|

DOI: 10.7256/2454-065X.2025.3.74740

EDN:

XQJPOI

Received:

06/06/2025

Published:

06/13/2025

Abstract: The subject of this study is the analysis of approaches (legal and economic) to the classification of tax benefits, followed by the development of a new approach using the example of the pharmaceutical industry. The aim of this article is to develop a new approach to classifying tax support instruments that enhances the effectiveness of fiscal support tools for capital-intensive industries (using the pharmaceutical industry as a case study) in practice. The author provides a detailed examination of current approaches to the classification and summarization of tax benefits by various authors. Based on these current approaches, the author proposes their own method for classifying support instruments for the pharmaceutical sector, developed on the basis of current benefits available to pharmaceutical companies. The author analyzes which support tools for the pharmaceutical industry are more effective. Based on the developed classification of support instruments for the pharmaceutical industry, the author suggests directions for the development of incentives in this sector. This research was conducted using general scientific research methods, including systemic, logical, and comparative analysis, as well as the method of analogy. The main results of the research include the classification of support tools for the pharmaceutical industry, which allows the identification of directions for the development of incentives in the pharmaceutical sector. From the conducted analysis, the author concludes that comprehensive support tools are more effective for supporting investment projects, and that targeted support instruments are also important as they impact specific costs and actions relevant to the pharmaceutical industry. The scientific novelty of the study lies in the development of a new classification of support instruments for the pharmaceutical sector, which facilitates the identification of challenges related to incentivizing the pharmaceutical industry, as well as suggestions for refining the current approach to applying comprehensive and targeted support tools with the aim of enabling their joint application: harmonization of tax benefits, expansion of technology-oriented tax benefits, and integration of existing tax benefits into comprehensive support tools.

Keywords:

Pharmaceutical industry, Targeted tax incentives, Complex tax incentives, Tax incentives classification, Tax incentives, Tax incentives compare, Support instruments, Non-tax incentives, Tax incentives harmonization, Approaches to classification

This article is automatically translated.

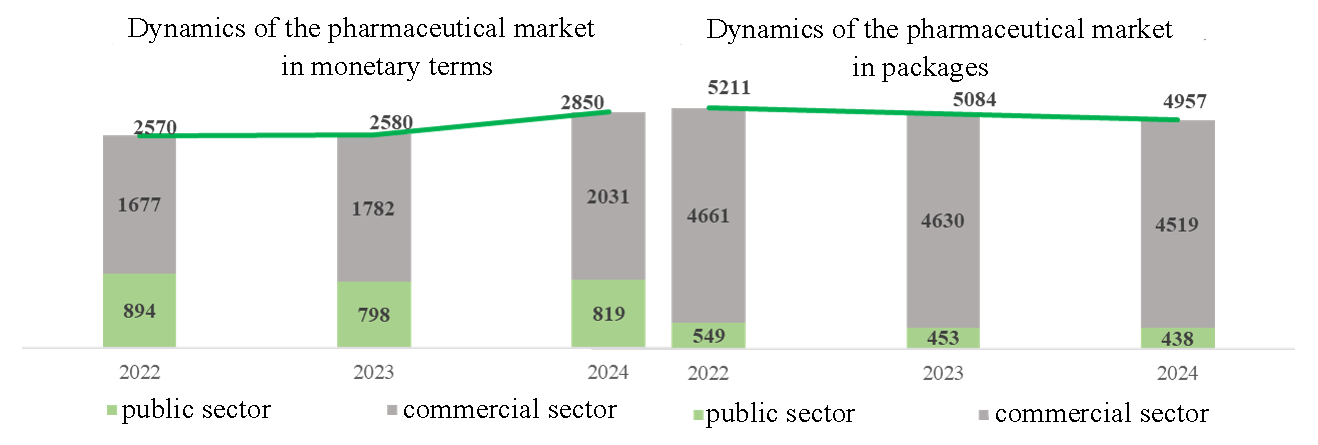

Introduction Tax incentives are an important component of government financial support for almost any industry, but they have the most important impact on capital-intensive industries. These types of production include the pharmaceutical industry. By complementing budget and credit forms of support, tax incentives reduce the burden on companies, increasing the return on investment in fixed assets. In this context, the most important aspect for the state is that such benefits should provide an appropriate effect for the state, manifested in maintaining stable economic growth rates. It is important to note that this requires a synergy of theoretical views, methodological developments and real practice. The purpose of this article is to develop a new approach to the classification of tax support instruments, which helps to increase the effectiveness of fiscal support instruments for capital-intensive industries (using the example of the pharmaceutical industry) in practice. The classification and analysis of tax benefits is implemented using the example of the pharmaceutical industry, since at the moment it plays a significant role in ensuring the national security of the Russian Federation through the development of medicines and the localization of their production on the territory of the Russian Federation. Consider the current performance of the pharmaceutical industry.

