|

DOI: 10.7256/2454-065X.2022.3.33881

EDN:

KCZTVP

Received:

09/10/2020

Published:

07/04/2022

Abstract: Currently, the problems of taxation of mineral extraction in the Russian Federation are very relevant, which is due not only to the formation of the monetary fund of the state, designed to finance the solution of various national tasks, but also to the rational use of natural resources. The mineral extraction tax (MET) is systemically important from the standpoint of the formation of tax revenues of the budget system of the Russian Federation. The industry specifics of the Russian economy, the predominance of extractive industries in GDP, and ensuring the profitability of the activities of extractive companies determine the significant attention of the state, business, and science to the issues of collection, administration, distribution, and reform of the mineral extraction tax. The subject of the study is the MET in the tax system of the Russian Federation. The methodological basis of the research consists of analysis, synthesis, ascent from the abstract to the particular, logical and historical methods, as well as other general scientific methods. The place and role of the MET in the tax system of the Russian Federation are considered, the place of this tax in the system of payments for the use of natural resources levied on the territory of our country is determined. Based on the statistical reports of the Federal Tax Service of the Russian Federation, it has been established that the receipts of mineral extraction tax are steadily increasing from year to year. This trend is due to an increase in the production of such types of hydrocarbon raw materials as oil, natural gas and gas condensate. It is determined that the contribution of the subjects of the Russian Federation to the formation of the monetary fund of the country is unequal, due to the difference in the mineral resource base in the regions. It is shown that in the coming decades Russia has a powerful potential to increase the tax revenues of the budget system through taxation of hydrocarbon production. The problems of taxation of mineral extraction in Russia are highlighted. The author comes to the conclusion that the budget system of the Russian Federation has a significant tax potential in the field of taxation of natural resources extraction, provided that favorable conditions for doing business are created.

Keywords:

mining, minerals, taxation of minerals, use of natural resources, hydrocarbon raw materials, gas condensate, tax system, oil, natural gas, taxation

This article is automatically translated.

Introduction Currently, the value of payments for the use of natural resources in the Russian Federation is very high. "Land and other natural resources are used and protected in the Russian Federation as the basis of the life and activities of the peoples living on the territory of the relevant territory" — so in the Constitution of the Russian Federation (Part 1 of Article 9) [1] the legislator recognizes natural resources as the basis for the well-being of the population and not unreasonably: on how effectively and expediently they will be used the natural wealth of the state depends on the welfare of the country as a whole and each of its citizens individually. There are quite a lot of works devoted to the taxation of mineral extraction. The issues of inequality in the distribution of the tax potential of the subjects of the Russian Federation are considered in the work of V. V. Matveev, L. V. Mazur, V. V. Bogachev [2]. The problems of reforming the taxation system of the oil and gas sector of the Russian economy and the directions of improving the taxation of mineral extraction are considered in the works of D. A. Artemenko, G. A. Artemenko [3], Ponkratov V. V., Pozdnyaev A. S. [4] and others. Various aspects of taxation of mineral extraction are described in the works of M. V. Mishustin [5], M. R. Dzagoeva, V. A. Kaitmazov [6], V. G. Panskov [7] and others. Despite many works devoted to the problem of taxation of mineral extraction, the place and role of mineral extraction tax in the tax system of the Russian Federation has not yet been fully studied. The purpose of this study is to study the place and role of the mineral extraction tax in the tax system Of the Russian Federation. Theoretical aspects of taxation of mineral extraction in the Russian Federation Natural resource payments are understood as a type of mandatory payments of a public-legal nature for the extraction and use of natural resources, the procedure for calculating and paying which is established by federal and regional legislation, as well as regulatory legal acts of municipalities. In accordance with the norms of the current legislation of Russia, natural resource payments are divided into two groups: tax and non-tax (Fig. 1).

