|

Finance and Management

Reference:

Akkhuzin, I.I. (2026). Investment cooperation within the BRICS framework as an alternative channel for attracting foreign investment to Russia. Finance and Management, 3, 1–15. https://doi.org/10.25136/2409-7802.2026.3.80327

Investment cooperation within the BRICS framework as an alternative channel for attracting foreign investment to Russia

Akkhuzin Il'ya Igorevich

Postgraduate student; Diplomatic Academy of the Russian Ministry of Foreign Affairs

53/2 Ostozhenka St., Moscow, 119992, Russia

|

ilyaakkhuzin@gmail.com

|

|

|

Other publications by this author

|

|

|

DOI: 10.25136/2409-7802.2026.3.80327

EDN:

QWHXCY

Received:

06/02/2026

First review received: 06/13/2026 04:50 — manuscript returned for revision

Revised manuscript submitted: 06/09/2026 07:41

Second review received: 06/15/2026 04:54 — manuscript returned for revision

Revised manuscript submitted: 06/17/2026 08:42

Final review received: 06/18/2026 17:42 — recommendation for publication.

The article is published in its final version as approved following the last positive peer review recommending acceptance for publication. It incorporates revisions made by the author in response to prior negative peer review reports that did not recommend publication. All peer review reports, including initial negative reviews, are published in open access alongside the article. All versions of the author’s revisions are archived in the publisher’s repository and may be made available upon reasonable request in accordance with Elsevier’s editorial policies and applicable data availability requirements.

Read all reviews on this article

Published:

06/19/2026

Abstract: The article examines the role of investment cooperation within the framework of the BRICS as an alternative mechanism for attracting foreign direct investment into the Russian economy in the face of sanctions pressure, which led to the disruption of its international investment ties. Since 2022, Western countries have practically curtailed their investment presence in Russia or frozen assets as part of sanctions. Under these conditions, the importance of the BRICS association has increased, the participants of which collectively form the largest «non-Western» investment block of the world economy. The study aims to analyze investment cooperation between Russia and the BRICS+ countries, assess its real scale, identify conditions and barriers to its expansion, and identify areas for the development and improvement of public investment policy, taking into account certain problems and key areas of development. The object of the study is investment cooperation within the framework of the BRICS, and its subject is the mechanisms, dynamics and institutional conditions for attracting FDI from the BRICS countries to the Russian economy. The research is based on general scientific methodology, as well as statistical data from national banks, international organizations and analytical centers. According to the results of the study, the BRICS countries are taking an increasingly important position in the global investment space, which means a structural shift in favor of non-Western centers of capital attraction. However, Russia found itself sidelined from this investment dynamic, the main reasons for which were the instability of the BRICS institutional architecture in the face of sanctions pressure and the threat of secondary sanctions. A number of areas have been identified for improving Russia's investment policy in the context of cooperation with BRICS partners (development of special investment regimes, accelerating the formation of an investment settlement infrastructure in national currencies and central securities, partial restructuring of the NBR in relation to the Russian position, and reorientation of investment priorities to technological sectors). Scenarios for further development of investment cooperation in the BRICS-Russia format are presented.

Keywords:

BRICS, foreign direct investment, international investment position, sanctions, New Development Bank, pool of foreign exchange reserves, alternative investment channels, friendly jurisdictions, secondary sanctions, investment cooperation

This article is automatically translated.