Figure 1 – Volume of the pharmaceutical market of the Russian Federation Based on the data presented, we can see that in monetary terms, the pharmaceutical market of the Russian Federation is showing growth in 2023 and 2024. However, we see that the pharmaceutical market is showing a decline in packaging in 2023 and 2024. This is due to the fact that medicines are increasing in price, while the volume of their sales on the market is slowing down due to rising prices, the withdrawal of individual foreign companies from the market, and a decrease in the volume of imports of medicines. This trend is relevant for both the commercial segment and the government segment. Thus, based on statistics, it can be concluded that the pharmaceutical industry needs additional incentives, including in accordance with the Decree of the Government of the Russian Federation dated 06/07/2023 No. 1495-r "On approval of the Strategy for the development of the pharmaceutical industry of the Russian Federation for the period up to 2030" for the implementation of "ensuring production in the Russian Federation high-quality, effective and safe medicines that are competitive in the domestic and foreign markets to meet the needs of the healthcare system of the Russian Federation and realize the export potential of the pharmaceutical industry", which is actually the term "drug safety". In addition, the pharmaceutical industry is a capital-intensive and knowledge-intensive industry[1], which is reflected in the need for a significant amount of investment both as a result of R&D and in the process of manufacturing in Russia. As part of the restrictions that have arisen, the withdrawal or reduction of imports by foreign pharmaceutical companies, it is necessary to increase the production rate of various types of medicines in the Russian Federation, which justifies the relevance of developing new views in the theory of tax incentives. Research methods and materials Achieving this goal is possible if the following general scientific methods are used in the process of research and evaluation of its results: - deduction and induction – the use of methods makes it possible to improve the quality of work by relying on general scientific principles of conducting research on the theoretical foundations, principles and methods of state financial support for the pharmaceutical industry and ensuring the logic of research;

- analysis and synthesis – the application of this methodology will ensure the construction of a holistic, scientifically based classification of tax incentive instruments based on comparative characteristics of their types;

- analogy – this method allows you to transfer previously studied tasks from one area of research to another, while obtaining new results, in particular, with its help it will be possible to evaluate the possibilities of using various conceptual approaches in the field of pharmaceutical support.

The scientific novelty of the study lies in a new approach to the classification of tax incentives (using the example of the pharmaceutical industry), aimed at increasing the effectiveness of tax incentives and the impact of their application. Approaches to classifying tax benefits It is worth noting that the relationship between the classification of benefits and the effectiveness of their application has already been proven in earlier studies by scientists[2],[3]. As a result of the analysis of scientific literature, two classical approaches to the classification of tax benefits (legal and economic) have been identified. As a rule, in the theory of taxation, benefits are divided into 3 categories: withdrawals, discounts and tax credits. This classification is based on an economic approach, which assumes that any tax benefit is manifested in a reduction in the tax burden. A similar approach is followed by S.G. Pepelyaev[4], Yu.A. Krokhina[5]. Representatives of the economic approach often consider tax benefits, according to the classification of the Tax Code of the Russian Federation (by level and type of taxes)[6],[7]. It is worth noting that such an approach to classifying tax benefits does not allow evaluating the effectiveness of tax benefits, it is aimed only at categorizing benefits. Consequently, this classification is losing its relevance. Adherents of the legal approach are, for example, S.V. Barulin, A.V. Makrushin[8]. The authors note that the concept of tax benefits is codified, and therefore tax credits and discounts cannot be formally classified as tax benefits. I.A. Maiburov calls codified benefits direct, and all others indirect or codified[9]. On the same basis, a number of authors introduce a different category of "tax preferences", which is considered in two ways. For example, Avdeeva V.M. notes that tax preferences are "advantages provided to taxpayers that change tax obligations and are subject to mandatory application by business entities"[10]. The author includes tax benefits, reduced tax rates, administrative incentives, and special tax regimes. A narrower approach is used by Balandina A.S., who focuses on the mandatory nature of tax preferences (as opposed to voluntarily applied tax benefits) and on the provision of tax preferences on the terms of mutual obligations on the part of the taxpayer[11]. The latter circumstance seems to be extremely relevant and will be discussed in more detail later.

