|

Taxes and Taxation

Reference:

Tikhonova A.V., Zas'ko V.N.

Economic effects of changes in VAT rates in Russia

// Taxes and Taxation.

2023. ą 4.

P. 39-53.

DOI: 10.7256/2454-065X.2023.4.43537.2 EDN: VUCXDL URL: https://en.nbpublish.com/library_read_article.php?id=43537

Economic effects of changes in VAT rates in Russia

Tikhonova Anna Vital'evna

ORCID: 0000-0001-8295-8113

PhD in Economics

Associate Professor, Leading Researcher, Department of Taxes and Tax Administration, Financial University

127083, Russia, Moscow, Verkhnyaya Maslovka str., 15, room 507

|

samozvanka_89@bk.ru

|

|

|

Other publications by this author

|

|

|

Zas'ko Vadim Nikolaevich

Doctor of Economics

Dean of the Faculty of Taxes, Audit and Business Analysis, Financial University

15 Verkhnyaya Maslovka str., Moscow, 127083, Russia

|

|

VNZasko@fa.ru

|

|

|

|

DOI: 10.7256/2454-065X.2023.4.43537.2

EDN: VUCXDL

Received:

09-07-2023

Published:

05-09-2023

Abstract:

The subject of the study is the effects of reforming the value added tax. In particular, the authors analyze the economic consequences of an increase in the VAT rate from 18 to 20% in 2020. The following effects are assessed: inflationary, consumer, investment and budgetary. The results are compared with the conclusions obtained earlier by domestic and foreign scientists on the example of developed and developing countries of the world. As research methods, analysis and synthesis, tabular and graphical methods of data visualization, analysis of time series, comparison method, structural and trend analyzes are used. The study contains a number of methodological limitations, which are also consecrated in the work. A special contribution of the authors to the study of the topic is the expansion of the zones of influence of indirect taxation on business and the population. In particular, the authors conclude that despite the presence of a number of negative effects of the increase in the VAT rate for business, nevertheless, such negative effects are most pronounced in relation to the population. They consist in accelerating inflation and reducing consumption in the short term. At the same time, the hypothesis of a significant impact of the VAT rate on investment processes is refuted, which is substantiated by an analysis of the indicators of the investment activity of economic entities in Russia.

Keywords:

tax, VAT, consumption, VAT reform, the tax burden, tax neutrality, tax fairness, tax effects, tax regulation, indirect taxes

Introduction

The popularity of VAT is due to its characteristics of tax neutrality and avoidance of double taxation, as well as, more importantly, its role as an effective means of tax administration. Value added tax is not only a budget-forming payment that performs an important fiscal role, but also a significant economic regulator.

The high regulatory potential of VAT is ensured by the fact that a whole chain of counterparties from producers of resources and means of production to end consumers participates in the process of creating added value in the production of goods, works, services (hereinafter TRU). Since the purchases of one firm are sales of another, the buyer's tax evasion by understating or failing to provide information about purchases may make it difficult for the seller to understate or fail to provide information about sales, since the same transaction in intercompany trade is registered on both sides in the form of incoming and outgoing VAT. All elements of such a chain are interconnected through the mechanisms of accrual and deduction of tax, and therefore, by transforming individual elements of this payment, the state affects the entire chain of counterparties to varying degrees. Thus, VAT naturally has the properties of self-fulfillment. Table 1 below shows the potential impact of individual VAT calculation mechanisms on economic agents.

Table 1 – Matrix of the impact of individual VAT calculation mechanisms on economic agents

|

|

Producer of raw materials – Processor

|

Processor – Wholesale Buyer

|

Wholesale Buyer – Retail Buyer

|

The seller of TRU is the final consumer of TRU

|

|

|

VAT exemption

|

Reducing the tax burden on business, simplifying accounting (with full exemption) – manifest themselves when targeting the retail consumer.

When trading to VAT payers, it complicates the search for sales markets.

|

Reducing the cost of TRU for consumers

|

|

|

Rate increase

|

Rising prices, accelerating inflation

|

|

Increasing the tax burden

|

Demand reduction

|

|

|

Rate reduction

|

Reducing the tax burden

|

Increasing demand

|

|

|

Application of tax deductions

|

VAT is paid only from a part of the value created by a specific participant in the production chain, when exporting – state support for exporters, when building for their own needs – investment promotion

|

Reduction of the final cost of the product

|

|

|

Zeroing the bid

|

When exporting: avoidance of double taxation, in other cases – reduction of the tax burden, stimulation of production, VAT refund in the form of state financial support

|

Increasing demand

|

|

Source: compiled by the author himself.

