-mentioned law, educational organizations that carry out educational activities under additional educational programs are exempt from paying this tax. In accordance with paragraph 2 of Article 26.30 of the same law, socially-oriented non-profit organizations were also exempt from paying tax from 2020 to 2022. In the legislation of other regions, you can also find the practice of spot exemption of NGOs from paying transport tax. Problems of taxation of NPOs. As mentioned earlier, only income from commercial activities is subject to corporate income tax. However, the legislation does not mention the passive income of NGOs, for example, from the placement of targeted funds on bank deposits. An organization may have temporarily free earmarked funds (received without specific deadlines and expenditure items) and the use of various financial instruments may be quite understandable. NPOs can invest in government securities, shares and bonds of Russian companies, cash and deposits, and other instruments. Let's take a closer look at bank deposits as one of the most popular and less risky financial instruments. According to the position of the Ministry of Finance of the Russian Federation, the placement of free balances of target receipts on deposit accounts is a form of saving money and is not taken into account in the corporate income tax base (Letter of the Ministry of Finance dated 04/25/2019 No. 03-03-06/1/30255 ). At the same time, the interest received from such an allocation of funds is non-operating income and is subject to taxation. But earlier in its explanations, the Ministry of Finance emphasized that, nevertheless, the main criterion for classifying the placement of the balances of earmarked funds as non-commercial activities is the final use of these funds for their intended purpose (Letter of the Ministry of Finance dated 28.03.2008 No. 03-03-06/4/17 ). In particular, such criteria as justification of incomplete use of target funds and minimizing the risk of depreciation of these funds; absence of costs for placing these target funds on deposit accounts were highlighted. In this issue, in our opinion, two problems can be identified. The first problem is actually the complete absence of legislative regulation of this issue. Even the positions of the Ministry of Finance are somewhat different, if we take a certain time interval. If there are no questions about the taxation of interest in the case of deposits, then there are certain issues with the taxation of the placement of the target funds themselves. It is not entirely clear how to justify the expediency of incomplete spending of funds and their placement using a financial instrument. And in general, targeted financing implies the targeted use of the funds received. How, when placing, for example, on the same deposit, to divide these targeted funds and how then to prove their final intended use – the legislator does not answer this question in any way. The second problem, in part, follows from the first. The use of financial instruments to save the target funds, as we have already seen, is very ambiguous and may lead to the need to justify this operation. Donors also have the right to restrict such use of property by the beneficiary. And the misuse of funds leads to the accrual of tax and other possible consequences approved by regulatory legal acts. Consequently, non-profit organizations face tax and financial risks. In conditions of limited and at the same time increasing need for financial resources, the need to preserve available funds, especially with certain macroeconomic instability that has manifested itself in recent years, such complexity and riskiness in using financial instruments limits opportunities for additional financing and development of NGOs in Russia.