The second direction in the development of tax science is related to the development of narrow author's classifications of benefits for various reasons. For example, M.V. Selyukova divides benefits according to the purpose of providing them into social, incentive and technical ones[12]. Khabdaev A.M. provides a broader classification of tax benefits[13] (Table 1). Table 1 – Classification of tax benefits according to Khabdaev A.M. | Classification criteria | Types of benefits | | According to the method of influencing the law-regulating process | 1) basic (basic) 2) additional | | In order of obtaining benefits for taxpayers | 1) Direct benefits 2) indirect benefits | | By the level of regulatory regulation | 1) federal 2) Regional 3) Local | | According to the degree of benefits provided | 1) Tax exceptions 2) tax holidays 3) tax deductions |

As you can see, within the framework of narrow author's classifications, there is a criterion for the targeted orientation of benefits, the degree of provision, and the possibilities of applying benefits in certain situations, which is aimed at improving the effectiveness of implementing a certain category of tax benefits. However, the research of the second group does not pay attention to the sectoral basis, which, according to the author, is an essential criterion for determining the effectiveness of tax benefits. Tax incentives have different effects and degrees of susceptibility depending on the industry[14]. These differences are primarily due to the industry-specific features of doing business. For example, examining the experience of applying tax incentives in the oil sector, A.S. Balandina revealed that "... the benefits provided to taxpayers for the purpose of calculating and paying taxes are not systemic and investment-oriented"[15], that is, they do not affect the stimulation and development of the industry. Using the example of the oil industry in the Russian Federation, the author suggests a classification based on the direction of the impact and the causes of the lowering coefficients. In accordance with the work of Balandina A. S., the following classification of sectoral tax benefits is proposed, depending on the direction of the impact and the causes of occurrence: industrial, geological, technological and geographical[16]. The author shows that the classification of tax benefits that is adequate to economic conditions is an important factor in identifying categories of instruments that will have the greatest effect on the development of a particular industry in the Russian Federation. However, it is important to note that the presented industry classification has too narrow a focus and cannot be adapted to other types of activities. At the same time, it should be noted that non-tax incentives are not considered in the presented classifications of tax scientists, despite the fact that they are often integrated into complex preferential regimes aimed at providing expanded incentives to companies. Non-tax benefits are also presented as a targeted support mechanism aimed at subsidizing, providing preferential loans, and preferential access to public procurement.

Therefore, in order to increase the effectiveness of tax incentives and areas for their improvement, it is necessary to take into account the sectoral approach, which analyzes the impact of tax and non-tax incentives on a particular sector of the Russian economy. In this regard, it seems necessary to develop a more universal approach to classifying tax incentives (in an economic rather than a legal sense), applicable to a broader group of capital-intensive industries and taking into account the mutual application of various types of financial support. In the context of this study, the relevance of such a classification is primarily justified by the need to identify those categories of tax benefits that have the greatest economic impact on the development of the pharmaceutical industry and the achievement of government goals. A new approach to classifying tax incentives For the purposes of classifying tax benefits that meet the needs of the pharmaceutical industry in the Russian Federation, it is necessary to determine approaches to stimulating the industry. As noted earlier, pharmaceutical production is a knowledge-intensive and capital-intensive industry[17]. This feature dictates the need to implement large investment projects aimed at creating production facilities and developing medicines. Moreover, it is difficult to overestimate the importance of public procurement for pharmaceutical companies, which is reflected in the availability of benefits aimed at facilitating pharmaceutical companies' access to public procurement. Therefore, when classifying tax benefits, it is necessary to take into account the fact that the development of the pharmaceutical industry is based on the implementation of large investment projects, many of which have a high innovation component, as well as the significant influence of the public procurement sector on pharmaceutical companies. Thus, based on the assumptions considered and analyzed above, and the analysis of scientific literature, the author suggests the following classification of state support instruments for the pharmaceutical industry (and other capital-intensive industries): - point-to-point support tools;

- comprehensive support tools.

