|

Taxes and Taxation

Reference:

Khyzhak N.

Theoretical and organizational aspects of creating a system of internal tax control of small enterprises

// Taxes and Taxation.

2023. ą 2.

P. 1-20.

DOI: 10.7256/2454-065X.2023.2.39375 EDN: EYHNRS URL: https://en.nbpublish.com/library_read_article.php?id=39375

Theoretical and organizational aspects of creating a system of internal tax control of small enterprises

Khyzhak Natalia

ORCID: 0000-0003-0084-2825

PhD in Economics

Associate Professor, the department of Economics and Finances, Humanitarian and Pedagogical Academy (branch) of V.I. Vernadsky Crimean Federal University

298609, Russia, Republic of Crimea, Yalta, ul. Khalturina, 14

|

shamnp75@gmail.com

|

|

|

Other publications by this author

|

|

|

DOI: 10.7256/2454-065X.2023.2.39375

EDN: EYHNRS

Received:

12-12-2022

Published:

15-03-2023

Abstract:

The subject of the research presented in this article is the theoretical and organizational aspects of creating a system of internal tax control of small enterprises. The author proves that such a system is an effective tool for managing tax risks of organizations to reduce current and potential financial losses of economic entities. The significance and relevance of this issue has been confirmed empirically, including using the latest data from the statistical tax reporting of the Federal Tax Service of Russia. The approach used by the author to the organization of internal tax control is based on the provisions of the COSO methodology, regulatory requirements of domestic legislation and provides for consideration of the specific features of small business entities that affect the procedure for conducting internal control of small enterprises. The criteria of functionality and structural elements of the internal tax control system are defined, their content is described. The approaches proposed by the author to the construction of the internal tax control system are summarized in the form of schemes, algorithms and recommendations that can be taken as a basis for the organization of such work by the heads of small enterprises. The scientific novelty of the research consists in a comprehensive study of the theoretical and organizational aspects of internal control for the development of an internal tax control system and in the application of the conceptual provisions of the theory of internal control to the management of tax risks of organizations, taking into account the specifics of small businesses.

Keywords:

tax risks, tax risk management, internal control, tax control, control environment, internal control procedures, business process, regulations, small business, activity specifics

This article is automatically translated.

The tax legislation of the Russian Federation is based on the recognition of the universality and equality of taxation and defines a tax as a mandatory, individually gratuitous payment levied from organizations and individuals in the form of alienation of funds belonging to them by right of ownership, economic management or operational management for the purpose of financial support for the activities of the state and (or) municipalities (Articles 3 and 8 of the Tax Code of the Russian Federation (hereinafter – the Tax Code of the Russian Federation)) [1]. At the macroeconomic level, a tax is a share of the gross domestic product produced, redistributed by the state in order to implement its functions. From the point of view of microeconomics, a tax is a forcibly alienated part of the income received by business entities in the course of their activities. Thus, as follows from the economic content of taxes, tax relations always have a legally compulsory form. The Tax Code of the Russian Federation defines tax relations as power relations for the establishment, introduction and collection of taxes and fees in the Russian Federation, as well as relations related to taxes arising in the process of tax control, appeals against acts of tax authorities, actions (inaction) of their officials and prosecution for committing a tax offense (Part 1 of Article 2 of the Tax Code of the Russian Federation) [1]. The interests of the participants in tax relations are naturally divergent: taxpayers are interested in reducing tax payments, and the state is interested in increasing tax revenues. Taxpayers are constantly looking for ways to optimize taxes, and tax authorities counteract the minimization of the tax base and tax evasion by enterprises, in connection with which they exercise tax control and bring to responsibility for committing tax offenses. The results of the control work of the Federal Tax Service of the Russian Federation (FTS of the Russian Federation) for the last 6 years are characterized by the following statistical data (Table 1). Table 1 – Results of the control work of the Federal Tax Service of the Russian Federation | | 2017. | 2018. | 2019. | 2020. | 2021. | 9 months. 2022. | | 1. Desk checks | | | | | |

| | 1.1 conducted in-house inspections, units. | 55 859 903 | 67 889 988 | 62 843 726 | 61 542 147 | 58 894 309 | 41 952 247 | | of these, effective, units. | 3 014 252 | 3 529 830 | 2 442 064 | 2 382 858 | 2 975 430 | 1 852 462 | | 1.2 additional payments, including tax sanctions and penalties, million rubles. | 61 599, 4 | 55 103,6 |

37 733,4 | 52 518,5 | 89 272,8 | 63 116,1 | | of these, tax sanctions and penalties, million rubles. | 19 746, 9 | 18 976,0 | 16 249,3 | 17 304,5 | 24 776,5 | 19 662,2 | | 2. On-site inspections2.1 conducted on-site inspections of organizations, sole proprietors, persons engaged in private practice, units. | | | | | | | | |