There are also problems in the taxation of non-profit organizations with another main tax - VAT. According to Clause 12, clause 3, Article 149 of the Tax Code of the Russian Federation, the gratuitous transfer of TRU within the framework of charitable activities in accordance with Federal Law No. 135-FZ of 11.05.1995 "On Charitable Activities and Volunteerism" is not subject to value added tax. The goals of charitable activity are spelled out in Article 2 of the aforementioned Federal Law and this list is closed. At the same time, it is important to note that charity is absolutely gratuitous. There is another source of income, generally similar to charity. This is sponsorship. The Federal Law "On Advertising" dated 13.03.2006 No. 38-FZ does not allocate restrictions for sponsorship purposes, and it also assumes the provision of advertising services as a mention of the sponsor. That is, based on the definitions given in Article 3 of Federal Law No. 38, it is possible to conclude that the nature of sponsorship is compensated. However, sponsorship can be gratuitous when, for example, the sponsor does not make a condition on advertising its goods, works or services at the conclusion of the contract, but there is a contradiction to the requirements of Federal Law No. 135. The concept of gratuitous sponsorship is not fixed in the legislation and, therefore, the question arises with the inclusion of such income in the VAT tax base. A twofold situation also arises here. In its Resolution, the Federal Antimonopoly Service of the Volga District explained that the nature of the assistance itself is important: if the funds are transferred selflessly and the reimbursable nature of the assistance is not proven, the organization has the right to use the benefit provided for in paragraph 12, paragraph 3 of Article 149 (Resolution of the Federal Antimonopoly Service of the Volga District of 10.11.2005 No. A55-2057/2005-29). On the one hand, such a position seems quite logical and justified: if funds are directed to the implementation of statutory goals, and their transfer is gratuitous, then there are no obstacles to exemption from VAT. However, this question has another interpretation. The very concept of sponsorship, enshrined in the current regulatory legal act, implies compensation in the form of an obligation to provide advertising services - this position is held by the Ministry of Finance (Letter of the Ministry of Finance No. 03-03-06/3/80029 from 9.01.2017). In case of compensation, the sponsorship fee becomes a payment for advertising and is subject to VAT taxation. Thus, the absence of other interpretations of sponsorship in the legislation and the absence as such of the concept of gratuitous sponsorship makes this source of financing less effective, since it becomes an object of taxation and, as a result, the organization loses a sufficiently significant part of it. Of course, sponsorship, if it is gratuitous, can be recognized by an organization as charitable, but in fact there are no justifications from the point of view of the law for this position, and certain difficulties may arise in court. If the gratuitous sponsorship is carried out for the purposes listed in Federal Law No. 135, that is, it meets the criteria of charity, then in order to reduce tax risks, it is worthwhile to carry out such assistance as charitable. Proposals for improving the taxation of NPOs. Within the framework of this study, the author identifies two problems related to the taxation of income of NPOs with VAT and corporate income tax. Let's imagine possible solutions to them. Regarding the issue of investing the organization's target funds in financial instruments, we consider it possible to provide for exemption from taxation of such transactions at the legislative level. Since it is assumed that these funds after the return of investments will still remain targeted and will be used for statutory activities, such an exemption may be provided for in paragraph 2 of Article 251 of the Tax Code of the Russian Federation regulating the exemption of targeted funds from corporate income tax. Regarding the financial instruments themselves, it is advisable to release investments in the least risky of them, because the purpose of an NGO should not be to maximize profits and it is necessary to exclude unjustified risk. Therefore, we consider it possible to release investments of target funds of NGOs in shares and bonds of Russian organizations, as well as their placement on a bank deposit. We believe that the placement of funds on deposit or the purchase of shares does not contradict the concept of a non-profit organization and the goals for which it is created. Moreover, in order to simplify the interpretation of the law, reduce the tax burden and risks, it is possible to consolidate the exemption from corporate income tax not only the amount of investment itself, but also the amount of interest received in the form of profit. The interest received in this case, as well as the invested amount of earmarked funds in general, should be spent only on statutory activities. To do this, we propose to amend paragraph 2 of Article 251 of the Tax Code of the Russian Federation in the form of a new subparagraph 24 and state it in the following wording: funds received by non-profit organizations free of charge to ensure the conduct of statutory activities, invested in shares and bonds of Russian organizations placed on bank deposits, as well as interest on them, subject to the use of the funds received and interest on ensuring the conduct of the statutory activities of non-profit organizations. At the same time, it is necessary to extend the obligation to keep separate records, fixed in paragraph 1 of paragraph 2 of Article 251, and for such income. Otherwise, it will be included in the non-operating income based on the results of the tax period. In our opinion, this initiative will allow non-profit organizations to keep temporarily free earmarked funds, and in case of receiving additional income in the form of interest, also direct it to social and socially useful purposes, thereby fulfilling their main function. The elaboration and implementation of this idea will make it possible to level the existing legislative gap in regulating this issue, simplify the process of investing in NGOs, increase opportunities for financing and conducting statutory activities, while not carrying any significant risks for the state to use the benefits for illegal tax optimization. To justify the introduction of such a benefit, an analysis was carried out based on the accounting data of ten thousand companies unloaded from the SPARK system. According to calculations, in case of exemption of NPOs from corporate income tax on the interest received, the lost budget revenues will amount to less than 800 million rubles, which is 0.012% of corporate income tax receipts to the consolidated budget of the Russian Federation. Thus, the introduction of such a benefit will not be burdensome for the budget. At the same time, for NGOs, these funds make up a more significant part of income. Moreover, if interest income is released, the opportunities for NPOs to invest in the instruments listed above will expand, while creating advantages both for the NPOs themselves and for those in whom they invest.