A point support tool is a separate benefit, advantage, or preference that is provided to a company in case of actual fulfillment of certain legal requirements without any counter obligations on the part of a legal entity. Such support tools mostly include tax incentives provided for by the Tax Code of the Russian Federation (for example, increasing coefficients for R&D expenses, increasing the coefficient to the depreciation rate, reduced corporate income tax rates, VAT and property tax exemptions). At the same time, certain non-tax incentive measures can also be attributed to them. Such measures include, first of all, the "second superfluous" and "third superfluous" rules, which allow companies to participate in public procurement with a preference in the case of the production of medicines with the status "Made in Russia". The essence of the preference is that if there is a company on public procurement (at least two companies in the case of the "third extra" rule) with medicines with the status "Made in Russia", other medicines are automatically rejected. A significant element of targeted support measures is direct budget financing provided within the framework of individual subsidies (budget financing within the framework of integrated support is excluded in this incentive group). A comprehensive support tool is a set of incentive measures (in some cases, support measures are limited to one targeted and significant support measure, for example, as in offset contracts and concessional financing) aimed at implementing a specific investment project, accompanied by the conclusion of an investment agreement with the government (or a similar contract), an obligatory element of which are specific incentive measures and the company's counter-commitment. Incentive measures in comprehensive support tools are provided before the actual implementation of investment projects, as they are aimed at supporting investment projects, ensuring their effective and speedy implementation. Based on the definitions presented, it can be seen that point-based and integrated support measures are actually opposite in nature (Table 2). Table 2 – Comparative characteristics of the proposed tools for supporting capital-intensive industries | Comparison criteria | Point tool | A comprehensive tool | | Availability of a taxpayer's reimbursable obligation | Missing | Required | | The condition for granting benefits |

When the specified conditions are met | Upon fulfillment of the established conditions and fulfillment of the counter obligation | | Terms of implementation of the tools | They can be applied within the framework of current activities. | They can be applied only within the framework of investment projects. | | Targeting | They are more widespread and less targeted due to the prohibition of individual tax benefits | More specific, targeted | | The effect of the application | Certain. Less tangible | Complex, often multiplicative. More tangible | | Example of tools | Increasing coefficient for R&D, investment tax deduction | Offset contract, SPIC, NWPC, SEZ |

The biggest difference lies in the moment of granting benefits and the occurrence of obligations for the company when implementing comprehensive support tools. With targeted support measures, benefits are provided when certain conditions are met (acquisition, incurring expenses, performing certain actions). In complex support measures, incentive measures are used for the purpose of supporting a specific investment project, performing certain actions involving the recipient's retaliatory liability (for example, the sale of production on the territory of a constituent entity of the Russian Federation). This feature also implies that the state is interested in implementing the investment project, since due to the provision of significant support measures, the state loses additional revenues to the budget of the Russian Federation. Consequently, the state provides for obligations for a legal entity in comprehensive support tools, non-fulfillment of which leads to fines and cancellation of incentive measures. Comprehensive support measures are the most effective and interesting for the pharmaceutical industry, as they are aimed at implementing investment projects, which in this segment implies the basis for the production of medicines, which is one of the most important tasks of the state to ensure drug safety and the needs of the healthcare system. Based on the features of comprehensive support tools, another important difference between comprehensive support measures is a more targeted focus.