Introduction The introduction of sanctions against Russia in 2022 led to the degradation of its international investment ties – the cumulative outflow of foreign capital from the Russian economy over the following years resulted in a reduction in accumulated foreign direct investment (FDI) from $610 billion to $258 billion, that is, by more than half. Western countries, which for a long period provided up to 72% of the accumulated portfolio of incoming FDI, curtailed their investment presence in Russia or froze assets as part of sanctions. In these circumstances, the importance of the BRICS association as a potential platform for redirecting investment flows has increased dramatically. The BRICS countries, including the new members admitted in 2024-2025 (the UAE, Egypt, Iran, Ethiopia and Indonesia) collectively form the largest "non-Western" investment bloc in the global economy: according to UNCTAD, the expanded BRICS (BRICS+) accounts for 22% of global FDI inflows and about 37% of global GDP by PPP. At the same time, questions about the current state and future prospects of Russia's reorientation towards BRICS partners remain a subject of discussion. This study aims to analyze investment cooperation between Russia and the BRICS+ countries, assess its real scale, identify institutional conditions and barriers to its expansion, and identify areas for the development and improvement of public investment policy, taking into account certain problems and key areas of development. The object of the study is investment cooperation within the framework of the BRICS, and its subject is the mechanisms, dynamics and institutional conditions for attracting FDI from the BRICS countries to the Russian economy. The scientific novelty of the study is a comprehensive analysis of investment cooperation in the BRICS-Russia format under the sanctions pressure of 2022-2026. using up-to-date data that had not previously been introduced into scientific circulation within the framework of a single study using an integrated approach that covers both barriers and prospects for the reorientation of Russian investment flows. The results of the study are of interest to experts in the field of global economics and international relations, as well as to government authorities shaping Russia's investment policy in the context of the global transformation of the global financial system. Materials and methods of research. The research is based on a general scientific methodology that includes systematic, institutional and comparative analysis, as well as methods of descriptive statistics and elements of scenario analysis. The empirical basis was statistical data from the Bank of Russia, national banks of the BRICS countries, international organizations (UNCTAD, the Eurasian Development Bank, the New Development Bank) and analytical centers (Oeconomus, wiiw). It should be noted that assessing the actual volume of investment cooperation between the BRICS countries and Russia is fraught with certain methodological difficulties, since, starting in 2022, the Bank of Russia stopped publishing some detailed data, including on FDI, and alternative sources use estimated rather than official data. Thus, the consolidation of these disparate and indirect data is one of the objectives of the study. BRICS as an international investment platform BRICS (English BRICS – short for Brazil, Russia, India, China, South Africa) is an informal association of countries with dynamically developing economies. The idea of such an association was first expressed back in the late 1990s, however, the starting point of the BRICS existence is considered to be 2006, in June of which the association was formally established within the framework of the St. Petersburg International Economic Forum (Brazil, Russia, India, and China were still BRICS), and in September the first meeting of foreign ministers was held. participating countries [1]. In June 2009, the first BRIC summit was held, and in 2011 the Republic of South Africa joined the association, after which it received the familiar name BRICS. Since January 2024, Iran, Egypt, the United Arab Emirates and Ethiopia have joined the BRICS, and at the beginning of 2025 Indonesia joined the BRICS as a full member [2], so at the moment the group includes ten countries (in connection with which, along with the former name, the association can also be designated as BRICS+). Currently, the BRICS does not have the official status of an international organization, legal documents, charter, a specific structure and powers of the participants [2]. Nevertheless, a number of international institutions, including financial ones, have been formed within its framework, and work is underway to modernize and develop economic systems by eliminating restrictions, creating common standards, and de-dollarization. trade operations, development of the transport network and digital infrastructure, etc., including investment cooperation [3]. Various views on the investment potential of the BRICS have been formed in the scientific literature. Some authors, relying on the concept of "South-South investments" (South-South FDI), consider investment cooperation within the framework of the association as an alternative to the Western model of transnationalization, in which BRICS companies act both as donors and recipients of investments, creating "horizontal" capital flows between developing economies, which is considered as a whole a positive phenomenon [4, 5]. Other researchers note the weakness of the contractual and legal framework, in particular, the lack of unified approaches to investment legislation, and the low level of mutual financial integration of the member countries of the association [6, 7]. From the point of view of J. Dunning's OLI (Ownership, Location, Internationalization) concept [8], investment cooperation within the BRICS is characterized by a number of advantages of localization, such as access to resources and markets at relatively low transaction costs within the bloc, a neutral or favorable regulatory environment, as well as certain protection from sanctions risks [9]. For Russia, these advantages became particularly important after 2022, which marked the beginning of unprecedented sanctions pressure, and the most significant role in this case was played by the so-called "geopolitical location advantage", expressed in the absence of obligations from BRICS partners under Western sanctions regimes. At the same time, such partners, who are also active in Western financial markets (primarily companies from China, India and the UAE), face the threat of secondary sanctions against them, which largely explains the gap between the declared intentions and the actual volume of investments of the BRICS countries in Russia.