Within the framework of this study, we will analyze the emerging effects of a number of these areas, paying attention, first of all, to the change in the tax rate within the framework of the Russian reform 2018-19.

Literature review

The issues of assessing the effects of changes in the value added tax do not lose their relevance in the research of domestic and foreign authors. Traditionally, research has focused on the impact of indirect taxes on consumers through the impact on prices. At the same time, most of the work is devoted to the study of the impact of changes in VAT rates. In a number of works, various coefficients of the transfer of VAT changes to prices are estimated [1, 2], and in some of them an important asymmetry in the effects of increasing and reducing VAT rates is documented [3, 4]. Thus, the work of Mexican scientists reveals the effects of a reduction in the VAT rate of 16 to 8% on the country's northern border with the United States in 2019 [5]. According to the authors' calculations, the reduction in the VAT rate led to a decrease in the consumer price index by 2.57%, this effect manifested itself quickly within one month. A similar decrease in inflation with a drop in the VAT rate was also revealed in a domestic study by Elkina M.A. [15]. In turn, the assessment of the effects of the VAT rate increase in 2019 by Russian scientists showed the following trends: a decrease in the purchasing power of the population, an increase in inflation [6].

Recent studies of the application of consumption taxes show that they have a direct impact on results that go beyond prices, such as corporate profits, investments, innovations. VAT differs from direct corporate taxes in terms of its potential impact on business, since it is a turnover tax, which, in accordance with classical economic views, has the characteristics of tax neutrality. However, VAT is not always completely neutral for a number of reasons [7]. Firstly, not all enterprises can carry out a full transfer of the tax burden through various market operations, which makes VAT non-neutral. Moreover, VAT is more likely to affect the operating activities of enterprises, the demand for products and cash flows and, ultimately, will affect the size and duration of debt financing. The effects of the VAT rate increase in 1995 [8] and 2014 [9] were estimated on the example of Mexico. In the work of Aportel and Werner, a number of effects (not only price effects) have been studied. Firstly, the VAT increase led to an increase in prices, but this increase was lower than the nominal rate increase. This refutes the conclusion that the VAT increase is fully transferred to consumers. In this context, it is important to take into account the specifics of the national economy, since a similar study on the example of European countries showed [10] that the VAT increase is fully transferred to consumers three months after the tax reform. Secondly, the VAT reform had a negative impact on wages (reduced it by about 2.0%) without affecting the level of employment. A similar reverse effect was revealed by Benzarti and Carloni [11]: the authors show that the wages of employees can increase with a decrease in VAT. Researchers of the Russian Academy of Sciences have found another effect of the impact of the increase in the VAT rate on wages on the example of Russian practice: the total inflow to the country's budget from the increase in the rate amounted to about 800 billion rubles, of which more than half are aimed at increasing public sector salaries, pensions, scholarships, social benefits; infrastructure development, sports, financing of healthcare and education [12]. At the same time, if the purchasing power is limited and price growth is not possible for each of the participants in the chain, an increase in the VAT rate by 2% will affect a decrease in the profitability of each participant in the chain [13].

The impact of the VAT rate on the Chinese economy is different: the reduction of the VAT rate in 2018 significantly reduced the share of borrowed funds and the current debt ratio of enterprises, but did not have a significant impact on the long-term debt ratio. Further research shows that the effect of deleveraging as a result of the reduction in the VAT rate was more significant for state-owned companies with a high share of borrowed funds, small and medium-sized enterprises and companies in eastern China. In western China, the total leverage ratio of enterprises has not undergone significant changes.

Thus, as the review of scientific literature has shown, the impact of the VAT reform is differentiated, it manifests itself not only in pricing policy and inflation, but also in the indicators of financial condition, profit and debt financing of companies. At the same time, the impact of VAT changes on various economic parameters depends on the context of their implementation and the state of the economy not only of a particular country, but also of its region (zone).