Let's move on to the next problem of attributing general economic expenses for the purposes of corporate income tax – the most rational seems to be fixing the distribution of clause 1 of Article 272 of the Tax Code of the Russian Federation and separate accounting of NPOs. Despite the absence of concepts of sold and shipped products in the implementation of statutory activities, it is possible to provide a similar procedure for calculating the proportion existing in commercial organizations. It is advisable to add the sixth paragraph to paragraph 1 of Article 272 and state it in the following wording: non-profit organizations have the right to allocate expenses that cannot be directly attributed to expenses exclusively for statutory or entrepreneurial activities, in proportion to the share of income accounted for in accordance with Articles 249 and 250 of the Tax Code of the Russian Federation in the total amount of income. This solution to the problem, firstly, is the easiest to implement, and secondly, it can significantly simplify the situation for taxpayers, because in this case it will be possible to reduce the taxable base for corporate income tax by attributing part of general economic expenses to business expenses. And, of course, it will be possible to resolve the contradiction that arose between the relevant ministries and departments at different times, which created uncertainty and risk for taxpayers. According to calculations made on the basis of accounting statements of various NGOs, the amount of tax risk for commercial and management expenses for 10,000 companies included in the sample formed by the SPARK system is more than 3.7 billion rubles, which is a significant value for non-profit organizations, and the risk itself is not justified by anything. A significant amount of such tax risk confirms the need to introduce the amendment proposed above into the legislation. Consider the issue of value-added tax on sponsorship. As noted above, there are no sufficient grounds for exemption from taxation of sponsorship, if it is gratuitous. There is a certain injustice in this. If we consider, for example, the sphere of physical culture and sports, then for most organizations in this area, sponsorship funds are, if not the key, then a significant source of income. At the same time, for most small sports clubs, especially youth sports, this VAT payment is a rather tangible loss and can lead to underfunding. Based on this, it is necessary to give greater freedom to NGOs and opportunities to generate income and then direct them to these very social goals. In this case, gratuitous sponsorship, if it goes for statutory purposes, may be exempt from taxation. The following application of the proposed mechanism is seen: recognition of gratuitous sponsorship as non-taxable in the part that goes to cover non-commercial expenses. To do this, it is possible to amend Clause 3 of Article 149 of the Tax Code of the Russian Federation in the form of a new subparagraph 12.1 and its presentation in the following wording: transfer of goods (performance of works, provision of services), transfer of property rights to non-profit organizations within the framework of gratuitous sponsorship, if such goods (works, services) and property rights are used by NGOs only in in order to ensure the conduct of statutory activities.In this case, such sponsorship will be an analogue of charity. In order to be exempt from VAT, an NGO will be obliged to spend these funds for statutory purposes and keep separate records. To confirm the right to exemption, sponsorship will need to be issued with the following documents: - sponsorship agreement, which specifies the gratuitousness, voluntariness, goals of assistance and the obligation to use them for these purposes; the act of acceptance and transfer of assistance; - documents on the acceptance of assistance for registration; - the recipient's report on the intended use of the received assistance. In addition, it is advisable to introduce into the Civil Code of the Russian Federation the concept of sponsorship, as well as the contract of gratuitous sponsorship. At the same time, the contract of gratuitous sponsorship should be based on the absence of a counter obligation from the party receiving such assistance. The expediency of such a proposal is seen in the following. Firstly, there is no concept of sponsorship in the legislation of Russia today. The Federal Law "On Advertising" contains only the concepts of sponsor and sponsored advertising, which considers sponsorship only from an advertising point of view and implies retribution (Federal Law No. 38-FZ of 13.03.2006 (ed. of 13.06.2023) "On Advertising"). Secondly, if we consider it from the point of view of gratuitousness, then charitable assistance (in accordance with the Federal Law "On Charitable Activities and Volunteerism" is exempt from VAT) is somewhat narrower than gratuitous sponsorship, because the above-mentioned law contains a closed list of purposes within which charitable activities can be carried out, as well as a restriction on organizations receiving such assistance (Federal Law No. 38-FZ of 13.03.2006 (as amended on 13.06.2023) "On Advertising"). Of course, the organization has the right to spend the sponsorship received for other purposes that are different from the statutory one. However, in this case, it will be necessary to pay value-added tax. On the one hand, this mechanism is simpler, since it is similar to the exemption from VAT of charitable activities in accordance with Clause 12, clause 3, Article 149 of the Tax Code of the Russian Federation, and on the other hand, it will require careful control of separate accounting and primary documentation to avoid using this mechanism for illegal tax optimization. This type of sponsorship will increase the sources of funding for the implementation of its activities, this will be especially sensitive for small organizations, which together are the basis of the social sphere and the socially useful services provided. In order to confirm the gratuitous nature of the expenditure of the sponsorship funds received, NGOs will need to keep separate records, reflecting these transactions in special tax accounting registers (which organizations have the right to develop independently) and allocating the necessary amounts in primary documents, as well as provide an estimate of income and expenses, which will reflect the receipts and expenditures of funds for statutory activities. In addition, it is advisable to provide an indication of the target orientation in the sponsorship agreement. In the future, it is possible to reflect such a clause in the proposed amendment to the Civil Code of the Russian Federation on a gratuitous sponsorship agreement. Conclusion. Non-profit organizations are the most important institution contributing to the development of the social sphere of the country. In Russia today, there are a significant number of inaccuracies and contradictions regarding the application of certain norms of tax legislation, which certainly complicates the work of non-profit organizations, makes their activities more risky and costly, and negatively affects its effectiveness. At the same time, the effectiveness of NGOs is manifested in the achievement of public and social goals. In the Russian Federation today, in fact, a full-fledged mechanism of tax incentives for the development of non-profit organizations has not been built. There are few specially created tax benefits for NGOs today, while the process of obtaining them, and in general conducting business, is very complex and faces many administrative barriers [13]. Therefore, it is necessary to develop and introduce new effective tax measures that can become a driver of the development of the non-profit sector in Russia. The directions of improvement proposed in this article will contribute to the formation of a qualitatively new social sphere capable of meeting the needs of citizens for intangible benefits at the proper level.