In other words, comprehensive support tools are aimed at a small number of companies that meet certain requirements and are ready to invest in the development of production, including pharmaceutical. The targeted orientation allows the state to apply support measures most effectively by implementing a state incentive policy. Mass benefits cannot be commensurately effective, since they are aimed at a large range of companies based on the fact that such benefits will be ineffective for some companies for various economic reasons. Thus, another major difference is the effectiveness of comprehensive support tools and the effect of their use. Due to the materiality of the combination of various tax and non-tax incentive measures, the savings of a company in the implementation of an investment project are more significant than in the implementation of individual benefits, and a multiplier effect is often achieved. Targeted and comprehensive tax incentives Tax benefits are presented in both comprehensive and point-to-point support tools. In point-based support tools, tax benefits are the main ones. Moreover, some targeted tax benefits are the most significant and may partially match comprehensive support measures in terms of their impact on the taxpayer's activities (for example, an increased coefficient for research and development costs). Moreover, the R&D benefit is an important tool for supporting innovation. However, this benefit, for example, is not actually applicable with the integrated SPIC instrument, since SPIC offers a 0% corporate income tax rate as part of an investment project. It is worth noting that in 2025, amendments were made to the Tax Code of the Russian Federation, which increased the effect of applying the increasing R&D coefficient to 2. Special conditions were also introduced in this part for "small technology companies". It is worth noting that both applications of the increasing R&D coefficient are relevant for companies in the pharmaceutical sector. The choice of the option depends on the company's revenue (the maximum value is 4 billion rubles), as well as on the "convenience" of administrative procedures provided for by both options. Most comprehensive support measures (special investment contract ("SPIC"), regional investment project ("RIP"), agreement on protection and promotion of investments ("NWPC"), special economic zones ("SEZ")) include several types of tax benefits at once. These are mainly incentives for corporate income tax and corporate property tax. The most serious tax benefits for industry are provided through comprehensive support tools such as SPIC, RIP, and NWPC, where taxpayers are provided with significant tax benefits. These include full or partial exemption from corporate income tax, and in some cases, insurance premium rates are also reduced. In other words, tax incentives play a significant role in the application of comprehensive support tools. Moreover, since such benefits are granted for a significant period of time (on average, in the region of 5-8 years), companies, when planning investment projects, focus on the possibility of obtaining the greatest effect from tax savings by obtaining an appropriate support measure (for example, companies choose the region in which production will be implemented, in terms of the regional tax rate). corporate income tax as part of a comprehensive support measure). At the same time, it is worth noting that some of the comprehensive support measures (offset contracts, concessional financing) do not provide for any tax preferences. At the same time, they are also in high demand from legal entities. This is due to the fact that offset contracts and concessional financing also provide companies with significant preferences and opportunities for more efficient implementation of investment projects. Thus, we understand that point-to-point support tools and comprehensive support tools differ significantly in the scope and directions of benefits provided. In practice, companies, including pharmaceutical companies, try to maximize government support for the implementation of investment projects and, for example, receive concessional financing and SPIC in parallel. This approach allows companies to implement a project and reach the break-even level much earlier, which is an important factor in the implementation of large projects. Conclusions and suggestions 1. The classification of instruments for supporting the pharmaceutical industry has made it possible to determine the direction of development of stimulating the pharmaceutical industry, namely comprehensive support in the implementation of investment projects, since the latter is the main driver of growth in any knowledge-intensive and capital-intensive industry. At the same time, a competent classification of incentives makes it possible to distinguish between support tools and identify more effective and relevant ones, taking into account the specifics of the industry. 2. Comprehensive support tools are more effective measures to support investment projects, as they offer various tax and non-tax benefits, the effect of which is more significant than from targeted support tools. 3. Point-based support tools are important support tools because they affect individual costs, actions relevant to the pharmaceutical industry (such as R&D benefits), but they are not always compatible with the use of integrated tools. In this regard, the following are the priority areas for the development of tax incentives:: 1) the inclusion of existing tax benefits in comprehensive support tools in order to expand the possible range of investors and investment projects due to more serious tax benefits; 2) harmonization of classical tax benefits in order to be able to apply them with comprehensive support tools, which also expands the possible range of investors and investment projects; 3) the expansion of technological tax incentives within the framework of comprehensive support tools, which is due to the above-mentioned knowledge intensity of the industry.

The article is published in the version approved by the reviewers (after receiving the final positive review recommending the manuscript for publication), with corrections made by the author (submitted after receiving preliminary negative reviews that did not recommend the manuscript for publication).

All reviews (including preliminary negative reviews) are published in open access directly after the text of the article itself. All versions of the author's corrections are stored in the publisher's repository and may be available upon request by authorized organizations.

Read all reviews for this article

References

1. Boldenkov, A. V. (2019). The pharmaceutical industry as a component of the economy of Russia. Youth and Science, 5-6, 98. EDN LPWCQZ.

2. Bykov, S. S. (2013). Classification of tax benefits as a condition and stage of assessing their effectiveness. News of Irkutsk State Economic Academy, 5, 20-26. EDN REDPCN.

3. Migashkina, E. S. (2017). Systematization of tax benefits and preferences provided by Russian tax legislation for assessing their effectiveness. Applied Economic Research, 3, 48-55. EDN YMKONU.