Fig. 1. The system of natural resource payments levied on the territory of the Russian Federation The procedure for calculating and paying natural resource tax payments is regulated by the Tax Code of the Russian Federation. As for non-tax payments, the procedure for their calculation and payment is established by other rules of law (water, forest, land, etc.). It is worth recognizing that the current system of payments for the use of natural resources is particularly complex in legal regulation, since it includes payments of various types and nature, regulated by a large number of regulatory documents.legal acts at different levels. Payment for natural resources (land, water, forest funds, subsoil, wildlife and others) is generally charged: – for granting the right to use natural resources within the established norms; – for excessive and irrational use of natural resources; – for the reproduction of natural resources and their protection. One of the most important natural resource payments levied on the territory of our country is the mineral extraction tax. The taxation of mineral extraction is based on the withdrawal of natural (or mining) rent, which arises in connection with the use by mining organizations of natural "wealth" that allows them to extract income. The mineral extraction tax performs fiscal, incentive, environmental and compensatory functions: firstly, the collection of mineral extraction tax is designed to form the monetary fund of the state, used to solve certain national tasks; secondly, with the help of the MET taxation system (tax rates, tax benefits, etc.), the state is able to influence the volume of mineral extraction, regulating the process in the right direction for it; thirdly, the collection of mineral extraction tax has an impact on taxpayers by establishing regulations, restrictions, norms and recommendations regarding the negative impact on the environment; Fourth, taxation of mineral extraction is aimed at restoring natural resources and their reproduction. Currently, the procedure for calculating and paying MET is regulated by Chapter 26 of the Tax Code of the Russian Federation, put into effect by Federal Law of the Russian Federation No. 126-FZ of 08.08.2001. With the entry into force of this chapter of the Tax Code of the Russian Federation, the payment for the use of mineral resources, deductions for the reproduction of the mineral resource base, the excise tax on oil and stable gas condensate, established by the Instruction of the Ministry of Finance of the Russian Federation dated 04.02.1993 No. 8 "On the procedure and timing of payment to the budget for the right to use the subsoil", ceased to exist. Analysis of statistical data on the mineral extraction tax and forecast of the development of the oil and gas industry in Russia In recent years, the importance of the natural resource sector of the economy has been increasing in the Russian Federation, which can be traced, among other things, by tax revenues to the budget system of our country. As can be seen from the presented Figure 2, the MET accounts for 27% of the tax revenues of the consolidated budget of the Russian Federation.

Fig. 2. Structure of tax revenues of the consolidated budget of the Russian Federation for 2019 [8] Paragraph 1 of Article 96.6 of the Budget Code of the Russian Federation states that "oil and gas revenues of the federal budget are used for financial support of the oil and gas transfer, as well as for the formation of the Reserve Fund and the National Welfare Fund" [9]. Thus, the mineral extraction tax in the form of hydrocarbon raw materials (oil, natural combustible gas from all types of hydrocarbon deposits, gas condensate), along with export customs duties on hydrocarbon raw materials and goods produced from oil, is a source of formation of the Reserve Fund of the Russian Federation. Statistical reporting of the Federal Tax Service of Russia allows you to estimate the change in income from the MET. The data in Table 1 show that for the period from 2015 to 2019, the receipts of the tax in question in monetary terms tend to increase, and the share of MET in tax revenues of the budget system of the Russian Federation is also increasing. The decrease in mineral extraction tax receipts in 2016 was due to a decrease in oil prices on the world market (the average value of prices for Urals grade oil was US$ 41.65/barrel in 2016 against US$ 51/barrel in 2015). Table 1 Dynamics of MET receipts to the consolidated budget of the Russian Federation for the period from 2015 to 2019. | Year | Tax income (total), thousand rubles. | MET, thousand rubles. | The share of MET in tax revenues, % | | 2015 | 13 720 353 254 | 3 226 830 746 | 23,5% | | 2016 | 14 386 060 931 | 2 929 407 888 | 20% | | 2017 | 17 197 016 498 |

4 130 424 358 | 24% | | 2018 | 21 142 044 805 | 6 127 369 049 | 29% | | 2019 | 22 503 367 147 | 6 106 392 213 | 27% | Source: [10]. Table 2 shows the dynamics of the receipt of federal taxes levied in the Irkutsk region to the federal budget of the Russian Federation (Table 2). Table 2 Dynamics of federal taxes levied in the Irkutsk region to the federal budget of the Russian Federation in the period from 2015 to 2019. | Indicator | The amount of receipts, thousand rubles. | | 2016 | 2017 | 2018 | 2019 |

| Tax revenues, total | 116 488 305 | 180 180 788 | 270 113 322 | 279 330 617 | | Income tax | 4 319 434 | 6 895 264 | 10 816 440 | 10 554 197 | | VAT | 44 848 412 | 57 111 090 | 81 785 723 | 88 369 894 | | Excise duty | 829 369 | 7 049 824 | 5 001 005 |