Research results

Effect 1 is inflationary. The last significant change in the VAT rate in Russia occurred in 2019, when it was increased from 18 to 20%. Even at the stage of approving the law , analysts of the Central Bank of the Russian Federation noted: "How significant the impact of the VAT increase on inflationary processes will be and how it will be distributed over time depends on various factors from the supply and demand side in the markets of goods and services, as well as on the dynamics of inflation expectations... The assessment of the Bank of Russia included in the June macroeconomic forecast is about 1 percentage point" [14]. Table 1 below shows the dynamics of the consumer price index during the period of VAT rate increase.

Table 1 – Quarterly consumer price indices for goods and services in the Russian Federation in 2005-2023. (quarter to the corresponding quarter of the previous year)

|

|

All products and services

|

of these

|

|

food products

|

of these

|

non-food products

|

services

|

|

food products (without alcoholic beverages)

|

|

2018

|

|

I quarter

|

102,24

|

100,95

|

100,76

|

102,51

|

103,84

|

|

II quarter

|

102,37

|

100,44

|

100,29

|

103,25

|

104,05

|

|

III quarter

|

102,98

|

101,62

|

101,67

|

103,85

|

103,75

|

|

IV quarter

|

103,87

|

103,64

|

103,97

|

104,13

|

103,91

|

|

2019

|

|

I quarter

|

105,16

|

105,77

|

106,31

|

104,57

|

105,09

|

|

II quarter

|

104,99

|

105,95

|

106,49

|

103,94

|

104,99

|

|

III quarter

|

104,29

|

105,04

|

105,49

|

103,49

|

104,31

|

|

IV quarter

|

103,44

|

103,47

|

103,75

|

103,07

|

103,83

|

Source: compiled by the author according to Rosstat.

As can be traced according to Table 1, inflation in 2019 increased sharply, and for food products – almost twice, which most strongly affects the reduction in purchasing power. It is important to note that this effect has been achieved despite the fact that 33% of the population's spending is on goods and services that are taxed at preferential VAT rates [14]. Similar reverse inflationary effects when the VAT rate was reduced from 20 to 18% in 2004 were revealed by Elkina M.A.: reduction of the standard VAT rate and the abolition of sales tax (with an effective rate of about 4%) in early 2004 led to a reduction in inflation by 0.6–0.7 percentage points, while the effect of the transfer was quite distant from the full, and a significant part of the benefits from tax cuts were received by producers and sellers of products, not consumers [15]. It is necessary to agree with the author in this context, since the reduction of rates is considered an element of increasing the fairness of taxation only if the tax reduction is fully transferred to consumer prices. However, in practice, manufacturers do not always transfer a full VAT reduction to the consumer. Otherwise, such a reduction in VAT is considered as an indirect subsidy to producers, which does not directly affect the demand for goods and increase its availability.

Effect 2 – budget. It is possible to justify the government's decision to raise the VAT rate as effective with a significant budgetary effect, since this aspect was the reason and was fundamental in promoting the reform (Table 2).

Table 2 – Budget effect of increasing the VAT rate in 2019, billion rubles.

|

|

2018

|

2019

|

2020

|

Growth rates 2020/18, %

|

|

consolidated budget

|

federal budget

|

consolidated budget

|

federal budget

|

consolidated budget

|

federal budget

|

consolidated budget

|

federal budget

|

|

Budget revenues

|

37320

|

19454

|

39498

|

20189

|

38206

|

18719

|

102,4

|

96,2

|

|

VAT on TRU sold in Russia

|

3575

|

3575

|

4258

|

4258

|

4269

|

4269

|

119,4

|

119,4

|

|

VAT on goods imported into Russia

|

2442

|

2442

|

2838

|

2837

|

2934

|

2934

|

120,1

|

120,1

|

|

The share of VAT in the budget revenues of the corresponding level, %

|

16,12

|

30,93

|

17,96

|

35,14

|

18,85

|

38,48

|

|

|

Source: compiled by the author according to the Ministry of Finance of Russia.