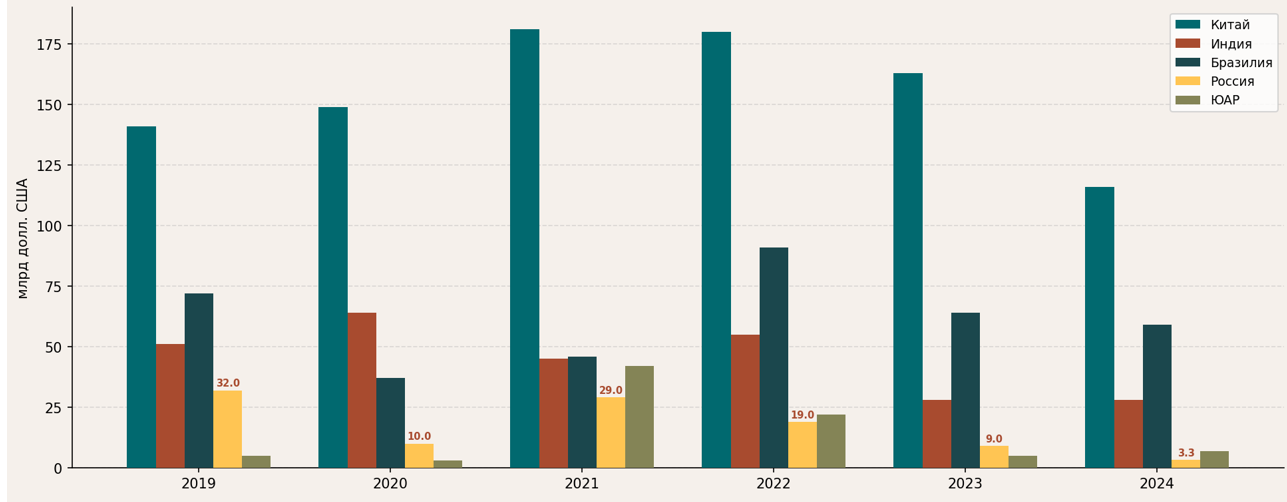

The institutional aspect of investment cooperation within the framework of BRICS is related to the activities of two key financial mechanisms formed within the block: the New Development Bank (NDB) and the Pool of Conditional Foreign Exchange Reserves (IWRM). The NBR, established by the Fortaleza Treaty in 2014 with an authorized capital of $100 billion [1], approved the financing of 140 investment projects totaling $42.9 billion by the beginning of 2026.[https://www.ndb.int /]. Since February 2022, the NBR has suspended new transactions with Russia, retaining only the maintenance of the existing portfolio ($1.9 billion). as of early 2026), however, following the results of the 11th annual meeting of the NBR Board of Governors, held on May 14-15, 2026 in Moscow, Russian Finance Minister Anton Siluanov announced the achievement of "mutually acceptable solutions, estimated at billions of dollars," which will be implemented as part of the bank's new strategy [Vedomosti, May 15, 2026, https://www.vedomosti.ru/economics/news / 2026/05/15/1197676-vozobnovleniya-finansirovaniya]. As for the IWRM, which was established at the same time, it was conceived as a currency swap instrument in which the Central Bank of the recipient country exchanges, through the IWRM, the national currency for US dollars from the Central Bank of the donor countries with the obligation to buy back and pay interest. However, during the entire existence of the IWRM, not a single country of the association has used this tool, so this mechanism, for all its symbolic significance as an analogue of the IMF, remains at the declarative level. Dynamics of investment flows in Russia and other BRICS countries During the association's existence, the total inflow of foreign direct investment (FDI) to the BRICS-5 countries (Brazil, Russia, India, China, South Africa) has more than tripled from $84 billion to $331 billion, and their share in global FDI inflows has increased from 15.2% to 21.9%. [UNCTAD, 2026. https://unctad.org/publication/two-decades-intra-brics-trade-trends-patterns-and-policies ], which, according to many researchers and analysts, indicates a structural shift in the global system of international capital movement, in which the countries of the Global South are increasingly becoming centers of attraction for international investors [10, 11]. At the same time, investment dynamics differ significantly for individual BRICS countries (Fig. 1). China remains the undisputed leader, attracting over $150 billion in FDI annually until 2023, although amid rising geopolitical tensions with Western partners in 2024, their volume decreased by 29% to $116 billion. India demonstrates relative stability in this indicator, while Brazil reached a record high of $91 billion in 2022 due to large-scale investments in renewable energy [Banco Central do Brasil, 2025. https://www.bcb.gov.br/content/acessoinformacao/acesso_informacao_docs/Economic-Bulletin-2025.pdf ], after which there was a certain natural decrease.

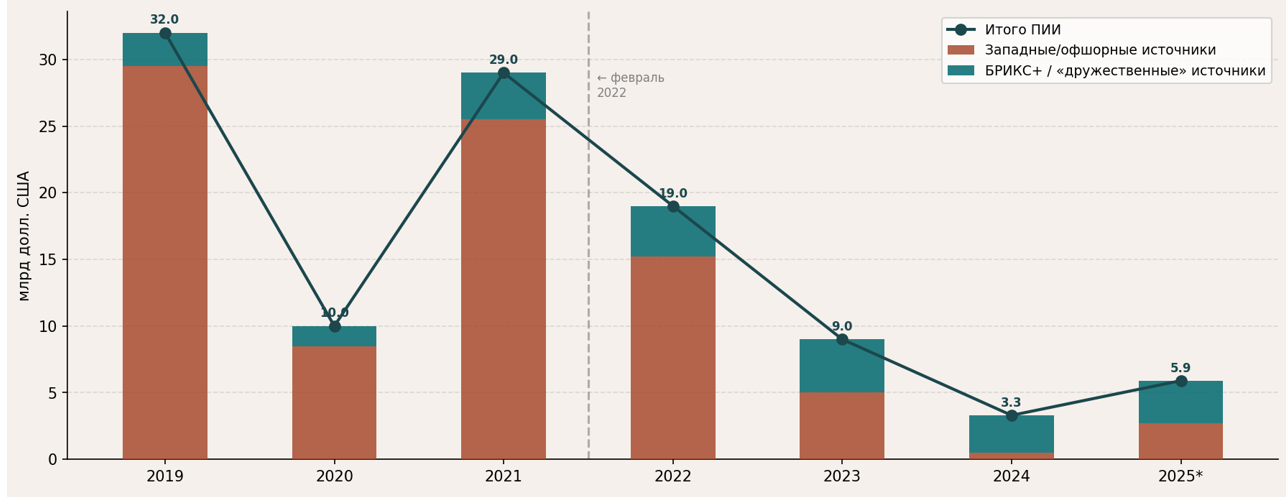

Figure 1. FDI inflows to the BRICS-5 countries in 2019-2024 (at the end of the year, USD billion). Compiled by the author according to the data of the Bank of Russia [http://cbr.ru/statistics/macro_itm/external_sector /], UNCTAD [https://unctad.org/publication/two-decades-intra-brics-trade-trends-patterns-and-policies , https://unctad.org/publication/world-investment-report-2025 ], NBR [https://www.ndb.int/wp-content/uploads/2025/03/Investor-Presentation-Oct-2025-.pdf ] Russia, on the other hand, stands out from other BRICS participants in principle: if in 2019 the country attracted $32 billion in FDI, by 2024 this figure had decreased by 9.7 times, amounting to only $3.3 billion (Fig. 2) According to preliminary data from the Bank of Russia [http://cbr.ru/statistics/macro_itm/external_sector/iip /], a trend was recorded in 2025 The net inflow of FDI amounted to about $5.9 billion, which was mainly due to reinvestment of income by Chinese companies and increased investor activity from the UAE, but its pre-crisis level remains unattainable in the near future.