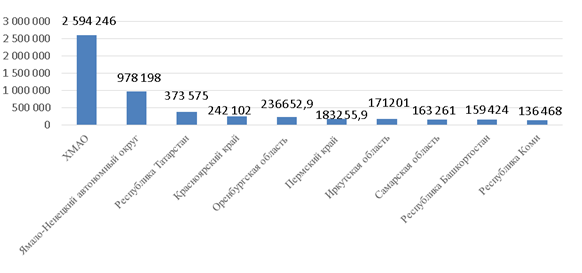

8 980 348 | | MET | 66 289 686 | 108 916 798 | 172 278 342 | 171 201 011 | | Water tax | 37 092 | 48 523 | 73 392 | 86 058 | | State duty | 164 078 | 159 186 | 158 357 | 139 029 | Source: [11]. From the presented statistical data it can be seen that the largest revenues to the federal budget of the Russian Federation are provided by the MET (more than 60%) and VAT (30%). Moreover, during the analyzed period, mineral extraction tax receipts increased more than twice, which is quite natural: a large-scale mineral resource base has been created in the Irkutsk region, which includes deposits of more than 60 types of minerals, including oil, natural gas and gas condensate. The absolute leaders in the receipt of MET in the federal budget of the Russian Federation are the Khanty-Mansiysk and Yamalo-Nenets Autonomous Okrugs (Fig. 3).

Fig. 3. Subjects of the Russian Federation with the highest MET receipts to the federal budget of the Russian Federation, 2019 (million rubles) [12] Based on the analysis, it can be concluded that the role of the MET in the formation of the revenue side of the budget system of the Russian Federation is very significant. Every year, in our opinion, the importance of the mineral extraction tax in the formation of the budget of our country will only increase, since mining has been the basis of the economic activity of the Russian Federation for quite a long time. Hydrocarbon raw materials (primarily oil) are the main resource asset of the Russian Federation, providing leadership in the reserves and production of this type of mineral raw materials, the demand for which determines a high level of profitability of oil production and refining. [13] The gas industry in the Russian Federation is the second most important of all the other resource-producing industrial complexes in our country. Tax payments from gas production bring significant revenues to the budget, second only to oil production. The gas industry includes enterprises that carry out geological exploration, drilling and operation of wells, production, transportation and storage of gas. Gas production in the Russian Federation is among the world leaders due to a fairly high level of domestic demand and large supplies to foreign markets. According to the statistical reports of the Federal Tax Service of Russia [14], the largest revenues of the mineral extraction tax are provided by the extraction of oil (86%), natural gas (10%) and gas condensate (3%). In total, 99% of tax revenues are provided by the extraction of hydrocarbon raw materials, only 1% is accounted for by all other minerals (concentrates and other intermediates containing gold, silver and platinum; natural diamonds; precious stones; coal, etc.). In terms of oil production in the world, Russia currently ranks third, second only to the United States and Saudi Arabia. During the period from 2014 to 2018, the volume of oil production in our country increased by 30 thousand tons, which amounted to 6% (Table 4). Table 4 Dynamics of oil production volumes among the largest oil-producing powers for the period from 2014 to 2018. | A country | Production volume, thousand tons | | 2014 | 2015 | 2016 | 2017 | 2018 | | USA | 524 | 567 | 545 |

580 | 676 | | Saudi Arabia | 541 | 565 | 584 | 563 | 583 | | Russia | 526 | 534 | 548 | 547 | 556 | | Canada | 216 | 222 | 219 |

241 | 259 | | Iraq | 154 | 173 | 222 | 225 | 230 | | Iran | 162 | 161 | 214 | 229 | 214 | | China | 214 | 217 | 203 |

195 | 193 | Source: [15] Today, the world energy market places the greatest emphasis on natural gas. The widespread use of this type of raw material in the economy is due to its environmental friendliness, technological efficiency and efficiency of use in industry and the municipal sector. Over the past 20 years, the increase in gas production and consumption in the world has amounted to more than 70%. At the same time, world gas trade increased by 46% and reached 1 trillion. 134 billion cubic meters of gas. [16] Studies show [17] that the natural gas market has a strong potential for development. The data presented in Table 5 show that the volume of natural gas production in Russia has been steadily increasing over the past decade, a similar trend is observed with respect to gas condensate. Table 5 Dynamics of natural gas and gas condensate production in Russia in the period from 2009 to 2018. | Year | Amount of natural gas produced, million cubic meters . | Growth rate | Amount of extracted gas condensate, thousand tons | Pace growth | | 2009 | 519 583 | — | 16 101 | — | | 2010 | 581 251 |

12% | 16 783 | 4% | | 2011 | 597 628 | 3% | 18 048 | 7,5% | | 2012 | 577 284 | -3% | 19 018 | 5% | | 2013 | 585 579 | 1,5% | 22 483 |

18% | | 2014 | 551 691 | -6% | 23 701 | 5% | | 2015 | 541 338 | -2% | 29 338 | 24% | | 2016 | 541 013 | -0,06% | 30 539 | 4% | | 2017 | 588 974 |