19 391 | 13 753 | 9 077 | 5 934 | 7 765 | 7 740 | | of these, those who revealed violations, units. | 19 134 | 13 452 | 8 704 | 5 658 | 7 429 | 7 423 | | 2.2 additional payments, including tax sanctions and penalties, million rubles. | 309 782,6 | 313 353,6 | 298 309,3 | 195 923,9 |

382 777,7 | 533 155,4 | | of these, tax sanctions and penalties, million rubles. | 88 376,0 | 91 711,4 | 88 187,6 | 60 464,4 | 124 951,6 | 181 433,1 | | 3. Total additional accrued payments based on the results of tax audits, million rubles. | 371 382,0 | 368 457,2 | 336 042,7 | 248 442,3 | 472 050,6 | 596 271,5 | Source: compiled by the author based on [2-7] The effectiveness of the control activities of the tax authorities of the Russian Federation can be assessed by indicators reflecting the share of tax audits during which tax offenses were detected in the total number of inspections conducted (by type). The annual performance indicators of tax audits calculated according to Table 1 are shown in Figure 1.Figure 1 – The effectiveness of the control activities of the tax authorities of the Russian Federation (compiled by the author on the basis of [2-7])

To assess the "financial results" of tax audits for the budgets of the parties to tax legal relations, it is necessary to operate with the values of specific (for 1 effective audit) additional tax payments. On the one hand, this indicator characterizes the quality of tax administration, and, on the other, the level of tax literacy and tax planning of taxpayers, their attitude to tax risk management. The indicators calculated according to Table 1 are shown in Figure 2.Figure 2 – Financial results of the control activities of the tax authorities of the Russian Federation (compiled by the author on the basis of [2-7])  The calculated indicators show that the desk inspections carried out by the tax authorities in the period under review have a low performance indicator with an increase in the amounts of additional accrued payments per one such audit. The increase in additional amounts accrued based on the results of desk inspections (inspections of documents submitted to the tax inspectorate) is the result of an increase in the number of errors and contradictions made by taxpayers when maintaining tax records and filling out tax returns.The effectiveness of on-site tax audits conducted over the same period is already at least 95% and the unit charges for one effective on-site tax audit amount to tens of millions of rubles. In general, this is understandable, since according to the "Concept of the on-site tax Audit Planning System" adopted in the Russian Federation [8], on-site tax audits are carried out only in relation to taxpayers whose activities are characterized by high tax risks. It also draws attention to the fact that in recent years there has been a steady trend of growth in the amounts of additional payments (including tax penalties and penalties) on average per check. Thus, the "financial result" of one on-site tax audit grew annually with a growth rate of 35%, as a result of which additional charges for one effective tax on-site audit increased by 4.4 times in the first 9 months of 2022 to the same indicator for 2017 to 71.2 million rubles on average. And it depends not so much on the competence and professionalism of the taxpayer's staff, as on the legality of the business operations carried out by the taxpayer and the accepted methods of tax optimization. In just 9 months of 2022, the tax authorities of the Russian Federation, when conducting tax audits of all types, credited a record amount of 596.3 billion rubles to the audited persons. At the same time, based on the actual structure of additional charges based on the results of tax audits (Figure 3), it can be seen that more than a third of the additional accrued payments for 2017-2021 and 9 months of 2022 are penalties for violating the tax legislation of the Russian Federation, which are direct business losses.  Figure 3 – The structure of additional payments based on the results of inspections of the tax authorities of the Russian Federation (compiled by the author on the basis of [2-7]) Thus, the size of the consequences of illegal tax optimizations and errors for the audited persons is growing and negatively affects the financial stability of enterprises and organizations, which is especially critical in today's economic realities. It follows from the above that any business entity should understand the causes of losses in the field of taxation and have appropriate tools and techniques to prevent and reduce them.The solution of this task requires the development and implementation by all taxpayers of a tax risk management system that relates to financial risks, that is, risks that ultimately cause the loss of financial resources. First of all, the probability of loss of financial resources for the taxpayer arises as a result of the actions of the taxpayer, his behavior and accepted methods of tax optimization. Their result is often a violation of tax legislation by the taxpayer (tax offenses), for which sanctions are provided, which are established and applied in the form of monetary penalties (fines) (Article 114 of the Tax Code of the Russian Federation) [1]. Also, losses of financial resources in the form of lost profits and an increase in the tax burden may arise due to the taxpayer's failure to use tax planning opportunities. These factors are attributed to internal factors affecting the magnitude of tax risks, and among the causes of their occurrence are distinguished [9]: 1) the mentality and way of thinking of the Russian taxpayer; 2) organizational aspects, expressed in the low level of organization of the tax management culture in commercial structures; 3) insufficiently responsible attitude of the head of a commercial structure to the problems of taxation; 4) insufficient professionalism of management and accounting personnel, which negatively affects the quality of accounting and tax accounting; 5) incorrect perception of risk by managers and accountants, due to their tendency to make insufficiently informed decisions, or with excessive caution; 6) negative perception by Russian taxpayers of tax authorities. In addition, a decrease in the financial potential of taxpayers may arise due to the uncertainty of the taxpayer's operating environment: for example, due to changes in tax legislation or possible actions (inaction) of tax authorities in relation to the organization during the implementation of control measures. Despite the fact that the taxpayer cannot directly affect the tax risks caused by external factors (due to their independence from the taxpayer's activities), he must organize monitoring of changes in accounting, tax legislation and judicial practice in order to timely predict the consequences of such changes and precedents on the results of the company's activities.