Figure 2. Volume and structure of foreign direct investment in the Russian Federation, 2019-2025 (at the end of the year, billions of US dollars). Source: compiled by the author according to the data of the Bank of Russia [http://cbr.ru/statistics/macro_itm/external_sector /], UNCTAD [https://unctad.org/publication/two-decades-intra-brics-trade-trends-patterns-and-policies , https://unctad.org/publication/world-investment-report-2025 ], Wiiw [https://wiiw.ac.at/foreign-capital-in-russia-taking-stock-after-two-years-of-war-dlp-6898.pdf ], Oeconomus [https://www.oeconomus.hu/en / analyzes/changes-in-russian-capital-investment-by-destination-country-between-1992-and-2024/] Not only the total volume, but also the geography of Russian FDI commitments has undergone significant changes (Figure 2). If, until 2022, Western jurisdictions (the so-called "unfriendly" countries) provided about 72% of the accumulated portfolio of incoming FDI, by now this share has decreased to 45%, while The combined share of the BRICS+ countries and other "friendly" jurisdictions increased from 10% to 30%. In absolute terms, accumulated liabilities to "friendly" investors increased from about $49 billion to about $77 billion, amid a general reduction in the portfolio of incoming FDI from $610 billion to $258 billion. Investment presence of the BRICS countries in Russia As mentioned above, it is difficult to assess the real investment presence of the BRICS countries in Russia due to the fact that starting in 2022, the Bank of Russia does not publish some data, including on FDI, and alternative sources use estimated rather than official data. With this caveat in mind, the following can be stated. China remains the largest investor among the BRICS+ countries in the Russian economy. As of the end of 2024, the accumulated direct investments of Chinese companies in Russia amount to about $9 billion, concentrated mainly in the energy, mining and construction sectors [UNCTAD, 2026. https://unctad.org/publication/world-investment-report-2025 ; wiiw, 2024. https://wiiw.ac.at/foreign-capital-in-russia-taking-stock-after-two-years-of-war-dlp-6898.pdf ]. At the same time, despite the political rhetoric about "unlimited partnership", the largest Chinese state-owned banks and corporations are cautious about new investments in Russia, fearing increased sanctions pressure from the United States and the EU [12].