References

1. Sinelnikov-Murylev, S., Trunin, I., Goldin, M., et al. (2007). Problems of taxation of non-profit organizations in Russia. Moscow: IEPP.

2. Grishchenko, A.V., Grishchenko, Yu.I., & Chigrakova, N.M. (2017). Debatable issues of tax regulation of non-profit organizations. USUE News, 2, 27-37

3. Doroshina, O.P. (2014). Monitoring of state support of SO NPOs in the mode of tax philanthropy (experience of the Republic of Tatarstan). Research Financial Institute. Financial journal, 3(21), 111-120.

4. Grishchenko, Yu.I. (2016). Specifics of the application of special tax regimes by non-profit organizations. Non-profit organizations in Russia, 2(91), 48–52.

5. Kuzmin, G. V. (2011). Entrepreneurial activity of NPOs: accounting and taxation. Accounting, 4, 45-52.

6. Mukhanova, I.N. (2021). Non-governmental non-profit organizations: accounting and reporting. Journal "Accounting", 8, 119–123.

7. Grantseva, T. G. (2022). Financial and tax support of NGOs in a pandemic: Russian and foreign practice. Economics and management: problems, solutions, 5(125), 208-212.

8. Chikina, A. S., & Oficerov, P.L. (2022). Experience of state support of non-profit organizations of the Ulyanovsk region. Diary of Science, 12(72).

9. Klishina, Yu.E., Uglitskikh O.N. (2015). Trends in the development of the non-profit sector of the economy and the improvement of its financing system. Financial analytics: problems and solutions, 36, 38-48.

10. Duquette Nicolas J. (2016). Do tax incentives affect charitable contributions? Evidence from public charities' reported revenues. Journal of public Economics, 137, 51-69. Retrieved from: https://doi.org/10.1016/j.jpubeco.2016.02.002

11. Bolton P., Mehran H. (2006). An introduction to the governance and taxation of not-for-profit organizations. Journal of Accounting and Economics, 41, 293-305. Retrieved from: https://doi.org/10.1016/j.jacceco.2006.06.001

12. Mityukova, E.S. (2022). Non-profit organizations: legal regulation, accounting and taxation. Moscow: AiSi Publishing House, 5.

13. Medvedeva, N.V. (2018). Non-profit organizations in Russia: barriers and conditions of development. Sociodynamics, 4, 12-20.