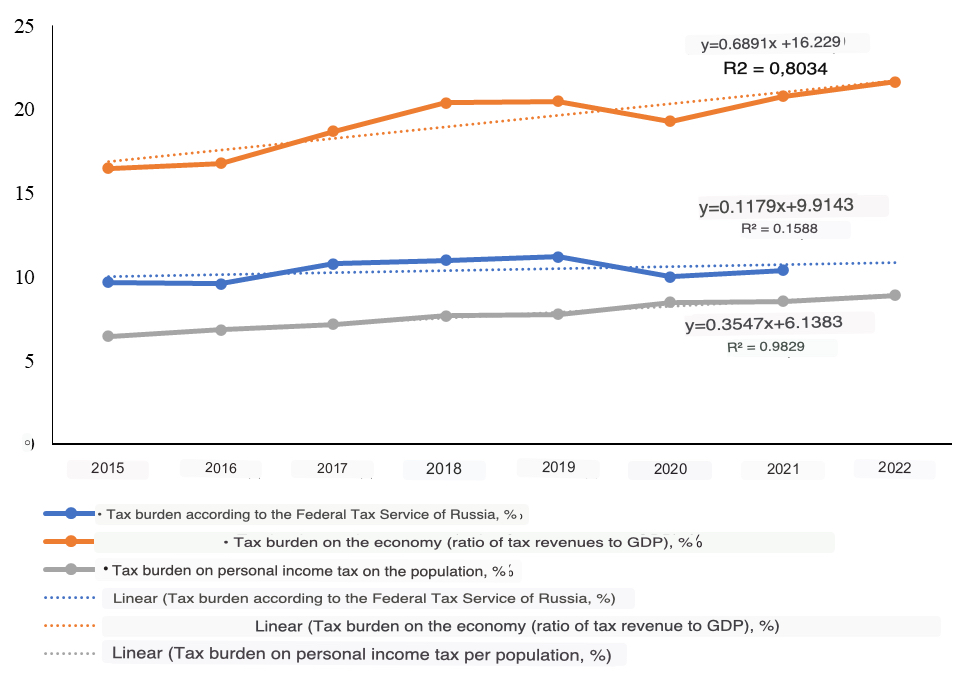

The increase in the VAT rate has led to a positive effect for the budget, the growth rate of tax revenues has increased by 20% over 3 years, despite the negative consequences of the pandemic that have already manifested in 2020. They largely exceeded the growth of consolidated budget revenues. It is important to take into account the impact of the tax rate on business (Figure 1).

Source: compiled by the author according to Rosstat and the Federal Tax Service of Russia.

Figure 1. Dynamics of tax burden indicators during the sanctions period

The data in Figure 1 show the absence of a significant increase in the tax burden on business in 2019 compared to 2018, which indicates the absence of a sharp negative impact of the VAT rate on producers, at the same time, the question arises about the nature of such an impact on consumers of labor.

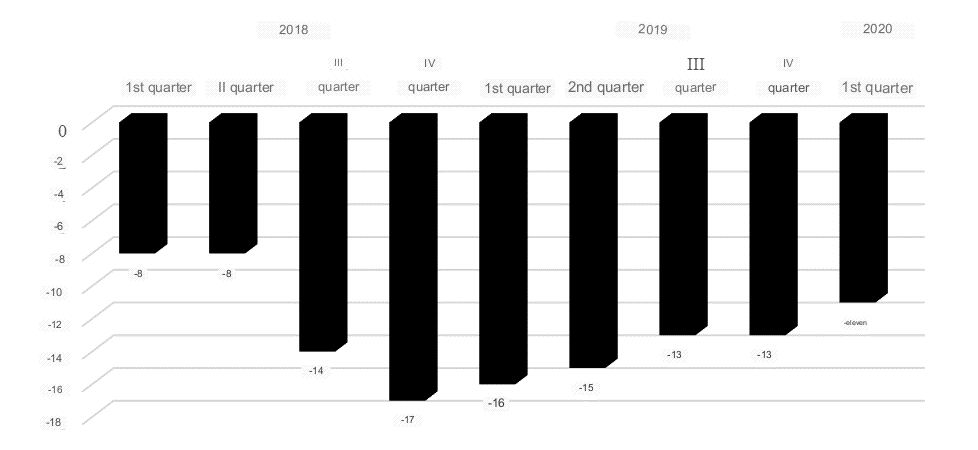

Effect 3 – consumer. One of the manifestations of the regulatory role of VAT is a possible reduction in consumption volumes with an increase in tax rates, which was revealed in the framework of a review of the scientific literature. To assess the impact of the VAT rate on consumer preferences, we will analyze the dynamics of the consumer confidence index, which characterizes the degree of optimism of the population about the state of the economy, which is expressed through consumption and saving (Figure 2).

Source: compiled by the author according to Rosstat and the Federal Tax Service of Russia.