The United Arab Emirates, which joined the BRICS since the beginning of 2024, had previously ranked second among "friendly" investors in the Russian economy [13]. The UAE's accumulated FDI portfolio in the Russian economy is estimated at $18 billion, and these investments are clearly diversified, heading into real estate, trade, financial intermediation, logistics, etc. [wiiw, 2024. https://wiiw.ac.at/foreign-capital-in-russia-taking-stock-after-two-years-of-war-dlp-6898.pdf]. According to the Eurasian Development Bank (EDB), in 2024-2025, the UAE provided at least 45% of the increase in Asian investment in the Eurasian region, although a significant part of it was directed not directly to Russia, but to the countries of Central Asia. [https://eabr.org/analytics/special-reports/eurasian-region-and-asian-countries-analysis-of-investment-flows/]. The economic cooperation between Russia and India is fundamentally different, characterized primarily by an increase in trade turnover [14], which reached a record $68.7 billion in the 2024-2025 financial year. At the same time, investment cooperation remains underdeveloped – according to official data from the Indian side, in 2025 Russia ranks only 31st in terms of FDI in India with an accumulated figure of $ 1.3 billion, and counter-investments by Indian companies in Russia in 2024 amounted to only $760 million [Infobrics, 2026. https://infobrics.org/en / post/92087]. As for the rest of the BRICS+ members, Brazil and South Africa are practically not present in the Russian economy as direct investors [15], their economic relations with Russia are mainly of a trade rather than investment nature [UNCTAD, 2026. https://unctad.org/publication/two-decades-intra-brics-trade-trends-patterns-and-policies ; UNCTAD, 2025. https://unctad.org/publication/world-investment-report-2025 ]. The new members of BRICS+ (Iran, Ethiopia, Egypt) currently do not have significant investment potential for investments in Russia in the short term [16], although they can be considered as possible "transit" jurisdictions for third-country capitals. Barriers and scenarios for the development of BRICS-Russia investment cooperation Currently, the development of investment cooperation between Russia and the rest of the BRICS member countries is facing a number of problems, the resolution of which largely determines its future prospects. The first of them should be called the imperfection of the institutional infrastructure of investment cooperation within the framework of the BRICS. Tests of the conditions of sanctions pressure have shown that the NBR and the IWRM are significantly less resistant to it than bilateral investment flows, which exposes the structural vulnerability of the BRICS as an investment platform. As mentioned above, the IWRM is currently only a declarative mechanism, and the NBR suspended consideration of new Russian projects in 2022. The decisions of the 11th annual meeting of the NBR Board of Governors, held on May 14-15, 2026 in Moscow, following which the NBR announced the resumption of project financing in Russia, inspire cautious optimism, but at the moment nothing specific is known about its timing, volume and conditions. A significant barrier to investment cooperation between the BRICS countries and Russia is the problem of secondary sanctions [17]. Western countries, primarily the United States, are consistently expanding the application of secondary sanctions against third countries doing business with Russia. A number of Chinese and Indian companies, as well as investors from "friendly" and "neutral" countries outside the BRICS, have already been subject to restrictions, which has had a pronounced deterrent effect on the investment activity of a large business from the BRICS countries in Russia [Oeconomus, 2025. https://www.oeconomus.hu/en / analyzes/changes-in-russian-capital-investment-by-destination-country-between-1992-and-2024/]. The development of the infrastructure for investment settlements in the national currencies of the BRICS countries remains a kind of "bottleneck". If the share of the ruble in Russia's foreign trade settlements reached 40-45% in 2025, and the share of the yuan reached 25-30%, then for longer–term and complex investment transactions, the infrastructure of mutual settlements in national currencies lags significantly [18]. At the same time, there are a number of factors that create a favorable environment for deepening investment cooperation. These include the strengthening of the role of the EAEU as an investment intermediary for the BRICS countries [19] (currently Kazakhstan and Belarus are transit jurisdictions for investment flows from Asia), the development of the mBridge project for cross-border settlements in digital currencies of central banks [20], the signing by Russia and India of a Program for the development of strategic areas economic cooperation until 2030, which provides for the expansion of investment flows to $50 billion [Infobrics, 2026. https://infobrics.org/en /post/92087], and a number of others. Based on the above, we can assume some scenarios for the development of investment cooperation in the BRICS-Russia format. The basic scenario assumes the continuation of the Western sanctions regime and a gradual deepening of bilateral investment cooperation, mainly through state-owned companies and joint ventures in the energy and infrastructure sectors. In this scenario, the main areas of cooperation will be the implementation of major projects of the Russian-Chinese gas corridor "Power of Siberia – 2", the expansion of oil refining in India and the development of industrial zones within the framework of the FEZ in the Russian Far East. The forecast estimate for this scenario was carried out by extrapolating the trend of recovery growth in 2024-2025. As mentioned above, FDI inflows from the BRICS+ countries to Russia increased from $3.3 billion in 2024 to $5.9 billion in 2025, which corresponds to an absolute increase of $2.6 billion or 79% year-on-year. A mechanical linear extrapolation of this trend gives a forecast for 2027 of about 10.7-11.1 billion dollars of FDI. However, the result obtained obviously requires downward corrections. First, it is necessary to take into account the effect of a "low base" – the high relative growth in 2025 is partly explained by the start from an abnormally low level in 2024, and its reproduction with the same intensity in subsequent periods should not be expected; the application of a smoothed growth rate of 25-30% for 2026-2027 reduces the estimate to 9.2-9.9 billion dollars.. Secondly, it should also be taken into account that this scenario assumes an influx of investments primarily in large projects involving a multi-year investment cycle. In particular, the peak of investments in the Power of Siberia – 2 project under the baseline scenario is expected no earlier than 2027-2028, which limits the potential contribution of this project to the indicators of 2027. Taking into account both amendments, the range of the forecast estimate can be adjusted up to 8-10 billion dollars. FDI per year by 2027, while maintaining the structure in favor of the energy sector (70-75%). The optimistic scenario assumes a reduction in sanctions pressure as a result of the settlement of the Ukrainian conflict and/or through the systematic and consistent development of mechanisms to protect against secondary sanctions (for example, through sovereign guarantees, clearing through the NBR or settlements with the Central Securities Exchange). In this scenario, the NDB resumes project financing in Russia, and the largest enterprises of the BRICS+ countries begin direct investments in the Russian economy. Returning once again to the results of the 11th annual meeting of the NBR Board of Governors, we note that some elements of this scenario can with a certain degree of probability be called implemented.