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the study, based on the formulated title, is the development of tax incentives for non-profit organizations. The stated topic has been partially disclosed, which will be described in more detail in the following paragraphs of the review. The research methodology is based on the study of scientific literature, current legislation and statistical data. It is very valuable that the author uses a graphical method of presenting the results of the study. It would also be good to show clearly: how is tax incentives being implemented now? How did it develop? what does the author suggest to improve it? This scheme would be in great demand among a wide range of readers. And this would ensure that the content corresponds to the stated research topic. The relevance of the research is beyond doubt and is associated with the fact that the implementation of scientific work on the stated topic will be useful both for scientists dealing with these issues, and for educational purposes, and within the framework of directly ensuring the development of the activities of non-profit organizations in the Russian Federation. Scientific novelty is partially present in the material submitted for review, but the author's judgments require justification and quantitative assessment of the feasibility of their implementation. Style, structure, content. The style of presentation is scientific in terms of the absence of colloquial expressions and journalistic phrases. The structure of the article is built by the author, contributes to the qualitative disclosure of the topic. Attention should be paid to the need, firstly, to demonstrate the development of tax incentives (for example, by building a diagram where this process will be visible and what adjustments does the author propose to make?). Secondly, the author proposes to exempt from taxation a number of transactions carried out by non-profit organizations. How much of the shortfall in income will arise from the budgets of the budgetary system of the Russian Federation? How can it be compensated? The author also "considers it possible to release investments of target funds of NGOs in shares and bonds of Russian organizations, as well as placing them on a bank deposit." Why does the author think so? Where is the quantitative assessment of the consequences of the implementation of this proposal? Similarly, with another proposal – "securing exemption from corporate income tax not only the amount of investment itself, but also the amount of interest received in the form of profit." In conditions of increased limited financial resources and socio-economic turbulence, it is necessary to approach the establishment of new tax incentives with extreme caution. It is this approach that is currently fixed as the basic one at the state level, therefore any initiatives to change it must have a financial justification. Otherwise, it looks more like political slogans than a scientific article. At the same time, it should be emphasized separately that the author's ideas may and may even be implemented, but it is unclear from the current version: why? What are the effects of this? (both positive and negative) Bibliography. The author studied 9 sources published in domestic publications, mainly earlier than 2018. The author is recommended, firstly, to study foreign scientific thought on the issues under consideration. Secondly, it should be supplemented with publications published in 2022-2023. This will significantly expand the possibilities for substantiating scientific novelty. Appeal to opponents. The text of the article contains an appeal to the works of other authors as part of a review of sources. It would also be interesting to discuss them with other researchers while improving the quality of the scientific justification of the author's initiatives. This would also increase the depth of scientific novelty. Conclusions, the interest of the readership. Taking into account all the above, we conclude that the chosen research topic is highly relevant, as well as that this article requires editing taking into account the comments indicated in the text. After the comments are eliminated, it will be in demand from a wide range of people.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the reviewed article is tax incentives for non-profit organizations, the presented field of research is new, there are areas in it that need scientific development. The content of the article reveals its title. The presented topic is relevant. The activities of non-profit organizations are becoming even more relevant and important in conditions of high social tension. As a rule, they are focused on improving the quality of life in areas of the economy that have a low income and high social significance, such as social support for the population, healthcare, etc.Currently, there is a high interest of government agencies in connecting the potential of the non-profit sector to solving social policy problems, including improving the quality of social services, their accessibility and variability, and accordingly there is a need to provide systematic support to non-profit organizations. The author uses general scientific and private scientific research methods. The first group includes analysis and synthesis, induction and deduction, and the method of generalization. The second group is represented by the analysis of dynamic series, tabular and graphical methods of presenting information. The author managed to give a general description of the tax field of non-profit organizations, identify the most significant problems of tax incentives for NGOs, and also suggest ways to improve the taxation of non-profit organizations. The analysis of the explanations of the Ministry of Finance and the Federal Tax Service of Russia, judicial practice, which makes it possible to give the article not only scientific, but also practical interest. The study contains elements of scientific novelty, which are presented by the author's scientifically based proposals for improving the system of tax regulation of non-profit organizations in terms of taxation of interest income of NPOs and the specifics of keeping separate records of administrative expenses. The advantage of the work is that the author not only framed his proposals in the form of regulatory proposals, but also made an attempt to economically substantiate the importance of such proposals for NGOs and for the budget by analyzing the reports of NGOs from the SPARK system database. In addition, the official statistics of the Federal Tax Service of Russia and the Ministry of Justice of Russia are presented. The research style is scientific, it is sustained throughout the text of the work. The article is well structured and logically structured. It contains the following sections: introduction, literature review, the system of tax incentives for NPOs, problems of taxation of NPOs, proposals for improving the taxation of NPOs, conclusion. Such a work structure makes it much easier for users to understand and read it. The bibliography is represented by 13 sources of literature, which present both domestic and foreign studies in Russian and foreign languages. The appeal to the opponents is not presented, but the section "Literature review" is independently highlighted. The presented research may be of interest to the readership both from the standpoint of theory and from the standpoint of practice.

|