Figure 2. Dynamics of the consumer confidence index

As the data in Figure 2 show, a significant decrease in the index (almost 2 times) occurred in the 3rd quarter of 2018, it was during this period (July 2018) that an increase in the VAT rate from 18 to 20% was announced. At the same time, the index stabilized only by the 1st quarter of 2020.

The volume of consumption is estimated through the index of the physical volume of retail trade turnover, which decreased on average in Russia in 2019 compared to 2018 by 0.9 percentage points (with the maximum drop in the Republic of Ingushetia by 7.6 percentage points and the maximum growth in the Republic of Dagestan, where extremely low index values were obtained in 2018 - by 10.8 At the same time, in 27 subjects of the Federation, the growth rate of physical trade turnover in retail in 2019 did not exceed one percent.

Effect 4 – investment. The assessment of investment effects can be carried out through the analysis of the system of indicators characterizing investment processes and investment attractiveness of the Russian economy (Table 3).

Table 3 – Indicators of investment activity results in 2018-19

|

Indicator

|

2018

|

2019

|

Growth rates,%

|

|

Gross savings, billion rubles.

|

30 050,3

|

29 172,2

|

97,1

|

|

Gross accumulation, billion rubles.

|

22 764,5

|

24 862,4

|

109,2

|

|

Commissioning of fixed assets (at full book value)

|

|

|

|

|

billion rubles .

|

14 907,9

|

22 508,8

|

151,0

|

|

as a percentage of the previous year (in constant prices)

|

114,6

|

104,0

|

H

|

|

The coefficient of renewal of fixed assets (in constant prices), %

|

4,7

|

4,7

|

100,0

|

|

Investments in fixed assets, billion rubles.

|

17782

|

19329

|

108,7

|

|

Consolidated index of prices for products (costs, services) for investment purposes, %

|

107,3

|

105,1

|

H

|

Source: compiled by the author according to Rosstat.

According to the data presented, in general, the investment situation in 2019 is positive: there is an increase in gross accumulation (even despite a decrease in its source – gross savings by 2.9%), the volume of fixed assets introduced and investments in fixed assets. The growth rates of prices for investment products became lower in 2019 compared to 2018. Thus, on the scale of the entire economy, the negative impact of the VAT rate increase on investment processes has not been revealed.

At the same time, it is important to take into account that the existing types of economic activity are heterogeneous in terms of contribution to GDP and value creation. In particular, V.G. Panskov argues that an increase in the VAT rate will have the most negative impact on the state of high-tech sectors of the economy with higher wages [16]. Moreover, from the point of view of the role of VAT, individual foreign economic activities and industries are exempt from taxation either completely or in a significant part (for example, the financial sector, education, medicine, etc.). Therefore, the assessment of the investment effects of the VAT rate increase should be carried out in the sectoral context (Table 4).

Table 4 – Commissioning of fixed assets, billion rubles.

|

|

Commissioning of fixed assets

|

Growth rates, %

|

|

2018

|

2019

|

2019/2018

|

|

Total

|

14 907,9

|

22 508,8

|

151,0

|

|

agriculture, forestry, hunting, fishing and fish farming

|

700,5

|

719,9

|

102,8

|

|

mining

|

2 965,9

|

3 085,4

|

104,0

|

|

manufacturing industries

|

1 855,0

|

2 197,7

|

118,5

|

|

provision of electric energy, gas

and steam; air conditioning

|

1 164,0

|

1 013,0

|

87,0

|

|

water supply; sanitation, organization of waste collection and disposal, pollution elimination activities

|

221,0

|

121,7

|

55,1

|

|

Construction

|

445,4

|

459,9

|

103,3

|

|

wholesale and retail trade; repair of motor vehicles and motorcycles

|

550,5

|

560,9

|

101,9

|

|

transportation and storage

|

2 644,0

|

2 985,7

|

112,9

|

|

activities of hotels and catering establishments

|

89,1

|

86,1

|

96,6

|

|

information and communication activities

|

465,6

|

568,6

|

122,1

|

|

financial and insurance activities

|

830,8

|

1 025,7

|

123,5

|

|

real estate operations

|

1 131,0

|

7 472,2

|

660,7

|

|

professional, scientific activity

and technical

|

428,3

|

482,6

|

112,7

|

|

administrative activity

and related additional services

|

141,0

|

216,5

|

153,5

|

|

public administration and military security; social security

|

672,8

|

839,4

|

124,8

|

|

Education

|

213,5

|

240,4

|

112,6

|

|

health care activities

and social services

|

242,6

|

268,5

|

110,7

|

|

activities in the field of culture, sports, leisure and entertainment

|

111,9

|

136,7

|

122,2

|

|

provision of other types of services

|

35,0

|

27,9

|

79,7

|

Source: compiled by the author according to Rosstat.