The essence of tax risks and issues of their management are well studied by modern scientists (the works of V.G. Panskov, L.I. Goncharenko, I.P. Komissarova, E. V. Zamula, I.A. Kuzmicheva, M. I. Migunova, T. A. Tsyrkunova, D.M. Shchekin and others). With the introduction of Section V in the Tax Code of the Russian Federation in 2015 .2. "Tax control in the form of tax monitoring" a new, more progressive form of tax control has appeared in Russia – tax monitoring. Such a preventive control mechanism is, in fact, an effective tool for managing tax risks. Most of the authors [10-14] and the legislator [1, 15] believe that minimizing tax risks is possible through the introduction of a reliable system of internal tax control. In [14], the author proposed the definition of internal tax control – "... it is a process organized by a taxpayer on the basis of independently developed principles and standards of activity in accordance with the current legislation, aimed at identifying, analyzing and minimizing tax risks in tax optimization." The organization of such a process requires the use of certain approaches and techniques. Having studied the legislative and regulatory framework for the implementation of internal tax control, in 2016, domestic authors formulated the main problems of its organization in the Russian Federation [13]: – the presence of gaps (ambiguities and contradictions) in the tax legislation; – ambiguity of the process of development and functioning of the internal tax control service; – lack of methodological recommendations (materials and manuals). At the moment, the only official methodology of internal tax control is contained in a document that was developed and approved by the Federal Tax Service of the Russian Federation in the development of tax monitoring – in the Requirements for the organization of the internal control system [15]. It should be noted that the Tax Code applies the application of tax monitoring only to large and a number of medium-sized enterprises: Part 3 of Article 105.26 of the Tax Code of the Russian Federation establishes restrictions on the application, which determines the circle of persons who must apply these Requirements to the organization of the tax control system. At the same time, the study of the provisions of this document allows us to draw the following conclusion: the stipulated requirements, formats and procedures cannot be used by small business entities without adapting approaches to the specifics of the functioning of small enterprises. Therefore, clarifying the theoretical and organizational aspects of tax risk management, taking into account the specifics of SMEs, in order to create a system of internal tax control of such enterprises is an urgent task. Small business entities are characterized by a number of specific features that affect the procedure for conducting internal control. In particular, the control environment in small enterprises differs from larger organizations in that: - persons responsible for the management of small enterprises may not include independent or external members; - the separation of powers of employees responsible for accounting and reporting is limited or absent; - audit evidence for elements of the control environment may not be available in documentary form, in particular, due to the fact that communication between management and other personnel is informal; - the management role can be assumed directly by the owner, who often does not have the necessary competencies; - the influence of the owner and (or) the sole head on all aspects of the activities of a small enterprise is predominant. The predominant influence of the owner and (or) the sole head on all aspects of the activities of a small economic entity can have both a positive and a negative impact on the internal control system and the reliability of accounting statements of such an entity. On the one hand, the personal control of the head can contribute to improving the reliability of accounting of an economic entity in a situation where alternative means of internal control are difficult or impossible for objective reasons. On the other hand, the predominant influence of the manager may contribute to the violation of generally established control procedures, increase the risk of violation of legislation, and contribute to the appearance of intentional material misstatements of accounting statements [16]. Also, in the Rules (Standard) of Auditing activities "Audit features of small economic entities", such potential risk factors are highlighted [16]: a) accounting records may be kept irregularly, without consistent compliance with formal requirements, may not reflect the real state of affairs, which increases the risk of misstatements of accounting statements; b) managers of an economic entity may mistakenly assume that during an audit involving the issuance of an audit opinion, the audit organization will additionally provide services for the restoration of accounting, correction of errors, preparation of accounting statements; c) due to the smaller number of accounting employees than in other economic entities, for objective reasons, it is impossible to ensure proper separation of their responsibilities and powers; d) in the conditions of small economic entities, a situation is possible when accounting employees simultaneously have access to such assets of an economic entity that can easily be hidden, seized or sold, which may contribute to the occurrence of abuse; e) if a small economic entity carries out a large number of transactions for cash, a situation is possible when revenue is not fixed or understated (in order to violate the requirements of tax legislation), and expenses are overstated (in order to spend as production costs funds aimed at personal consumption of executives); f) with a limited number of accounting staff, regular mutual reconciliation of accounting data is difficult or impossible, which increases the risk of errors and distortions of accounting statements. The regulatory framework for the activities of small businesses also has its own specifics [16]: a) simplified procedure for registration, licensing and certification of small business entities;