Finally, the pessimistic scenario suggests the extension of secondary sanctions to the main BRICS partners, which will lead to a sharp curtailment of investment activity and the de facto exclusion of Russia from the system of international capital flows. Linear extrapolation of the general trend of 2021-2025 suggests that in this case, the inflow of FDI from the BRICS countries will not exceed $ 1-2 billion per year, mainly due to reinvestment of already accumulated positions, and the investment deficit will be replaced by an increase in government investments with a decrease in their effectiveness. Conclusion Thus, the conducted research allows us to conclude that the BRICS countries are taking an increasingly important position in the global investment space, which suggests a structural shift in favor of non-Western centers of capital attraction that has occurred during the existence of the association. Its recent expansion at the expense of the UAE, Egypt, Iran and Indonesia significantly increases the total investment potential of the block. At the same time, since 2022, Russia has been practically sidelined from this investment dynamic – the annual inflow of FDI has decreased by almost 10 times to date, and although there has been a structural shift from "unfriendly" to "friendly" jurisdictions (the share of FDI from the BRICS+ countries in Russia's accumulated liabilities has increased from 10% to 30%), however, the absolute magnitude of this shift did not compensate for the losses from the withdrawal of Western capital, and the total FDI portfolio more than halved. One of the key reasons for the current situation is the instability of the BRICS institutional architecture (NBR and IWRM) in the face of sanctions pressure. Thus, the threat of secondary sanctions is the main barrier limiting the willingness of even "friendly" BRICS partners to make large-scale investments in Russia. Overcoming this barrier is not only and not so much a financial, but also a geopolitical task that requires a coordinated position of the BRICS countries on international platforms. As long as this threat persists, the BRICS investment potential for Russia remains only partially realized. Based on the conducted research, it is also possible to identify a number of priority areas for improving Russia's investment policy in the context of cooperation with BRICS partners. First, it makes sense to develop special investment regimes for companies from the BRICS+ countries, including expanded guarantees for profit repatriation, tax preferences, and simplified mechanisms for resolving investment disputes. Secondly, it is necessary to accelerate the formation of an investment settlement infrastructure in national currencies. The key in this area is the intensification of Russia's participation in the development of the mBridge project and similar initiatives within the framework of BRICS on digital financial settlements. Third, it seems appropriate to partially restructure the NBR in relation to the Russian position. An alternative to completely abandoning participation in Russian investment projects could be the creation of a specialized NDB financial window for projects implemented exclusively within BRICS without involving Western counterparties, with a different regulatory regime and without access to Western capital markets. However, the implementation of this initiative depends not only on Russia and will require political will from all BRICS members, primarily China and India. We would like to note once again that following the results of the 11th annual meeting of the NBR Board of Governors, held on May 14-15, 2026 in Moscow, it was announced that the financing of projects in Russia would resume as part of the bank's new strategy, which may imply something similar to the proposed one. Finally, it seems necessary to reorient investment priorities to technology sectors. Historically, Russia's investment cooperation with the BRICS countries has been concentrated mainly in the raw materials industries, however, it is strategically advantageous to increase investments in digital infrastructure, industrial cooperation, and nuclear energy, as in areas where the risk of secondary sanctions is significantly lower and the development potential is much higher.

The article is published in its final version as approved following the last positive peer review recommending acceptance for publication. It incorporates revisions made by the author in response to prior negative peer review reports that did not recommend publication. All peer review reports, including initial negative reviews, are published in open access alongside the article. All versions of the author’s revisions are archived in the publisher’s repository and may be made available upon reasonable request in accordance with Elsevier’s editorial policies and applicable data availability requirements.

Read all reviews on this article

References

1. Pivovar, E. I., Kondrashova, I. S., Naumov, A. O., & others. (2024). The intergovernmental association BRICS: Pages of history and modernity. Saint Petersburg State University Press.

2. Lukyanov, V. Yu. (2026). SCO and BRICS-history and modernity. Northern (Arctic) Federal University Bulletin. Humanities and Social Sciences Series, 26(2), 18-29. https://doi.org/10.37482/2687-1505-V496

3. Anofrikhov, D. O. (2026). The role of BRICS+ in the construction of a new economic order. Siberian Institute of Business and Information Technologies Bulletin, 15(1), 50-57. https://doi.org/10.24412/2225-8264-2026-1-1065

4. Garcia, A., Thompson, L., & Brito, C. (2025). South-south investments: Driver for alternative globalization? Examining China-led special economic zones in Brazil and South Africa. Critical Sociology, 51(4-5), 887-905.

5. Serrano-Moreno, J. E., Solar, D., & Sossdorf, F. (2026). To BRI or not to BRI? Geoeconomic competition, trade agreements and foreign direct investment in East Asia and the Pacific. Asian Education and Development Studies, 1-20.

6. Wasif, M., et al. (2025). Data-driven insights on the relationship between BRICS financial policies and global investment trends. Journal of Economics, Finance and Accounting Studies, 7(2), 133-147.

7. Kovalchuk, A. (2025). Financial crises, economic uncertainty avoidance and investment decisions in BRICS economies. Review of Behavioral Finance, 17(6), 1020–1044. https://doi.org/10.1108/rbf-12-2024-0370

8. Dunning, J. H., & Lundan, S. M. (2008). Institutions and the OLI paradigm of the multinational enterprise. Asia Pacific Journal of Management, 25(4), 573-593. https://doi.org/10.1007/s10490-007-9074-z

9. Kafeel, K., et al. (2026). Analyzing the complexities of export: A heterogeneous analysis of BRICS economies and product types. Future Business Journal, 12(1), 27. https://doi.org/10.1186/s43093-026-00742-8

10. Gomez, L., Oinas, P., & Wall, R. S. (2022). Undercurrents in the world economy: Evolving global investment flows in the South. The World Economy, 45(6), 1830–1855. https://doi.org/10.1111/twec.13219

11. Shkhagoshev, R. V., Shkhagoshev, R. V., & Buben, A. A. (2024). Changes in international capital flows in the modern world: Trends and consequences. Eurasian Science Bulletin, 16(1), 44.