In general, the bulk of industries developed investment activities after the VAT rate increase, with the exception of housing and communal services, hotels and catering, as well as other types of services, where there is a decrease in the volume of fixed assets introduced in 2019 compared to 2018. Thus, the significant impact of the increase in the VAT rate from 18 to 20% in Russia on the investment activity of companies in the sectoral context has also not been revealed.

Limitations of the research methodology.

The limitations of this study consist in the absence of separation of the identified effects from various potential sources of their occurrence. The authors consider the economic effects provided that the influence of other factors that are not included in the assessment of the VAT reform is "frozen". This is due to the fact that global economic shocks (financial crises, pandemics, etc.) are not typical for 2018-19, which could have a significant impact on the analyzed parameters. It is also important to take into account that the extension of the dynamic period for analyzing the long-term effects of VAT changes is also not carried out due to the fact that in 2020 the COVID-19 pandemic had the most important impact on the change in individual economic indicators, this makes it impossible to compare this time period and the period 2018-19.

Conclusions and suggestions.

As the results showed, an increase in the VAT rate leads to a number of economic effects. As a positive effect, it is worth noting the increase in the volume of tax revenues of the budget from this payment, which is ensured, among other things, by high-quality tax control. The identified negative effects should include an acceleration in the rate of inflation, as well as a reduction in the growth rate of TRU consumption in the short term. Thus, the results of this study are consistent with the estimates of research by domestic and foreign scientists in the field of the inflationary impact of VAT. At the same time, the hypothesis of a significant impact of the increase in the VAT rate on the level of the tax burden on the economy and inflationary processes in business was not confirmed (the negative effect is manifested only in the context of certain types of activities).

From the point of view of assessing the joint effects for the state, business and the population, it has the most negative impact on the latter. This negative influence is manifested largely due to the regressive nature inherent in VAT and manifested with a significant decrease in the share of tax in the income of the population with their increase [17]. The potential directions of practical use of the results obtained are the possibility of developing tax policy tools. In particular, based on the results obtained, it seems appropriate to increase the amount of social transfers to the population (pensions, allowances, scholarships) by a multiple when the rates of indirect taxes increase without taking into account the annual inflationary growth, since it is it that bears the greatest losses from this kind of tax reforms.

References

1. Benedek D., Mooij R., & Wingender Ph. (2015). Estimating VAT Pass Through. IMF Working Papers, 15(1). doi:10.5089/9781513586359.001

2. Kosonen T. (2015). More and cheaper haircuts after VAT cut? On the efficiency and incidence of service sector consumption taxes. Journal of Public Economics, 131(C), 87-100.

3. Batista Politi R., & Enlinson M. (2011). Ad-valorem tax incidence and after-tax price adjustments: evidence from Brazilian basic basket food. Canadian Journal of Economics/Revue canadienne d'économique, John Wiley & Sons, 44(4), 1438-1470.

4. Kalinin A. (2019). On the impact of an increase in the VAT rate on the price level. Society and Economics, 9, 95-103.

5. Calderón M., Cortés J., Pérez J., & Salcedo A. (2023). Disentangling the Effects of Large Minimum Wage and VAT Changes on Prices: Evidence from Mexico. Labor Economics, 80, 10229. Retrieved from https://doi.org/10.1016/j.labeco.2022.102294

6. Grigoryeva E.A. (2020). Consequences of increasing the VAT rate for the socio-economic development of the state. Azimut of Scientific Research: Economics and Management, 9, 2(31), 140-142.

7. Melnikova N.P. (2018). Key directions of creating a "smart" tax system and the risks of their practical implementation. Scientific works of the Free Economic Society of Russia, 209, 1, 69-74.

8. Aportela, F., & Werner, A. (2002). La Reforma al Impuesto al Valor Agregado de 710 1995: Efecto Inflacionario, Incidencia y Elasticidades Relativas. Working paper 2002-01 Banco de M´exico.

9. Mariscal R., & Werner A. (2018). The price and welfare effects of the value-added tax: Evidence from mexico. IMF Working Paper WP/18/240, International Monetary Fund.