4. Pepelyaev, S. G. (Ed.). (2015). Tax law: textbook. Alpina Publisher.

5. Krokhina, Y. A. (2013). Tax law: textbook (6th ed., rev. and add.). Yurait.

6. Kuleshova, N. A. (2020). The system of tax benefits in Russia: federal and local regulation. In Current Issues of Modern Science and Education: Proceedings of the Scientific Session 2020 of the Borisoglebsk Branch of FSBEI HE "Voronezh State University", 204-207. Perо. EDN ODNLVP.

7. Zinnurova, A. M. (2019). Classification of tax benefits. In Fundamental and Applied Aspects of the Development of Modern Science: Collection of Articles from the International Scientific and Practical Conference, Ufa, December 18, 2019 (Part 1, pp. 171-177). Scientific Publishing Center "Bulletin of Science".

8. Barulin, S. V., & Makrushin, A. V. (2002). Tax benefits as an element of taxation and a tool of tax policy. Finance, 2, 39-42. EDN VUFBBB.

9. Mayburov, I. A. (2007). Theory and history of taxation. Unity-Dana.

10. Avdeeva, V. M. (2024). Tax preferences as an object of tax control: a terminological aspect. Innovative Development of the Economy, 3, 97-102. https://doi.org/10.51832/222379842024397. EDN AXWPFL.

11. Balandina, A. S. (2011). Analysis of theoretical aspects of tax benefits and tax preferences. Bulletin of Tomsk State University, 4, 45-60.

12. Selyukov, M. V. (2023). The role of tax benefits in the implementation of tax policy. Innovative Economy and Society, 2, 46-52. EDN GSVXIP.

13. Habdaev, A. M. (2024). Types of tax benefits in the Russian Federation: a new look at the foundations of classification. Academic Legal Journal, 25(3), 492-499. https://doi.org/10.17150/1819-0928.2024.25(3).492-499. EDN PSFTDQ.

14. Pinskaya, M.R., Steshenko, Y.A. (2019). Diagnostics of industry susceptibility to tax incentives. Taxes and Taxation, 9, 14-25. https://doi.org/10.7256/2454-065X.2019.9.30978

15. Balandina, A. S. (2014). Theoretical foundations of the classification of sectoral tax benefits and preferences. Eurasian Union of Scientists, 6-1, 17-19.

16. Balandina, A. S. (2014). Classification of sectoral tax benefits using the example of the oil and gas industry. Socio-Economic Sciences and Humanitarian Research, 1, 35-39. EDN SZBPZP.

17. Yuldasheva, M. A. (2024). Development of the pharmaceutical industry as a factor in the modernization of the economy. Bulletin of the West Kazakhstan Innovative and Technological University, 29(1), 266-273.

First Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

An article on "Point and complex tax incentives to support the pharmaceutical industry" has been submitted for review for publication in the journal Taxes and Taxation. The article is devoted to the analysis of tax incentives aimed at supporting the pharmaceutical industry, with an emphasis on their classification and effectiveness. The author examines both point-based and complex instruments of state support, highlighting their role in the development of capital-intensive and knowledge-intensive industries. The subject of the research is relevant for economic and financial disciplines, especially in the context of national security and import substitution in the pharmaceutical industry. The research methodology is based on the author's use of general scientific methods such as deduction, induction, analysis and synthesis, which allows us to systematize existing approaches to the classification of tax benefits. However, the work could benefit from the use of empirical methods, for example, the analysis of data on the effectiveness of tax incentives in specific pharmaceutical companies (studies by D.V. Kondratova and I.Y. Sizova, 2023; A.N. Martynova, 2024; A.Y. Sekushina, 2024). There is also no quantitative analysis that could confirm or refute the author's hypotheses. The topic of the article is relevant, given the need to develop the pharmaceutical industry in the face of sanctions and reduced imports. However, the author should have linked his conclusions more clearly with current government initiatives, such as the strategy for the development of the pharmaceutical industry until 2030 (Decree of the Government of the Russian Federation dated March 30, 2024 No. 753-r). There is also a lack of analysis of recent changes in tax legislation, for example, amendments to the Tax Code of the Russian Federation aimed at supporting innovation. The scientific novelty of the article lies in the classification of tax incentives into point and complex ones proposed by the author, as well as in their comparative analysis. However, the author does not take into account recent research in the field of tax incentives, for example, work on the role of benefits in tax policy. In addition, there is a lack of criticism of existing approaches, which reduces the originality of the work. The style, structure, and content meet the required requirements. The article is well structured: introduction, methods, classification, conclusions. The style conforms to scientific standards, but in some places the text is overloaded with descriptive elements. For example, tables with classifications could be supplemented with specific examples from the practice of pharmaceutical companies. There are also not enough references to modern cases, such as the use of SPIC in pharmaceuticals. The bibliography includes classical works (Pepelyaev, Krokhina), but modern sources, including those mentioned above, are not sufficiently represented. It would also be useful to include data from the reports of the Ministry of Industry and Trade or the Federal Tax Service in recent years. The author mentions various approaches to classifying tax benefits, but does not provide arguments in favor of his position against alternative points of view. For example, it would be possible to critically evaluate the views of Balandina A.S. (2023) on industry benefits or discuss the limitations of the proposed classification. The conclusions of the article are logical and emphasize the importance of comprehensive support tools for the pharmaceutical industry. However, to increase the interest of readers, it would be worthwhile to add practical recommendations, for example, on optimizing the tax burden for pharmaceutical companies. The article will be useful for economists, tax specialists and representatives of the pharmaceutical business, but needs to be improved to meet the level of the Higher Attestation Commission journal. Thus, the article represents a significant contribution to the study of tax incentives for the pharmaceutical industry. However, for publication in a selected journal, it is necessary to supplement the work with modern sources, empirical data and a critical analysis of existing approaches. It is recommended for publication after revision.