b) simplified procedure for submitting state statistical and accounting reports; c) the admissibility of the use (subject to the necessary conditions) by small business entities of independently developed forms for documenting business transactions and submitting accounting forms on forms made independently; d) measures of state support for small business entities that affect their financial and economic activities; e) the influence of the peculiarities of regional and local legislation on the functioning of small economic entities. Among other things, the business of small businesses is often undiversified: activities are carried out within the framework of one type of activity, in a local market with a limited number of suppliers and buyers, on the territory of one municipality, with limited opportunities to hire qualified personnel and attract financing. Therefore, the influence of external and internal factors that determine the risks of a small enterprise, including tax, increases many times. Thus, the specifics of the activities of small enterprises generate specific potential risk factors. At the same time, the legislation assumes the same requirements for all for planning and conducting tax control measures [8]. Therefore, it is necessary that the internal tax control system created at a small enterprise provides full functionality of internal tax control. The functionality of the tax control system should be understood as its following characteristics: - a set of internal tax control processes, procedures and tools ensures understanding and adequate control of tax risks; - the internal tax control system allows timely prevention or correction of tax accounting distortions, ensures the correctness of calculation (withholding), completeness and timeliness of payment (transfer) of taxes, fees, insurance premiums; - the internal tax control system ensures the achievement of the operational and financial goals of the enterprise, including through the use of favorable opportunities in the field of taxation established by law; - the internal tax control system provides information to internal and external users on taxation issues and the tax strategy of the enterprise; - the costs of organizing and operating the internal tax control system are economically justified and rational. Full functionality of internal tax control can be provided only as part of an effectively functioning internal control system. Therefore, the model of internal tax control of a small enterprise should be based on the main provisions of the COSO methodology set out in the documents "Conceptual Foundations of Internal Control" (COSO) (1992-1994) and "Conceptual Foundations of Risk Management of Organizations" (ERM COSO) (2004) [17].The following theses are important for the management in the work on the creation of an internal tax control system [17]: - internal control is a process, a means to achieve an end, not an end in itself; - internal control depends on people. It represents not only policies, guidelines and forms, but also people at all levels of the organization; - internal control can provide management with only sufficient confidence, but not absolute guarantees; - internal control is aimed at achieving goals in one or more separate but overlapping categories; - creation and provision of effective implementation of internal control of the organization – a matter of direct responsibility of the management of the organization; - one of the most important issues addressed by the top management of organizations is determining the amount of risk that the organization is ready to accept and accepts in the course of its activities; - the internal control system should be documented in a format understandable to the inspectors; - the internal control system should function effectively, - procedures for evaluating the effectiveness of the internal control system should operate in the company on a regular basis. In accordance with the ERM COSO methodology, the organization's risk management includes the following key tasks [17]:- determining the level of risk that the organization is ready to take in accordance with its development strategy; - improving the decision-making process to respond to emerging risks; - reduction of the number of unforeseen events and losses in economic activity; - identification and management of the entire set of risks in economic activity. Based on the recommendations of the Ministry of Finance of the Russian Federation contained in the document "Organization and implementation by an economic entity of internal control of the facts of economic life, accounting and preparation of accounting (financial) statements" [18] (based on the COSO methodology), we present the structure of the internal tax control system as a set of processes consisting of five elements (Table 2). Table 2 - Structural elements of the internal tax control system | Element |