10. Benzarti Y., & Carloni, D. (2019). Who really benefits from consumption tax cuts? evidence from a large vat reform in franc. American Economic Journal: Economic Policy, 11(1), 38–63.

11. Benzarti Y., Carloni D., Harju J., & Kosonen T. (2020). What goes up may not come down: Asymmetric incidence of value-added taxes. Journal of Political Economy, 128(12), 4438–4474.

12. Budget policy and economic growth in Russia: trends and prospects. IPN RAS.Retrieved from https://ecfor.ru/publication/ byudzhetnaya-politika-i-ekonomicheskij-rost-v-rossii

13. Akhmadeev R.G., Bykanova O.A., & Agapova A.A. (2018). Increasing the VAT rate from 2019: impact on the pricing policy of the taxpayer. Azimut of Scientific Research: Economics and Management, 7, 4(25), 23-26.

14. Report on the assessment of the impact of increasing the basic VAT rate on inflation. (2018, August). P. 2. Moscow.

15. Elkina, M. A. (2019). Reducing the rate of indirect taxes in Russia: assessment of the impact on inflation. Financial journal, 5, 37–49. doi:10.31107/2075-1990-2019-5-37-49

16. Panskov, V.G. (2017). Tax maneuver: how it is seen. Economics and management: problems, solutions, 1, 6, 13-20.

17. Esmurziev, A.M., & Barakhoev A.A. (2019). The regressive nature of VAT as the main drawback of the tax. International Academic Bulletin,5(37), 166-168.