12. Zhirikov, V. (2025). Analysis of the sectoral structure of foreign direct investment between the Russian Federation and the People's Republic of China. BRICS Journal of Economics, 6(3), 31-45. https://doi.org/10.3897/brics-econ.6.e145598

13. Shavina, E. V., & Prokofyev, V. A. (2020). Energy potential and directions of cooperation of BRICS countries with Russia. Geo-economics of Energy, 9(1), 56-71.

14. Ogloblina, E. V. (2025). Investment cooperation between Russia and India. Discussion, (6) 139, 255-262. https://doi.org/10.46320/2077-7639-2025-6-139-255-262

15. Esteves, P., & Coelho, C. F. (2025). Be careful what you wish for: Brazil and BRICS in three acts. South African Journal of International Affairs, 32(1-2), 91-112. https://doi.org/10.1080/10220461.2025.2528980

16. Chikova, A. E. (2025). Cooperation within BRICS+ as a new format of integration process of fast-developing countries. Law and Management: XXI Century, 21(1), 195-206. https://doi.org/10.24833/2073-8420-2025-1-74-195-206

17. Oganisyan, L. D. (2026). Sanctions in the BRICS discourse. Moscow University Bulletin. Series XXV. International Relations and World Politics, 18(1), 33-61.

18. Makogon, Yu. V., & Shikova, L. V. (2026). Research on sectoral cooperation between Russia and BRICS+ countries. Siberian Institute of Business and Information Technologies Bulletin, 15(1), 81-88. https://doi.org/10.24412/2225-8264-2026-1-1088

19. Tsiku, S. Yu. (2026). Prospects for economic integration of the Eurasian Economic Union countries in the period of global fragmentation. Scientific Notes of Young Researchers, 14(1), 24-36.

20. Bouguelli, R., & De Conti, B. (2026). Building bridges or competing in a payments arms race? The geopolitics of the mBridge project. International Journal of Political Economy, 55(1), 70-87. https://doi.org/10.1080/08911916.2026.2624895

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The article is devoted to the study of investment cooperation within the framework of BRICS as an alternative channel for attracting foreign investment to Russia. The topic of the paper has been particularly relevant in recent years due to the catastrophic decline in investment in the Russian Federation. The research methodology is presented in the article and corresponds to the stated objectives (no complex mathematical analysis is presented in the work, therefore general scientific methods were used). The advantages of the described methods should include the author's honest recognition of methodological limitations. In particular, the author points out that after 2022, the Bank of Russia stopped publishing some of the detailed data, and therefore it is forced to use estimated and consolidated indicators from alternative sources. This approach increases the credibility of the results. The weak side of the methodology is the lack of econometric tools, which is explained by the fragmentary nature of the data, but reduces the rigor of the conclusions; forecast estimates in scenarios (8-10 billion dollars). FDI by 2027) does not have a clear methodological justification (how did they get it? expert assessment / extrapolation/ model?). The scientific novelty of the work is not explicitly described, which is generally one of the disadvantages of the work. There are no significant comments on the style or structure of the work. The structure of the work is quite logical, but in the section "Structure and scale ..." it is necessary to describe exactly the structure and scale, preferably illustrated with diagrams or drawings. Currently, the text does not describe the structure as such. Nevertheless, there are shortcomings in the work that need to be addressed.: 1. Specify the scientific novelty in the introduction, as well as the audience for which this work is intended. 2. Indicate on the basis of which development scenarios were proposed (expert assessment?, calculations - according to the author's estimates based on trend extrapolation?). 3. You should also check the source number 10 in the list of references.: 10. The BRICS Bank has found a solution to resume financing projects in Russia // Vedomosti, May 15, 2006 – URL: https://www.vedomosti.ru/economics/news/2026/05/15/1197676-vozobnovleniya-finansirovaniya (date of request: 05/16/2026). The article was published in 2026. We need to fix the date for 2026. The author demonstrates mastery of the scientific context and correctly works with alternative points of view. In general, the appeal to opponents is present and correct, but it can be enhanced by a more explicit juxtaposition of points of view and approaches. The conclusions presented in the paper are empirically sound, logical, and consistent with the goal. After minor edits, the article can be accepted for publication. The article is of interest to experts in the field of world economy and international relations. In general, this can also be clearly stated in the introduction. The author has made changes to the text of the article. Added an investment structure in the form of a diagram. I have corrected the text and conclusions. Made edits to the list of sources.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of the research in the reviewed article is the transformation of the structure of foreign investment in the Russian economy under the sanctions pressure of 2022-2026. The research methodology is based on the use of a scenario approach, general scientific methods (systemic, institutional and comparative analysis) and statistical methods applied to data from the Central Bank of the Russian Federation, UNCTAD, EDB, the New Development Bank (NDB) BRICS and various analytical centers. The relevance of the work is due to the degradation of investment cooperation with "unfriendly" countries and the forced search for new channels to attract foreign investment to Russia. The scientific novelty of the work consists in the presented results of the analysis of investment cooperation in the BRICS–Russia format in the period 2022-2026, proposed by the authors of the idea of restructuring the NBR through the creation of a "specialized financial window" for intra-block projects that do not enter the Western capital markets. Structurally, the following sections are highlighted in the work: "Introduction", "Materials and research methods", "BRICS as an international investment platform", "Dynamics of investment flows in Russia and other BRICS countries", "Investment presence of BRICS countries in Russia", "Barriers and scenarios for the development of BRICS-Russia investment cooperation", "Conclusion" and "Bibliography". The publication notes that a number of international institutions, including financial ones, have been formed within the framework of the BRICS, and work is underway to de-dollarize trade operations, develop the transport network, digital infrastructure, and investment cooperation. The authors analyzed the inflow of foreign direct investment (FDI) to the BRICS countries, and showed the dynamics of attracting investment to Russia in 2019. Russia attracted $32 billion in FDI, but by 2024 this figure had decreased by 9.7 times, amounting to only $3.3 billion. The text of the publication is successfully illustrated with two figures: "FDI inflows to the BRICS-5 countries in 2019-2024" and "Volume and structure of foreign direct investment in the Russian Federation, 2019-2025", vividly visualizing the results of the analysis. Recognizing the potential of BRICS, the author argues that without solving the problem of secondary sanctions and the institutional instability of the NBR, this potential will remain unfulfilled, since the absolute increase in the share of "friendly" countries from 10% to 30% does not compensate for the twofold drop in the total FDI portfolio. In conclusion, the article identifies priority areas for improving Russia's investment policy in the context of cooperation with BRICS partners. The Bibliography section includes 14 sources: modern scientific publications by Russian and foreign authors in Russian and English. The text contains references to the bibliographic list, confirming the existence of an appeal to the opponents. Of the shortcomings, it is worth noting the following. Firstly, when constructing the baseline scenario, specific calculations are not provided, but only their results are presented, and it is not clear whether the effect of a "low base" and investment lags of large projects (for example, the Power of Siberia – 2) were taken into account when extrapolating the trend of 2024-2025. Secondly, it is appropriate to expand the "Bibliography" section and bring the number of sources to the recommended list of references accepted by the editorial board – 20 pieces. The reviewed material corresponds to the direction of the journal "Finance and Management", reflects the results of the research conducted by the authors, has signs of scientific novelty and practical significance, but before publication the article needs some revision in in accordance with the comments made.