Composition and characteristics of the element | | Control environment | - a set of principles and standards of activity of an economic entity that define a common understanding of internal tax control and requirements for internal tax control at the level of an economic entity as a whole | | Risk assessment | - the process of identifying and analyzing tax risks that may affect the reliability of accounting (financial) and tax reporting and the risk of abuse | | Internal control procedures | - actions aimed at minimizing tax risks affecting the achievement of the goals of an economic entity | | Information and communication | - high-quality and timely information that ensures the functioning of internal tax control and the ability to achieve its goals | | Assessment of internal control | - the process of evaluating the effectiveness and efficiency of elements of the internal tax control system (monitoring of internal tax control) and determining the need to change them | The starting point of creating an internal tax control system is the creation of a control environment. To create a high-quality control environment, the head of the enterprise needs to solve several issues. The first issue is the creation of an internal tax control service in the organization. Internal audit and structural and functional form of internal control are distinguished as forms of internal control of the organization [19-21]. The organization of internal control in the form of internal audit is inherent in large and some medium-sized organizations that have a rather complex organizational structure; there are branches and subsidiaries; several types of activities. Internal audit institutions include audit commissions (auditors) whose activities are regulated by the current legislation. This form of internal control is mainly common in joint-stock companies. Enterprises of other organizational and legal forms often do not have an internal audit department and an audit commission. In this case, for the implementation of internal control, it is advisable to use the structural and functional form of internal control of the organization, in which control functions are assigned to existing employees of the organization without allocating them to a structural unit. In general, the current regulatory legal acts [18] do not prescribe the mandatory application of all elements of internal control, including risk assessment, for small businesses. In accordance with article 20 of the Information Letter of the Ministry of Finance of the Russian Federation [18], it is allowed that if any elements of internal control cannot be applied by a small business entity, its head may organize internal control in any other way that ensures the achievement of the goals of the organization and the implementation of internal control. The owner of a small enterprise in this case, when making a decision on the organization and implementation of internal control, should be guided by the requirement of rationality. For example, if the number of employees of an economic entity does not allow for the separation of powers and the rotation of responsibilities, the functions of organizing and implementing internal control can be assumed by the head of the enterprise. Another solution for the organization of internal control in a small business entity may be the transfer of internal control to outsourcing. The second issue that needs to be addressed in order to create a high-quality control environment is the issue of developing internal documents and regulations.