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the study. Based on the title, it seems possible to assume that the article should be devoted to assessing the economic effects of changes in value added tax rates. Familiarization with the text showed that the content of the article corresponds to the title, provided that it is added that it is about the Russian Federation. The current version of the title requires filling in the content with the experience of other countries, and not only with the practice existing in the Russian Federation. Research methodology. The author performs theoretical and practical analysis and synthesis of data. It is valuable that the author presents the results of the study graphically in the form of tables and a drawing. Separately, it should be noted that the author uses econometric tools, which makes it possible to enhance the reliability of the author's conclusions and judgments. The relevance of the study of issues related to the assessment of the economic effects of changes in tax rates on taxes is beyond doubt, because its results can provide a scientific basis for making future decisions regarding tax rates on taxes in order to maximize budget revenues of the budgetary system of the Russian Federation while minimizing harm to stimulate economic growth. There is a scientific novelty in the article. In particular, this is due to the construction of a matrix of the impact of individual VAT calculation mechanisms on economic agents, and to the determination of specific effects from changes in tax rates on taxes. It is important to note that the classification of these effects is quite authorial: inflationary, budgetary, consumer, investment. The obtained scientific results can serve as a foundation for further numerous economic and social scientific research. Style, structure, content. The style of presentation is scientific. The structure of the scientific article formed by the author allows us to qualitatively reveal the issues under consideration. Most of the content of the article is formed at a high methodological level. The concluding part of the article causes comments. Thus, it is argued that "The authors make an assumption about the insignificant influence of other factors that are not included in the assessment of the VAT reform." What is the basis of this author's assumption? It would also be interesting to reflect the potential directions of practical use of the obtained results among a possible readership. Bibliography. The author has compiled a bibliographic list consisting of 17 sources. It should also be supplemented with sources that contained numerical data used in the text of the scientific article, without forgetting to indicate references to them (in the current version of the article, both the first and the second are missing). Appeal to opponents. In the introductory part of the scientific article, the author conducted a qualitative review of the scientific literature. The author is also recommended to discuss the results obtained, taking into account the results of scientific research contained in the sources listed in the literature. Conclusions, the interest of the readership. Taking into account all the above, the article requires small (but important) clarifications, after which it can be recommended for publication. The chosen research topic, as well as the depth of immersion in it, form stable positive prerequisites for a high level of demand for this scientific article among officials of public authorities at all levels of government, as well as in the scientific community.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The economic effects of changes in VAT rates in Russia, Indirect taxes are the most important tool for state regulation of the economy. They have been forming the focus of attention in the research of economists, financiers and tax scientists for a long time, which confirms the high importance of indirect taxes. Sensitivity to changes in VAT rates on the part of businesses, citizens and the state determines the controversial issues of tax impact, neutrality and shifting the tax burden on VAT. The presented article is devoted to the study of the economic effects of increasing the VAT rate in Russia from 01.01.2019 from 18 to 20%. The title of the article generally corresponds to the content. However, let us draw the author's attention to the fact that the article considers one specific change in the VAT rate in Russia - an increase from 01.01.2019 from 18 to 20%, which requires specifying the title. We recommend that the author formulate the title also taking into account the ultimate goal of the research. The article highlights sections with subheadings, which corresponds to the presented requirements of the journal "Taxes and Taxation". In the "Introduction" the author makes an attempt to substantiate the significance and relevance of the chosen research direction. There are no standard elements for "Conducting" scientific articles. The author needs to supplement the Introduction with such mandatory elements as the purpose, objectives, practical significance, relevance of the study, etc. In the section "Literature Review", the author examines the results of domestic and foreign studies of the economic effects of changes in VAT rates. The section "Research results" is devoted to a separate assessment of the four economic effects of VAT – inflationary, budgetary, consumer and investment. As a positive effect, the author notes an increase in the volume of tax revenues of the budget. The negative effects include an acceleration in the rate of inflation, as well as a reduction in the growth rate of consumption. In the section "Limitations of the research methodology", the author made the most important remarks on the assumptions of the study – the lack of consideration of other factors (besides changes in the VAT rate) for inflation, tax revenues, investments, as well as on the time constraints of the analysis – for 2 years. The formulated limitations confirm the scientific approach of the author to the study. In the "Conclusion", the author formulates conclusions based on the results of the study. The research uses well-known general scientific methods: analysis, synthesis, comparison, ascent from the abstract to the concrete, logical method, etc. Among the special economic methods, statistical analysis, analysis of structure and dynamics are applied. The relevance of the chosen topic is obvious. Firstly, sufficient time has passed since the VAT rate increase in order to conduct a comparative analysis of its results based on representative data. Secondly, in the context of an increased budget deficit in 2023 due to foreign economic shocks and sanctions pressure, as well as an active search for sources to cover the deficit, the lessons learned from previous tax reforms are particularly relevant. The practical significance of the study seems to be high. However, the author does not explicitly state it in the article. Only in Conclusion is the phrase that the results of the study can be used in the development of tax policy, however, this thesis requires justification and specification – which specific results may have practical significance. The author has not formulated the points of scientific novelty of the study. We believe that the elements of increment of scientific knowledge are present in the article, the article should be supplemented with the author's vision of scientific novelty. This will increase the attractiveness of the research to the general readership of the journal. The style of the article is scientific and meets the requirements of the journal. At the same time, the text is not without some shortcomings and typos, for example, "reducing the VAT rate from 16 to 8%", the heading of table 1 indicates "in 2005-2023", while in the table itself the data are given only for 2018 and 2019. The author actively uses illustrative material, which increases the perception of the research results by readers. The article contains 2 figures and 4 tables. At the same time, the drawings were not included in the layout format of the magazine, so they could not be considered, they were cropped. The bibliography is presented by 17 foreign and domestic sources, which does not meet the requirements of the journal. All sources are referenced in the text of the article. The list of sources needs to be expanded. The bibliographic list should be supplemented with more recent publications, since only 3 publications in the list were published in 2020 or later. The article succeeded in developing a scientific controversy regarding the differences in the results of assessing the effects of changes in VAT rates on the economy. At the same time, the prospects for the development of scientific discourse have a further comparison of the results of assessments by various authors of the VAT increase in Russia since 2019, as well as the assessment of forecasts for 2018 to assess its effects. The advantages of the article include the following. Firstly, the relevance and significance of the chosen research area. Secondly, the high quality of the structuring of the material and the separate study of individual effects. Thirdly, the presence of illustrative material that increases the level of perception of the material by readers. The disadvantages of the article include the following. Firstly, the absence of explicitly formulated elements of scientific novelty, as well as the need to specify the practical significance. Secondly, the need to adjust the "Introduction" section and supplement it with formalized elements. Thirdly, the need to specify the title of the article. Fourth, the need to expand the bibliographic list in accordance with the requirements of the journal. Conclusion. The presented article is devoted to the study of the economic effects of increasing the VAT rate in Russia from 01.01.2019 from 18 to 20%. The article reflects the results of the author's research and may arouse the interest of the readership. The article can be accepted for publication in the journal "Taxes and Taxation" after the elimination of the comments indicated in the text of this review.

|