9% | 30 013 | -2% | | 2018 | 616 797 | 5% | 30 254 | 0,8% | Source: [18] It is worth admitting that Russia ranks first in the world in terms of gas reserves, second in terms of gas production, second only to the United States (Table 6). Table 6 Dynamics of gas production by the largest gas producing powers for the period from 2014 to 2018. | A country | The volume of natural gas production, million cubic meters. | | 2014 | 2015 | 2016 | 2017 | 2018 |

| USA | 733 | 767 | 755 | 775 | 864 | | Russia | 647 | 638 | 644 | 694 | 741 | | Iran | 175 | 184 | 200 |

214 | 232 | | Canada | 164 | 165 | 174 | 181 | 188 | | Qatar | 160 | 167 | 169 | 169 | 168 | | China | 130 |

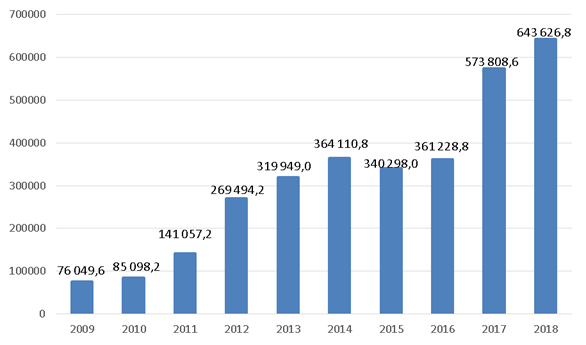

135 | 137 | 148 | 160 | | Norway | 113 | 121 | 121 | 128 | 127 | Source: [19] The increase in the production of natural gas and gas condensate directly affects tax revenues to the budget system of the Russian Federation. As can be seen from Figure 4, mineral extraction tax receipts in the form of natural gas increased from 76 to 644 billion rubles, that is, nine times, due to the increasing demand for this type of raw material on the world energy market.

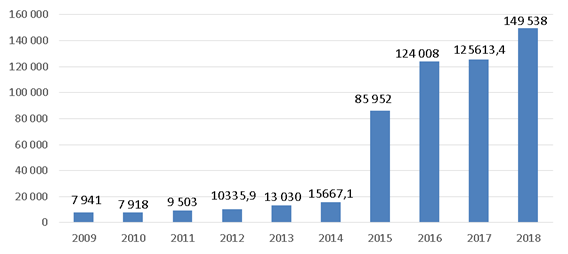

Fig. 4. Dynamics of MET income from natural gas production in Russia in the period from 2009 to 2018, million rubles [20] Static tax reporting shows that the MET receipts in the form of gas condensate are increasing at the highest rate (Fig. 5). Over the past decade, the receipts of this payment have increased from 8 to 150 billion rubles, that is, almost 20 times. The increase in gas condensate production and, as a result, tax revenues from the extraction of this hydrocarbon raw material is due to the increasing demand for it on the world market: the value of "white oil" is due to the characteristics of this raw material – ultra-light, high-quality oil with an appropriate yield potential of light, allowing for an equal amount of refining with conventional oil to obtain a larger amount of petroleum products. The profitability of supplying this type of raw material abroad is also high compared to crude oil due to savings on export duties due to the lower density of gas condensate. [21]

Fig. 5. Dynamics of MET income from gas condensate production in Russia in the period from 2009 to 2018, million rubles [22]

The above analysis shows that the gas industry in Russia has experienced a significant increase in the production, processing and export of natural gas and gas condensate in the last decade. This is confirmed by the increasing volumes of hydrocarbon production every year, the development of new deposits and the growing demand of consumers both within the country and abroad for this type of raw material. The positive dynamics of the development of this type of resource extraction and processing industry in Russia has a beneficial effect on the development of certain regions of the country, in which natural gas and gas condensate are mainly produced. Among other things, due to this industry, the revenue part of the budget of our country is rapidly increasing. According to experts, gas will be the most demanded hydrocarbon resource in the period up to 2040, because this resource meets environmental requirements most of all, has huge reserves in the world, production and transportation capabilities. It will be in demand in many areas of the economy, the electric power industry, and its role will grow in transport. [23] According to general forecasts, the demand for gas in the near future for the period up to 2035 will grow by 40%, and gas trade will increase by 2.6% annually.[24] In general, the supply of gas on the world market will grow by 1 trillion. 477 billion cubic meters . Analysts also predict the expansion of the liquefied natural gas market, according to the latter, this industry will develop rapidly, so the share of liquefied natural gas in the world gas market will increase to 70%. [25] Minister of Energy of the Russian Federation A. Novak noted that consumers of this type of hydrocarbon raw materials are expected to double in the next decade. It is believed that the share of liquefied natural gas in the structure of world trade will grow 2.3 times, and the trade in pipeline gas will increase by 15-20%. The excess of demand over supply will create a potential niche in the period from 2024 to 2035 in the amount of approximately 250 million. tons relative to the current level of 300 million tons. [26] By 2025, analysts believe, the liquefied natural gas market will grow by more than a third and amount to about 440 million tons. As the Minister of Energy of the Russian Federation assured, Russia has significant potential in increasing the volume of gas production and production of liquefied natural gas. In the main sales markets, the demand for gas will only grow, especially in Europe and the Asia-Pacific region. In Yamal, Russian reserves of liquefied natural gas amount to about 40 trillion cubic meters and the resource base allows for the production of this type of hydrocarbon raw materials in the amount of at least 115 million tons per year. The projected development potential of this industry indicates a possible increase in budget revenues of the Russian Federation due to the gas industry, however, this will be possible only with an adaptive approach of tax regulation in this sector of the economy. Speaking about the tax burden on the oil and gas industry, it is worth noting that this indicator varies depending on the chosen methodology. According to various estimates, the tax burden ranges from 20 to 50% (Table 7). Table 7 Tax burden on the oil industry, calculated by various methods, 2011-2017 | Methodology | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | |