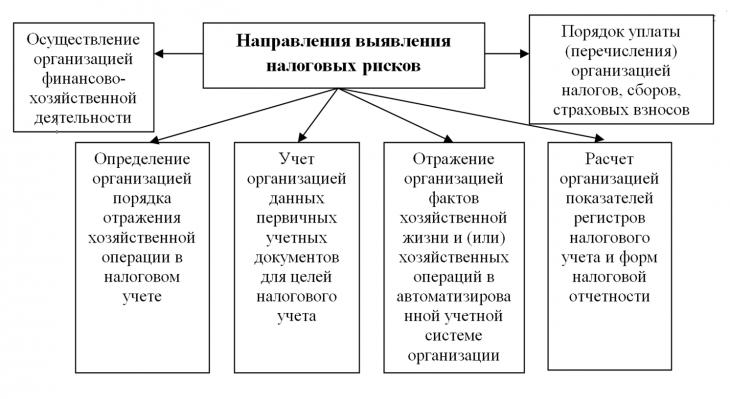

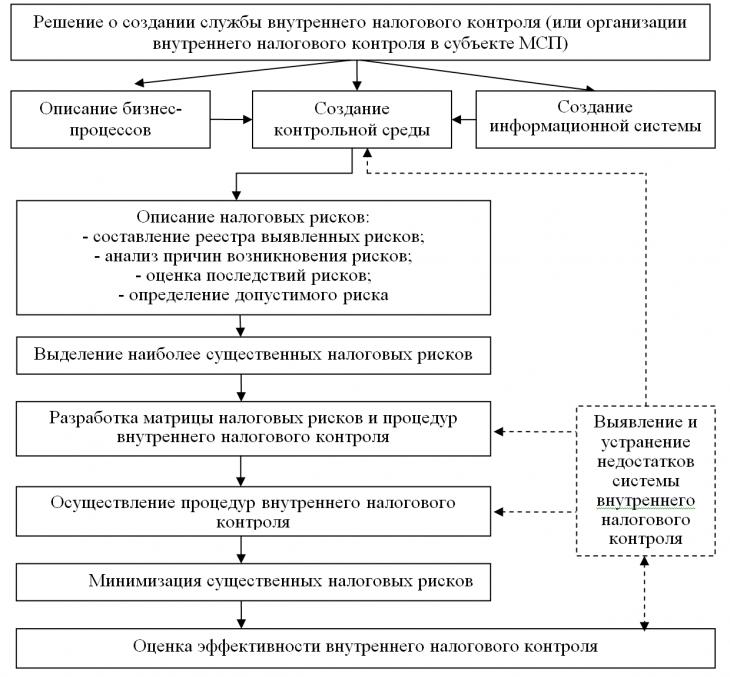

In relation to accounting and tax accounting, including the preparation of accounting (financial) and tax reporting, the control environment can be described by the regulations on the accounting service, the accounting policy of the organization, the tax accounting policy of the organization, the requirements for the qualification of accounting personnel, job descriptions, regulations on information policy in the field of external and internal communications, schedules for the provision of data and reporting, regulations on the conduct of contractual work, other documents that establish general requirements for the environment in which accounting and tax accounting is organized and maintained. When creating a control environment, it is important that the adopted regulations ensure the possibility of conducting: - preliminary internal control; - current internal control; - subsequent internal control; - control of authority; - control of accounting procedures; - control of household funds. Preliminary control is carried out before the start of the economic operation. It involves analyzing the upcoming results of business operations, preliminary approval of contracts or other documents before signing them in order to prevent violations. During the implementation of the current control, the monitoring of the performed business operations takes place. Subsequent control is carried out based on the results of business transactions and is aimed at identifying errors and violations of the established procedure of activity. The subsequent control, in fact, is the verification of documents, accounting registers and reports. As part of the subsequent internal control, the elimination of identified inconsistencies should be organized. The control of authority is aimed at preventing abuse of officials and employees of the organization, limiting inefficient operations, limiting the possibility of making changes to accounts without proper authorization. A person holding a certain position in the organizational structure of an enterprise should clearly know the scope of his duties and have clearly defined powers, which, in turn, are sufficient to perform official duties. The level of responsibility of the official should also be determined. These issues are solved by developing job descriptions, internal regulations on the structural divisions of the organization, approving the list of persons who are allowed to sign documents and authorize business transactions, introducing a password system to restrict access to computer programs used to process information about business transactions. Control of accounting procedures is a group of control measures that are aimed at creating conditions for the correct and timely registration of authorized (authorized and provided for by accounting policy and other internal and documents) accounts (by date, amounts, details). Each agreed and authorized business transaction must be correctly and timely recorded and systematized in the accounting system. Moreover, it is necessary to ensure the correct measurement and evaluation of such an operation. Control of economic assets is a group of internal control procedures that contributes to the preservation of the company's property, limits fraud and other types of abuse of material values. Preparation of regulatory and methodological documents on internal control should be carried out by authorized employees of the organization simultaneously with the description of the business processes of the enterprise. The prepared documents must comply with the requirements of legislation (civil, tax, labor) and reflect the specifics of business processes, operating model and organizational structure of management of a particular enterprise. The main source of information for decision-making is the information systems of an economic entity. An information system is a system of storing, processing, converting, transmitting, updating information using computer and other equipment [22]. The elements of the enterprise information system should include the following components [23]: personnel, special procedures, databases, technical means, software. The completed stages are the basis for documenting risks, assessing them and developing internal control procedures by the enterprise to minimize risks. The development of tools for identifying tax risks of an organization, methods of their assessment and management of tax risks is a block of methodological issues that require separate consideration. Nevertheless, within the framework of the purposes of this article, it is necessary to specify the directions for identifying tax risks and the factors that cause their occurrence, since this is necessary to determine the scope and composition of internal tax control procedures. The directions of identifying tax risks identified in the study [24] are shown in Figure 4.  Figure 4 – Directions for identifying tax risks [24, p.116] Internal control procedures should be divided into two groups: for the accounting and tax accounting system and for the organizational management system (Figure 5).  Figure 5 – Internal tax control procedures (compiled by the author on the basis of [18])