Third Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

In the re-reviewed article, submitted after revision, the subject of the study is the transformation of the structure of foreign investment in the Russian economy under the sanctions pressure of 2022-2026. The research methodology is based on the use of a scenario approach, general scientific methods (systemic, institutional and comparative analysis) and statistical methods applied to data from the Central Bank of the Russian Federation, UNCTAD, EDB, the New Development Bank (NDB) BRICS and various analytical centers. The relevance of the work is due to the degradation of investment cooperation with "unfriendly" countries and the forced search for new channels to attract foreign investment to Russia. The scientific novelty of the work consists in the presented results of the analysis of investment cooperation in the BRICS–Russia format in the period 2022-2026, proposed by the authors of the idea of restructuring the NBR through the creation of a "specialized financial window" for intra-block projects that do not enter the Western capital markets. Structurally, the following sections are highlighted in the work: "Introduction", "Materials and research methods", "BRICS as an international investment platform", "Dynamics of investment flows in Russia and other BRICS countries", "Investment presence of BRICS countries in Russia", "Barriers and scenarios for the development of BRICS-Russia investment cooperation", "Conclusion" and "Bibliography". The publication notes that a number of international institutions, including financial ones, have been formed within the framework of the BRICS, and work is underway to de-dollarize trade operations, develop the transport network, digital infrastructure, and investment cooperation. The authors analyzed the inflow of foreign direct investment (FDI) to the BRICS countries, and showed the dynamics of attracting investment to Russia in 2019. Russia attracted $32 billion in FDI, but by 2024 this figure had decreased by 9.7 times, amounting to only $3.3 billion. The text of the publication is successfully illustrated with two figures: "FDI inflows to the BRICS-5 countries in 2019-2024" and "Volume and structure of foreign direct investment in the Russian Federation, 2019-2025", vividly visualizing the results of the analysis. Recognizing the potential of BRICS, the author argues that without solving the problem of secondary sanctions and the institutional instability of the NBR, this potential will remain unfulfilled, since the absolute increase in the share of "friendly" countries from 10% to 30% does not compensate for the twofold drop in the total FDI portfolio. In conclusion, the article identifies priority areas for improving Russia's investment policy in the context of cooperation with BRICS partners. The Bibliography section includes 20 sources: modern scientific publications by Russian and foreign authors in Russian and English. The text contains references to the bibliographic list, confirming the existence of an appeal to the opponents. In the course of eliminating the comments made, the authors reflected in the text the logic of calculations when constructing the baseline scenario, starting from growth from $ 3.3 billion to $ 5.9 billion in 2025, pointed to the application of corrective amendments, the "low base effect" and the transition to a smoothed rate of 25-30%, took into account the investment lag of large projects, indicating that As the peak of investments in the Power of Siberia – 2 is expected no earlier than 2027-2028, the Bibliography section has been expanded and the number of sources has been brought up to the recommended list of references adopted by the editorial board. The reviewed material corresponds to the direction of the journal "Finance and Management", reflects the results of the research conducted by the authors, has signs of scientific novelty and practical significance, and is recommended for publication.

|