Ministry of Finance of the Russian Federation | 19% | 19% | 20% | 20% | 21% | 22% | 25% | | Kreinina M. N. | 69% | 68% | 69% | 63% | 58% | 81% | 65% | | Litvin M. I. | 48% |

48% | 47% | 50% | 54% | 79% | 58% | | Kadushin A., Mikhailova N. | 27% | 26% | 26% | 20% | 23% | 25% | 24% | | Pasco O. F. | 44% | 49% |

45% | 55% | 47% | 44% | 46% | Source: [27, p. 49] Currently, mineral extraction organizations have a growing need for investments in the development of deposits in new oil and gas provinces, in the development of transport and processing capacities. [28] The industry has faced a number of internal and external problems, for example, deterioration of the quality and structure of the commodity base, an increase in the share of hard-to-recover oil reserves. The costs of solving these and many other problems have an impact on the financial performance of oil companies and investment opportunities in the sustainable development of industry and the economy as a whole. [29] All these factors, coupled with a high tax burden and a high level of financial risks caused by fluctuations in foreign oil and gas markets and the exchange rate of the national currency [30], have a direct impact on the financial stability of oil and gas industry enterprises. Problems of taxation of mining

in the Russian Federation Among the problems related to the calculation, payment and administration of MET are: 1) the problem of determining the value of minerals, which creates difficulties in the calculation of tax by taxpayers and the administration of mineral extraction tax by tax authorities. The problem of estimating the value of a mineral has been singled out by experts for quite a long time as grounds for adjusting the mechanism of taxation of mineral extraction. According to experts, the consequence of using the calculated method of determining the tax base, in addition to budget losses, is an excessive tax burden on enterprises that incur higher production costs, especially in the case of the development of the worst-quality mineral reserves. In addition, the content of the list of expenses and the procedure for their recognition, taken into account in the process of determining the tax base for the tax under study, is also ambiguously determined. A possible solution to this problem may be the introduction of amendments to the tax legislation regarding the establishment of tax rates, which will allow taking into account the specifics of the extraction of all types of minerals and at all stages of field development. [31] This will increase the attractiveness of low-profit deposits for investors, as well as reduce the number of tax offenses by subsoil users who bear an excessive tax burden. 2) the problem of the lack of comprehensive differentiation of mineral extraction tax rates depending on the mining, natural-geographical and economic conditions of the development and development of the deposit. To date, differentiation, which contributes to the creation of approximately the same economic conditions for the implementation of the activities of organizations, is achieved by applying a large number of coefficients, applying a zero rate, excluding an object from the list of objects of taxation, as well as the introduction and application of various kinds of tax benefits. It is worth recognizing that at the moment taxpayers developing low-margin deposits bear the same tax burden as taxpayers developing fairly profitable deposits. As a result, hard-to-reach areas with problematic recovery of minerals from the subsoil become less attractive to investors. Meanwhile, the state should be interested in the development of hard-to-reach deposits, since their development inevitably contributes to the development of the territories (regions, regions, districts) in which they are located. A single level of tax burden for subsurface users will make it possible to implement the fiscal function of the mineral extraction tax more efficiently, since the burden of paying the mineral extraction tax will be redistributed depending on the specifics of mining. In addition, differentiation will make it possible to implement the regulatory function of the mineral extraction tax and encourage taxpayers to carry out the extraction of a certain type of minerals in certain subsurface areas, depending on the needs of the state. 3) the problem of applying tax benefits in the payment of mineral extraction tax. To date, the tax legislation provides not so many stimulating conditions for the development of absolutely new deposits, which are naturally characterized by a large number of expenses (costs), the complexity of geological and geographical conditions, the need to develop an infrastructure environment, as well as greater distance from the potential sales market. According to the calculations of the project oil and gas institutes for the profitable development of new fields, it is not enough to establish those tax benefits for mineral extraction tax that the state offers to the taxpayer, therefore, this problem has a solid foundation and requires its solution by the state. [32] 4) administration of MET payment. Taxation of the extraction of natural resources is characterized by certain specifics and narrow focus, which complicates the process of implementing tax control measures. When administering the mineral extraction tax, experts highlight such problems as the problem of determining the value of the extracted mineral, determining the object of taxation, as well as determining the legality of applying certain tax benefits. Often, conducting a tax audit regarding the correctness of determining the value of a mineral when applying the calculation method by a taxpayer causes the greatest difficulties, since the approved list of expenses and the procedure for their recognition as a tax base is often subject to ambiguous interpretation.