As can be seen, in terms of internal control procedures, no specific methods of internal tax control have been identified. Such a general approach is justified by the fact that both accounting and tax accounting in general are systems for the formation and reflection in documents of systematized information about accounting objects for compiling reports based on these data, with the only difference that within the framework of tax accounting, the subject and objects are narrowed to objects of taxation and obligations for accrual (withholding) and payment taxes and fees. The elements of the accounting method are also common to the two types of accounting: documentation, evaluation and reporting. Guided by the general scheme, each business entity should develop and apply such types and techniques of internal control (or their combination) that will allow achieving the level of acceptable risk. Acceptable risk should be understood as a risk that is considered acceptable in this situation with existing social values. The fundamentals of the security theory, to which the term "permissible risk" refers, are set out in the National Standard of the Russian Federation "Security Aspects" GOST R 51898-2002 [25]. Control actions for neutralization and minimization are applied to those risks that the organization determines to be significant and that will be above the limit of acceptable risk. An obligatory stage of the organization of the internal control system is the assessment of the effectiveness of internal tax control [17, 18]. Internal control assessment should be carried out at least once a year to the extent determined by the head or a person authorized by him, in two directions: - evaluation of the effectiveness of the internal control design; - assessment of the operational effectiveness of internal control. The evaluation of the effectiveness of the internal tax control design of the enterprise assumes: - confirmation of the existence of internal tax control, completeness and correctness of the description of internal control, completeness of internal control coverage of tax risks; - forming an opinion on whether the adopted internal tax control procedures are sufficient to minimize tax risk; - checking whether the description of internal tax control procedures is correct and understandable. The operational effectiveness of internal control means that internal control is carried out continuously throughout the reporting period (without omissions) in full compliance with the approved design. Confirmation of operational effectiveness involves testing a certain amount of evidence of internal control during a period or performing a certain number of repetitions of internal control procedures. In order to ensure the reliability of the information used for internal control, when conducting an internal control assessment, it is necessary to use the same documents and information systems that are used by the company's personnel in their current activities. The results of the internal control assessment should be documented, discussed with the executors of the internal tax control procedures and presented to the head of the enterprise. The volume, composition and forms of documentation are determined by the needs of the economic entity. If necessary (when identifying design flaws or operational effectiveness of internal control), actions are taken to eliminate the identified shortcomings. The above stages of the organization and implementation of internal tax control based on a risk-based approach are summarized in Figure 6 for a visual representation of this process.  Figure 6 – Organization of the internal tax control process in an organization (compiled by the author)The mechanism of functioning of the internal tax control system should be provided with an appropriate methodological basis, which is the subject of a separate study that goes beyond the scope of this article. The internal tax control system created according to the proposed algorithm should function on an ongoing basis, which will ensure the prevention or minimization of the negative impact of events and factors affecting the achievement of financial and operational indicators of the enterprise, and will significantly reduce the likelihood of the risk of information distortion or unreliability of tax accounting data. When creating such a system, taking into account the potential risk factors described in the article, generated by the specifics of the activities of small enterprises, will allow organizing this process as efficiently and efficiently as possible.

References

1. Tax Code of the Russian Federation. Part one: federal law N 146-FZ: adopted by the State. Duma on July 16, 1998 (as of November 21, 2022) // ConsultantPlus: legal reference system [Official. website]. – URL: http://www.consultant.ru/document/cons_doc_LAW_19671/ (date of access: 11/25/2022).

2. Data on the forms of statistical tax reporting. Updated report on the form No. 2-NK as of 01/01/2018, in general for the Russian Federation // Federal Tax Service [Official. website]. – URL: https://www.nalog.gov.ru/rn77/related_activities/statistics_and_analytics/forms/6763053/ (date of access: 11/25/2022).

3. Data on the forms of statistical tax reporting. Updated data of the report in the form No. 2-NK as of 01/01/2019, in general for the Russian Federation // Federal Tax Service [Official. website]. – URL: https://www.nalog.gov.ru/rn77/related_activities/statistics_and_analytics/forms/7430557/ (date of access: 11/25/2022).

4. Data on the forms of statistical tax reporting. Updated report on form No. 2-NK as of 01/01/2020, in general for the Russian Federation // Federal Tax Service [Official. website]. – URL: https://www.nalog.gov.ru/rn77/related_activities/statistics_and_analytics/forms/8753733/ (date of access: 11/25/2022).

5. Data on the forms of statistical tax reporting. Updated report on the form No. 2-NK as of 01/01/2021, in general for the Russian Federation // Federal Tax Service [Official. website]. – URL: https://www.nalog.gov.ru/rn77/related_activities/statistics_and_analytics/forms/9770621/ (date of access: 11/25/2022).

6. Data on the forms of statistical tax reporting. Report in Form No. 2-NK as of 01/01/2022, in general for the Russian Federation // Federal Tax Service [Official. website]. – URL: https://www.nalog.gov.ru/rn77/related_activities/statistics_and_analytics/forms/10924767/ (date of access: 11/25/2022).

7. Data on the forms of statistical tax reporting. Report in Form No. 2-NK as of 01.10.2022, in general for the Russian Federation // Federal Tax Service [Official. website]. – URL: https://www.nalog.gov.ru/rn77/related_activities/statistics_and_analytics/forms/12241965/ (date of access: 11/25/2022).

8. The concept of the planning system for field tax audits: approved. by order of the Federal Tax Service of Russia dated May 30, 2007 N MM-3-06 / 333@ (as of May 10, 2012) // ConsultantPlus: reference and legal system [Official. website]. – URL: http://www.consultant.ru/document/cons_doc_LAW_55729/ (date of access: 11/25/2022).

9. Shepelin, G. I. (2019). Insurance and tax risks of entrepreneurial activity. International Scientific Research Journal, Part 3, 3 (22), 94–97.

10. Goncharenko, L.P. (2009). Tax risks: management theory and practice. Finance and credit, 2, 30-31.

11. Burtsev, V.V. (2002). Internal control: basic concepts and organization of conduct. Management in Russia and Ŕbroad, 4, 35-50.

12. Vasilchuk, E.V. (2012). Issues of developing a model for organizing the system of internal tax control. Bulletin of BelUPK: international scientific and theoretical journal, 1, 371–377.