Second Peer Review

Peer reviewers' evaluations remain confidential and are not disclosed to the public. Only external reviews, authorized for publication by the article's author(s), are made public. Typically, these final reviews are conducted after the manuscript's revision. Adhering to our double-blind review policy, the reviewer's identity is kept confidential.

The list of publisher reviewers can be found here.

The subject of research in the peer-reviewed work is tax incentives, which are considered using the example of the pharmaceutical industry. The research methodology is based on the application of general scientific methods: deduction and induction, analysis and synthesis, analogy. The relevance of the study is due to the fact that the pharmaceutical industry is a capital-intensive industry for which tax incentives are an important component of government financial support, complementing budgetary and credit forms of support. The scientific novelty of the work, stated by the authors, consists in a new approach to classifying tax incentives (using the example of the pharmaceutical industry), aimed at increasing the effectiveness of tax incentives and the impact of their application. The publication highlights the following sections: Introduction, Research Methods and Materials, Approaches to Classifying tax benefits, a new Approach to Classifying tax incentives, Point and Complex tax incentives, Conclusions and Suggestions, as well as a Bibliography. The article notes that the pharmaceutical industry is a capital-intensive and knowledge-intensive industry that requires significant investments both as a result of R&D and in the process of manufacturing in Russia. The publication provides data on the volume of the pharmaceutical market in the Russian Federation for 2022-2024, noting that tax incentives reduce the burden on companies, increase the return on investment in fixed assets, and contribute to the development of the industry. Various classifications of tax benefits are considered: according to the method of influencing the legal regulatory process, according to the procedure for obtaining benefits for taxpayers, according to the level of regulatory regulation, according to the degree of benefits, and the author's classification of state support instruments for the pharmaceutical industry (and other capital-intensive industries) is proposed: point-to-point support tools; comprehensive support tools. The following is a comparative description of the proposed tools for supporting capital-intensive industries according to the following criteria: the presence of a taxpayer's reimbursable obligation, the condition for granting benefits, the conditions for implementing the tools, targeting, the effect of their use, and examples. According to the authors, a competent classification of incentives makes it possible to distinguish between support tools and identify more effective and relevant ones, taking into account the specifics of the industry. The bibliographic list includes 17 sources – scientific publications of Russian authors on the topic in Russian journals in Russian. The text of the publication contains targeted references to the list of references confirming the existence of an appeal to opponents. As a remark, it should be noted that the Bibliography section should be expanded with foreign publications on tax incentives. This will allow us to summarize foreign experience in providing tax benefits and comply with the editorial Rules for the design of the list of references, according to which "The recommended volume of the list of references for an original scientific article is at least 20 sources, which should contain: at least a third of foreign sources; at least half of the works published in the last 3 years." The topic of the article is relevant, the material submitted for review corresponds to the subject of the journal "Theoretical and Applied Economics", contains elements of scientific novelty, has practical significance, may arouse interest among readers, and is recommended for publication after some revision, which can be carried out in a working order.

|

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.