Another difficulty in conducting a tax audit arises due to the use of a large number of different coefficients, which are regularly changed. This problem is aggravated by the fact that in the case of extraction by one taxpayer of various types of minerals and at various deposits, it is necessary to take into account all the features of taxation of mineral extraction. In addition, each field undergoes a large number of changes during its operation, which also needs to be taken into account when carrying out tax control measures. Speaking about the importance of the mineral extraction tax in the tax system of the Russian Federation, it should also be noted the problem of inequality of the regions of our country, which is due to the concentration of the mineral resource base only in certain subjects of the Russian Federation. According to the World Bank report "On the way to a new Social Contract", Russia is among the top three in terms of regional inequality within the country among the states of Europe and Central Asia, and even ahead of large emerging economies such as India, China and Brazil. In the period from 2014 to 2019, 72 regions consistently receive subsidies to equalize budget security. Only 13 regions are non-subsidized, the main donors of which are the oil-rich KhMAO and Yamalo-Nenets Autonomous District, the Republic of Tatarstan and the federal cities of Moscow and St. Petersburg. They can rightfully be called budget-forming, since they provide more than half of all tax payments: some due to the concentration of the mineral resource base on their territory, others due to the high concentration and diversification of large businesses. As a result, the social and economic stratification of society increases. It is quite obvious that regional inequality takes place in a state with more than 80 regions, however, the scale of this inequality in our country can be called unprecedented. It is worth noting that since January 1, 2019, Russia has moved to the process of completing a tax maneuver in the oil industry, the purpose of which is to diversify Russian exports of oil and petroleum products. [33] The tax maneuver as such involves reducing the export duty on oil and petroleum products to zero and simultaneously increasing the mineral extraction tax, which, according to the legislator, will allow: — to reduce the amount of subsidies to the EurAsEC economies and inefficient oil refining in Russia; — to ensure the growth of budget revenues and the termination of the activities of producers of surrogate fuels; — to gain full control over prices on the domestic market of motor fuels due to a compensation mechanism – a damper, which will return to oil companies part of the lost export profits when selling fuel on the domestic market; — to form a more effective system of tax benefits and subsidies; — achieve more profitable exports, as well as partially get rid of the dependence of oil prices on the global market. At the same time, practice shows that the tax maneuver does not have the best effect on the oil industry: — substitution of export duties for mineral extraction tax provokes an increase in the cost of oil and petroleum products on the domestic Russian market; — only a part of oil refineries whose results meet certain requirements (production volume, processing volume, volume of supplies to the domestic market, etc.) can receive a return (return) excise tax.; — constant fluctuations in the tax burden negatively affect the operation of oil refineries, as a result, it is increasingly difficult for the latter to attract investors to implement modernization projects and maintain stable refining volumes. For some enterprises, there was a risk of closure at all (for example, the President of the Antipinsky Oil Refinery (Novy Potok) Group of Companies, D. Mazurov, linked the bankruptcy and financial difficulties of the company with the initiative of the Ministry of Finance of the Russian Federation). It is worth admitting that there are numerous disputes around the tax maneuver in the oil sector. Thus, the first deputy chairman of the State Duma Committee on Economic policy, Industry, innovative development and Entrepreneurship V. Hartung proposed to sharply increase the export duty on oil and cancel VAT refunds to exporters of "black gold". This, according to the deputy, will reduce the incoming price of oil at refineries in the country and increase the profitability of oil refining. At the same time, the attractiveness of raw material exports will significantly decrease. [34] The ambiguous direction of reforming the taxation system in the oil and gas sector is also indicated by the introduction of a tax on additional income from the extraction of hydrocarbon raw materials, which provides for taxation not of the extraction of hydrocarbon raw materials as such, but of the income received from its sale. According to the results of the experiment, which took place at 35 license areas of a number of large and small oil companies, the amount of lost revenue amounted to 213 billion rubles in 2019, which is comparable to the cost of tax holidays for small and medium-sized businesses for two quarters. Deputy Head of the Ministry of Finance of the Russian Federation A. Sazanov admitted that he considers the introduction of a tax on added income to be the main mistake in his career. The Ministry of Energy of the Russian Federation, in turn, considers the experiment successful, believing that the introduction of this tax will avoid a possible drop in production, which may occur in a few years in the event of a tightening of the fiscal regime. Based on the above, it should be recognized that the tax maneuver in the oil industry is an unprecedented attempt to regulate the oil market. In our opinion, the budget system of the Russian Federation has a significant tax potential in the field of taxation of mineral extraction. In order to receive large tax revenues, the state needs to provide favorable conditions for the further development of this industry, as well as the stability of the economic situation in the country. When developing the concept of taxation of hydrocarbon production, it is necessary to base on the following approaches: taxation of the results of companies' activities; stimulation of rational use of mineral resources and the most complete extraction of the main and associated components; economic and budgetary efficiency; ease of administration. [35] Undoubtedly, the importance of tax payments for ensuring the national security of any state is very great. [36] However, the best tax policy in the modern conditions of the development of the system of world economic relations is a tax policy focused on the regulatory (stimulating), and not on the fiscal role of taxes. [37]