13. Chukhnina, G.Ya. (2016). Methodology for organizing the system of internal tax control. Finance and credit, 21 (693), 24-38.

14. Khizhak, N.P., Umerov, R.I. (2021). Conceptual issues of managing the tax risks of an organization. In A. V. Olifirova (Ed.), Financial, economic and information support for the innovative development of the region (202-207). Simferopol: IT "ARIAL".

15. Requirements for the organization of the internal control system: approved. Order of the Federal Tax Service of Russia dated May 25, 2021 N ED-7-23 / 518@ // ConsultantPlus: reference and legal system [Official. website]. – URL: http://www.consultant.ru/document/cons_doc_LAW_385613/ (date of access: 11/28/2022).

16. Rules (standard) of audit activity “Peculiarities of auditing small economic entities”: approved by the Audit Commission under the President of the Russian Federation on July 11, 2000 Minutes N 1 // ConsultantPlus: reference and legal system [Official. website]. – URL: http://www.consultant.ru/document/cons_doc_LAW_28978/ (date of access: 10/16/2022).

17. Organizational risk management. integrated model. [Electronic resource] / Committee of Sponsoring Organizations of the Treadway Commission (COSO). – URL: https://www.coso.org/documents/COSO_ERM_ExecutiveSummary_Russian.pdf (date of access: 04/06/2021).

18. Information of the Ministry of Finance of Russia N PZ-11/2013 “Organization and implementation by an economic entity of internal control of the facts of economic life, accounting and preparation of accounting (financial) statements”. // ConsultantPlus: legal reference system [Official. website]. – URL: http://www.consultant.ru/document/cons_doc_LAW_156407/ (date of access: 11/05/2022).

19. Burtsev, V.V. (2002). Internal control: basic concepts and organization of conduct. Management in Russia and Ŕbroad, 4, 35-50.

20. Illarionova, N.Yu. (2013). Internal control: gaps and parallels. Laws of Russia: experience, analysis, practice, 9, 34-43.

21. Parkhomchuk, D.V. (2016). The main functions and types of internal control of the organization. Eurasian Union of Scientists, 1-1 (22), 83-87.

22. Dictionary of terms. [Electronic resource]. – URL: http://economicportal.ru/ (date of access: 11/25/2022).

23. Soboleva, O.A., Bogdanovich, I.S. (2015). Information system as an element of the internal control system of an audited entity. Bulletin of the Pskov State University. Series: Economy. Right. Control, 2, 37-41.

24. Olifirov, A. V. (Ed.). (2022). The mechanism for managing the economic potential of the spatial structure of the region. Simferopol: IT "Arial".

25. GOST R 51898–2002. (2018). State standard of the Russian Federation. Aspects of security. Rules for inclusion in standards. Mîscow.

Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the study. Based on the title formed by the author, the article should be devoted to the theoretical and organizational aspects of creating a system of internal tax control of small enterprises. The content of the article does not reveal the chosen topic, at least due to the lack of specific distinctions between "theoretical" and "organizational" aspects. Also, the text of the reviewed materials does not take into account the specifics of small enterprises. When finalizing the article, attention should be paid to this, including, possibly, correcting both the content and the title. Research methodology. The research, in general, is based on the presentation of well-known facts and judgments without any author's assessment and formulation of his own position on the issues under consideration. At the same time, it is valuable that the author actively uses diagrams to reflect information, which allows you to visually see the processes under consideration. The relevance of the study of the organization of internal tax control is beyond doubt, as it is of great importance for all economic entities: organizations are interested in reducing the tax base, and the state is interested in maximizing funds credited to the budgets of the budgetary system. Scientific novelty. The reviewed materials do not have scientific novelty, despite the presence of a large number of potentially unexplored areas, which hypothetically creates prerequisites for conducting qualitative research. Style, structure, content. The style of presentation is scientific. The article does not have a structure formally defined by the author with a subtitle for each section of the article. It seems that this problem has also affected the content. So, in particular, the text does not contain any problems identified by the author on the range of issues under consideration, as well as ways to solve them. It also requires specifying specific examples of the direction of identifying tax risks (especially considering that the content of the above scheme is borrowed from another source: what is the contribution of the author?), internal tax control procedures (especially considering that the content of the above scheme is borrowed from another source: what is the contribution of the author?). Bibliography. The bibliographic list consists of 25 titles, including scientific publications, regulatory legal acts and electronic resources containing statistical data used in the preparation of materials submitted for review. Given the wide range of issues raised in the scientific literature, it is recommended to supplement the bibliographic list with publications from periodicals. Conclusions, the interest of the readership. Taking into account all the above, the article can be published.

|