The article is published in the version approved by the reviewers (after receiving a positive review recommending the manuscript for publication) with corrections made by the author (after receiving the editor’s comments, if any).

Read all reviews on this article

References

1. Konstitutsiya Rossiiskoi Federatsii (prinyata vsenarodnym golosovaniem 12.12.1993) // Spravochno-pravovaya sistema "Konsul'tant"

2. Matveev V. V., Mazur L. V., Bogacheva V. V. Neravenstvo raspredeleniya nalogovogo potentsiala sub''ektov RF / V. V. Matveev, L. V. Mazur, V. V. Bogachev // Vestnik OrelGIET. — 2017. — №4 (42). — S. 85—91.

3. Artemenko D. A., Artemenko G. A. Reforma sistemy nalogooblozheniya neftegazovogo sektora rossiiskoi ekonomiki / D. A. Artemenko, G. A. Artemenko // Gosudarstvennoe i munitsipal'noe upravlenie. Uchenye zapiski SKAGS. — 2017. — №2. — S.75—80.

4. Ponkratov V. V., Pozdnyaev A. S. Nalogooblozhenie dobychi nefti v Rossii – posledstviya nalogovykh manevrov / V. V. Ponkratov, A. S. Pozdnyaev // Neftyanoe khozyaistvo. — 2016. — №3. S. 24—27.

5. Mishustin M. V. Faktory rosta nalogovykh dokhodov: makroekonomicheskii podkhod / M. V. Mishustin // Ekonomicheskaya politika. — 2016. — T. 11. — № 5. — S. 8—27.

6. Dzagoeva M. R., Kaitmazov V. A. Nalog na dobychu poleznykh iskopaemykh kak odin iz osnovnykh istochnikov dokhodov gosudarstva / M. R. Dzagoeva, V. A. Kaitmazov // Ekonomika i predprinimatel'stvo. — 2016. — №10-2 (75). — S. 927—932.

7. Panskov V. G. Nalogi neftyanogo sektora: izmeneniya neobkhodimye, no nedostatochnye / V. G. Panskov // Nalogovaya politika i praktika. — 2008. — №11. — S. 12—19.

8. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

9. Byudzhetnyi kodeks Rossiiskoi Federatsii ot 31 iyul. 1998 g. №145-FZ // Spravochno-pravovaya sistema «Konsul'tant».

10. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

11. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

12. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

13. Budueva K. D. Analiz neftegazovykh dokhodov federal'nogo byudzheta Rossiiskoi Federatsii / K. D. Budueva // Vestnik IEAU. — 2017. — № 16.

14. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

15. Ctatisticheskii ezhegodnik mirovoi energetiki [Elektronnyi resurs]. — URL: https://yearbook.enerdata.ru/

16. Gorbach A. P. Sovremennoe sostoyanie vnutrennego rynka prirodnogo gaza i tendentsii ego razvitiya / A. P. Gorbach // European scientific conference: materialy Mezhdunar. nauch. konf. — Anapa, 2019. — S. 10—16.

17. Tsvigun I. V. Mirovoi rynok szhizhennogo prirodnogo gaza: sovremennaya kon''yunktura i tendentsii razvitiya / I. V. Tsvigun, E. V. Ershova // Izvestiya Baikal'skogo gosudarstvennogo universiteta. — 2016. — T. 26. — №6. — S. 868—881.

18. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

19. Ctatisticheskii ezhegodnik mirovoi energetiki [Elektronnyi resurs]. — URL: https://yearbook.enerdata.ru/

20. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

21. Shibanov A. I. Tekhniko-ekonomicheskaya otsenka protsessa pererabotki stabil'nogo gazovogo kondensata / A. I. Shibanov, O. V. Andrukhova //Upravlenie i ekonomika: issledovanie i razrabotka: materialy Mezhdunar. nauch.-prakt. konf. — Penza, 2019. — S. 114—120.

22. Ofitsial'nyi sait Federal'noi nalogovoi sluzhby RF [Elektronnyi resurs]. — URL: https://www.nalog.ru

23. Dolgaya O. Klyuchevye trendy global'noi energetiki [Elektronnyi resurs]. — Rezhim dostupa: https://belchemoil.by/news/analitika/klyuchevye-trendy-globalnoj-energetiki

24. «EkoGrad»: Kakim budet global'nyi gazovyi rynok — 2030? [Elektronnyi resurs]. — Rezhim dostupa: http://ekogradmoscow.ru/.

25. «EkoGrad»: Kakim budet global'nyi gazovyi rynok — 2030? [Elektronnyi resurs]. — Rezhim dostupa: http://ekogradmoscow.ru/.

26. «EkoGrad»: Kakim budet global'nyi gazovyi rynok — 2030? [Elektronnyi resurs]. — Rezhim dostupa: http://ekogradmoscow.ru/.

27. Filimonova I. V. Klasternyi analiz kompanii neftyanoi promyshlennosti po parametram nalogovoi nagruzki / I. V. Filimonova, I. V. Provornaya, S. I. Shumilova, E. A. Zemnukhova // Journal of Tax Reform. — 2019. — T. 5. — S. 42—56.

28. Ponkratov V. V. Nalogooblozhenie dobychi nefti v Rossii – posledstviya nalogovogo manevra / V. V. Ponkratov // Journal of tax reform. — 2015. — №1. — S. 112.

29. Filimonova I. V. Klasternyi analiz kompanii neftyanoi promyshlennosti po parametram nalogovoi nagruzki / I. V. Filimonova, I. V. Provornaya, S. I. Shumilova, E. A. Zemnukhova // Journal of Tax Reform. — 2019. — T. 5. — S. 42—56.

30. Shupletsov A.F. Instrumenty khedzhirovaniya riskov: effektivnost' i znachimost' ikh ispol'zovaniya v protsesse formirovaniya strategii razvitiya rossiiskikh neftegazovykh kompanii / A. F. Shupletsov, A. I. Perelygin // Izvestiya Baikal'skogo gosudarstvennogo universiteta. — 2020. — T. 30. — № 2. — S. 318—325.

31. Il'icheva M. A. Pravovoe regulirovanie nalogovykh otnoshenii s uchastiem krupneishikh nalogoplatel'shchikov (na primere predpriyatii neftegazovoi otrasli) / M. A. Il'icheva // Nalogi (zhurnal). — 2016. — № 5. — S. 31.

32. Palyuvina A. S. Sovershenstvovanie sistemy nalogovykh l'got pri raschete NDPI v RF / A.S. Palyuvina, M. V. Kashirina // Finansovoe pravo i upravlenie. — 2016. — № 3. — S. 244—259.

33. Shupletsov A. F., Bun'kovskii D. V. Diversifikatsiya rossiiskogo eksporta nefti i nefteproduktov / A. F. Shupletsov, D. V. Bun'kovskii // Izvestiya Baikal'skogo gosudarstvennogo universiteta. — 2016. — T. 26. — № 6. — S. 889—895.

34. Mavrina L. V Gosdume predlozhili otmenit' nalogovyi manevr v neftyanke [Elektronnyi resurs]. — URL: https://www.vedomosti.ru/economics/articles/2020/09/01/838485-otmenit-manevr

35. Ponkratov V. V. Nalogooblozhenie dobychi nefti v Rossii – posledstviya nalogovogo manevra / V. V. Ponkratov // Journal of Tax Reform. — 2015. — T. 1. — S. 100—112.

36. Fedotov D. Yu. Rol' nalogov v obespechenii natsional'noi bezopasnosti Rossii / D. Yu. Fedotov // Journal of Tax Reform. — 2017. — T. 3. — S. 6—17.

37. Pogorletskii A. I. Nalogovaya politika v sovremennom mire: osobennosti i perspektivy, realizatsiya v Rossii / A. I. Pogorletskii // Journal of Tax Reform. — 2017. — T. 3. — S. 29—42.

|